Column: Obama's tax cut plan takes pressure off Bernanke

President Obama's tax cut plan, by lowering unemployment and boosting economic growth, may ease the Federal Reserve's pressure to buy Treasuries via its controversial program of quantitative easing (QE).

The Fed is mandated by law to maintain maximum employment and price stability. By the middle of 2010, because of the weak economy, the unemployment rate remained elevated and there were serious concerns of deflation.

The Fed, having already lowered interest rates to near-zero, felt compelled to act further in order to meet their dual mandate. Therefore, on November 3, it announced a controversial program of purchasing $600 billion in longer-term Treasuries by mid-2011 (commonly referred to as QE2).

The program was widely criticized. PIMCO's Bill Gross called it was a Ponzi scheme. German Finance Minister Wolfgang Schaeuble called it clueless. The Chinese cried foul -- probably both as an owner of U.S. debt and from an exchange rate perspective.

Some U.S. politicians were even suggesting measures that would encroach upon the independence of the central bank.

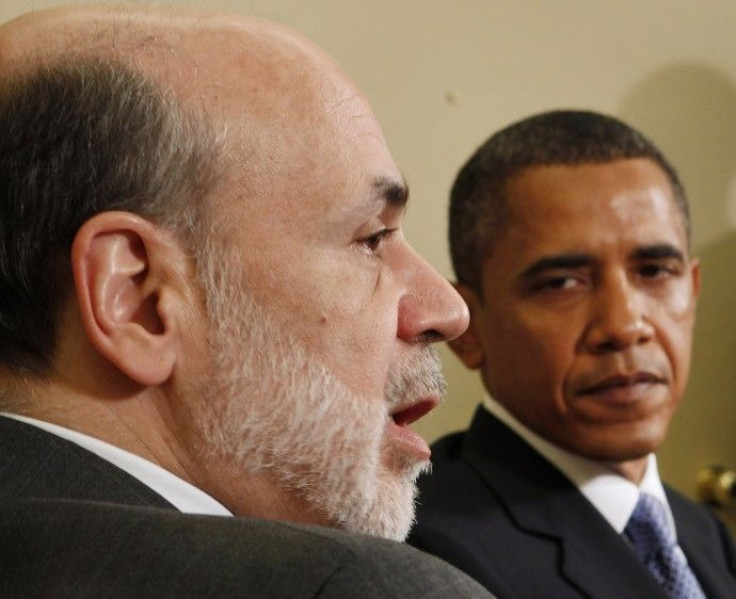

On November 30, Fed Chairman Ben Bernanke felt compelled to tape an interview with the 60 Minutes TV news program to defend QE2 to a skeptical public.

It might be reasonable to assume that if the jobs market and inflation level were acceptable to Bernanke, he would spare himself all these headaches.

Obama's tax cut plan, which is essentially a multi-hundred-billion-dollar stimulus package through tax cuts and government spending, may boost inflation and the jobs market and take some pressure off Bernanke.

Obama's package targets the Fed's dual mandate pretty well.

It includes a payroll tax cut, which specifically relates the jobs market.

Even though the Fed aggressively expanded U.S. monetary supply, deflation still loomed a few months ago because consumer prices were held down by wages (a reflection of the poor jobs market) and the slack in the economy. Obama's fiscal stimulus should address these two issues.

Many prominent economists -- although they don't agree with every single detail of it -- agree with the general direction of Obama's plan. Nouriel Roubini and Richard Koo are among them.

They believe fiscal stimulus is what the economy really needs. However, because legislators lack resolve, the burden of propping up the economy has fallen on the monetary authority. Unfortunately, monetary stimulus doesn't work as well as fiscal stimulus in this case. Moreover, it fuels asset bubbles and creates dangerous distortions.

Now, with fiscal stimulus finally picking up some of the slack, the responsibilty is no longer solely on Bernanke.

In an adverse scenario, it may prop up the economy enough to allow the Fed to not push for a third round of quantitative easing. In a more favorable scenario, it may boost the economy enough for the Fed to cut short QE2 and not spend the entire $600 billion amount.

For the market, one implication of Obama's tax plan is rising longer-term Treasury yields. One, the plan eases pressure on Bernanke to buy Treasuries as a part of the QE2 program. Two, yields usually rise during economic expansions. Three (in an admittedly unlikely scenario), the mounting budget deficit will shake confidence in U.S. sovereign debt.

Email Hao Li at hao.li@ibtimes.com

Click here to follow the IBTIMES Global Markets page on Facebook.

Click here to read recent articles by Hao Li.

© Copyright IBTimes 2024. All rights reserved.

-

French Air Traffic Controller Strike Threatens Flight Chaos

-

Azerbaijan Says 'Closer Than Ever' To Armenia Peace Deal Amid Border Talks

-

How UK's Biggest Water Supplier Sank Into Crisis

-

Taiwan Hit By Dozens Of Strong Aftershocks From Deadly Quake

-

Gaza Health System 'Completely Obliterated': UN Expert

-

In Ecuadoran Amazon, Butterflies Provide A Gauge Of Climate Change

-

50 Years On, Vintage Vehicles To Reenact Portugal's Carnation Revolution

-

Conflicts Push Military Spending To 'All-time High': Report

-

'Thank You, America:' Zelensky And Netanyahu Applaud House Passage Of Foreign Aid Package

-

Women Journalists Bear The Brunt Of Cyberbullying