India Economic Expansion Slowest In A Decade; It Was 9% In 2011, Now It’s Less Than 5%

India’s economic growth stood at 4.8 percent in the first three months of the year, which is the country’s fourth fiscal quarter, only slightly higher than the 4.7 percent it registered in the previous three-month period, the slowest in 15 quarters, according to official statistics released Friday.

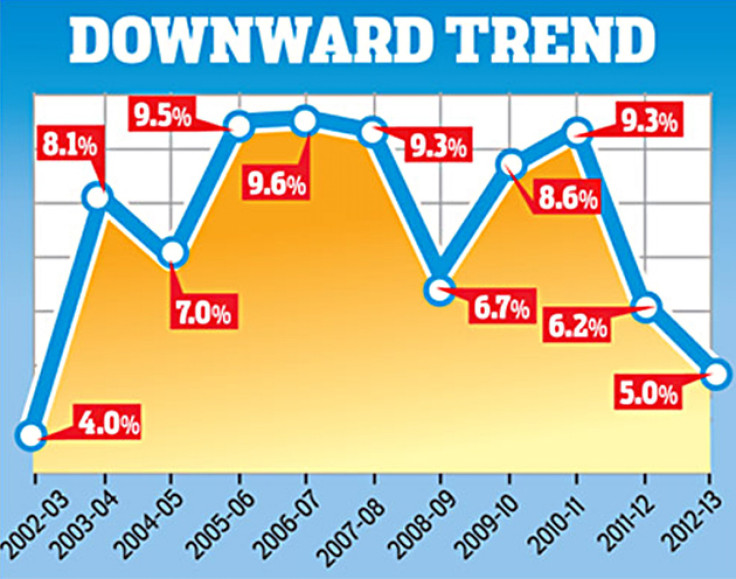

For the fiscal year, the country’s economic output stands at 5 percent, significantly lower than the 9.6 percent annual growth the country topped off at in fiscal year 2006-07 prior the global economic downturn. It’s also considerably down from a rebounded FY2010-11 when the country again topped 9 percent growth.

This graphic from India Today shows the extent by which the country’s expansion has slowed:

(Click here to see what Indian auto giant Tata Motors Ltd.’s (NYSE:TTM) most recent earnings report shows about how much consumer demand for its vehicles has slowed, a significant indication of the loss in consumer confidence and income.)

Perhaps more significantly: Asia’s third largest economy has seen economic expansion drop since the start of the 2011 fiscal year to levels even lower than the 2008-09 global recession caused largely by the global banking system’s sketchy bartering of debt.

"It is imperative that both the government and the RBI [Reserve Bank of India] get their acts together," Jyotinder Kaur, an economist with HDFC Bank Limited (NYSE:HDB) told India Today. "The room for policy response is limited but it is not completely absent.”

Most estimates suggest a rebound for 2013-14, from anywhere between 5.8 percent and 7.2 percent, depending on the source. Morgan Stanley (NYSE:MS), for example, predicts 5.8 percent growth, while JPMorgan Chase & Co. (NYSE:JPM) has a more bullish prediction of up to 6.5 percent. Only the Centre for Monitoring Indian Economy Pvt. Ltd. thinks growth will top 7 percent in this current fiscal year.

Finance Minister P. Chidambaram initiated a series of measures last September to spur investment and reel in the fiscal deficit. The country has managed to bring down the deficit to 4.89 percent of GDP and is on track to bring it down to 4.8 percent in 2013-14, according to Indian Express.

© Copyright IBTimes 2024. All rights reserved.

-

Taiwan Hit By Dozens Of Strong Aftershocks From Deadly Quake

-

Gaza Health System 'Completely Obliterated': UN Expert

-

In Ecuadoran Amazon, Butterflies Provide A Gauge Of Climate Change

-

50 Years On, Vintage Vehicles To Reenact Portugal's Carnation Revolution

-

Conflicts Push Military Spending To 'All-time High': Report

-

'Thank You, America:' Zelensky And Netanyahu Applaud House Passage Of Foreign Aid Package

-

Women Journalists Bear The Brunt Of Cyberbullying

-

US Aid Shows Ukraine Will Not Be 'Second Afghanistan': Zelensky

-

Elon Musk's X Fights Australian Watchdog Over Church Stabbing Posts

-

Ukraine, Israel, TikTok: The Massive Aid Package Before US Congress