Mobile Payment Technology Like Apple Pay Could Entice Consumers To Spend More

It’s no wonder why retailers, credit card vendors and banks want shoppers to use mobile technology to pay instead of cash, credit or debit cards. Consumers who use smartphones when shopping tend to buy more, according to early studies of the budding mobile payment market.

“Right now it’s more convenient,” said George Peabody, a partner at Glenbrook, which researches the payment industry. “And convenience is really driving the bus right now.”

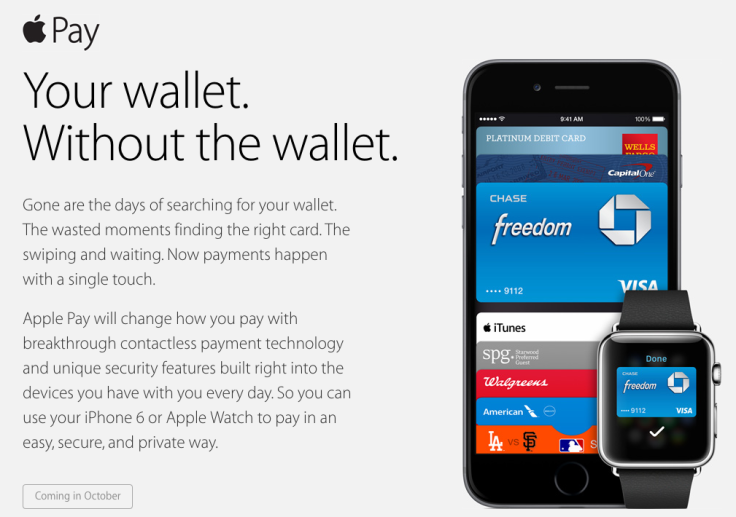

With Apple Inc.’s (Nasdaq: AAPL) new system Apple Pay, users with the latest iPhones will be able to tap and wave their phones to pay at major retailers like McDonald’s Corp. (NYSE:MCD) and Macy’s Inc. (NYSE:M) instead of digging through their pockets or purses for a traditional wallet. Credit and debit card info is stored on the phone and activated by the owner’s fingerprint but not shared with the retailer in an effort to protect it from hackers and fraud.

“We’re providing our customers with tools to make their financial lives better, including our 30 million digital banking customers,” said Brian Moynihan, CEO of Bank of America (NYSE:BAC), in a news release about Apple Pay. “For them, better means simple and convenient.”

Security concerns and lack of widespread in-store equipment has hindered the mobile payment market so far, Peabody said.

But Pew Research and Elon University have predicted that by 2020, mobile wallets will become the preferred method of in-store and digital payments, “nearly eliminating the need for cash or credit cards.”

Cutting the time and fuss it takes to complete a transaction tends to increase consumer spending, and that means higher revenues for stores, card vendors and banks.

Frequent smartphone shoppers, those using mobiles to shop online, spent 50 percent more on health and beauty items and 40 percent more on appliances like televisions and microwaves than shoppers who rarely or never shop on their phone’s web browser, according to the Shopper Marketing Council.

In the last five years, mobile-based transactions have grown an average 118 percent per year, according to researchers at Merchant Warehouse. In 2011, the average mobile payment user spent $61 on each transaction, and that number is projected to grow to $1,080 by 2017, Merchant Warehouse said.

Jenn Reichenbacher, senior developer of corporate marketing at Merchant Warehouse, said consumers are likely spending more using mobile payments rather because of the rewards offered than the convenience. Mobile payment apps LevelUp and Softcard, which used to be called Isis Wallet, both offer rewards and coupons when users pay with the apps.

"When consumers receive a reward or discount, they’re not only more likely to spend more during the transaction, but they’re also more likely to become a loyal and return again for a repeat purchase," she said.

The effect could be similar to what behavioral economists at Massachusetts Institute of Technology hailed as the credit card premium -- consumers’ willingness to pay more when using a credit or debit card instead of cash. The business information firm Dun & Bradstreet illustrated the credit card premium by finding that McDonald’s customers using credit cards paid an average $7 per visit while those using cash only $4.50.

According to Thrive Analytics, 75 percent of digital wallet transactions are less than $10, for items like coffee, drinks and snacks. Starbucks, which has an app that processes mobile payments in the store, reported more than $1 billion in mobile transactions last year.

About 90 percent of mobile payments in 2013 were those made shopping online, according to Forrester Research, but the firm expects mobile payments in stores, currently the smallest category of mobile spending, to grow the fastest. The category will account for $41 billion in 2017, and the mobile payment market overall will reach $90 billion that year, Forrester said in 2013 when Isis Mobile Wallet (now Softcard), First Data Mobile Pay and others dominated the market.

"Whether you pay with plastic or with a mobile app, I think at the end of the day you have a finite amount of money to spend," said Georges Pigeon, a Montreal-based advisory services, transactions and restructuring partner at consulting firm KPMG. "The bigger question is, will cash be replaced?"

For now, Americans are still using cash for two-thirds of transactions under $10, the majority of spending activity, though only 14 percent of the value of all transactions, according to the Fed. Electronic methods, like paying bills with a checking account, accounted for about a third of transactions over $100.

© Copyright IBTimes 2024. All rights reserved.

-

French Air Traffic Controller Strike Threatens Flight Chaos

-

Azerbaijan Says 'Closer Than Ever' To Armenia Peace Deal Amid Border Talks

-

How UK's Biggest Water Supplier Sank Into Crisis

-

Taiwan Hit By Dozens Of Strong Aftershocks From Deadly Quake

-

Gaza Health System 'Completely Obliterated': UN Expert

-

In Ecuadoran Amazon, Butterflies Provide A Gauge Of Climate Change

-

50 Years On, Vintage Vehicles To Reenact Portugal's Carnation Revolution

-

Conflicts Push Military Spending To 'All-time High': Report

-

'Thank You, America:' Zelensky And Netanyahu Applaud House Passage Of Foreign Aid Package

-

Women Journalists Bear The Brunt Of Cyberbullying