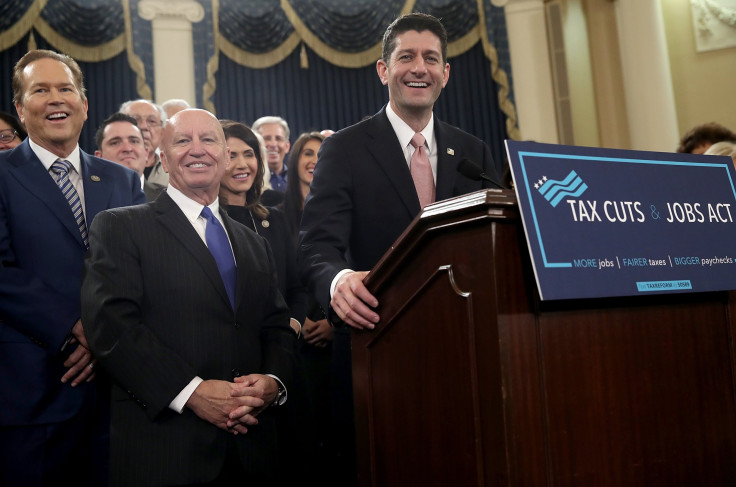

Paul Ryan And Top Republican Lawmakers Could Reap Personal Windfall From New Real Estate Tax Breaks

As Congress races to finalize a landmark $1.4 trillion tax bill, key Republicans legislators directly overseeing the initiative could reap a personal windfall from provisions designed to reduce levies on so-called “pass-through” income, according to federal records reviewed by International Business Times. Those lawmakers — including U.S. House Speaker Paul Ryan — together have tens of millions of dollars invested in scores of real-estate related pass-through corporations and partnerships, collectively earning them millions of dollars of annual income that could be partially exempted from taxes, depending on how the final legislation is structured.

IBT reviewed the most recent personal financial disclosure records of 44 Republican lawmakers in the House and Senate leadership, as well as on the chambers’ committees that have overseen the tax bill. In all, 13 of those lawmakers have between $36 million and $163 million worth of ownership stakes in 40 real-estate or property-related partnerships, corporations and investment trusts. In 2016, those 13 legislators earned between $2.6 million and $16 million of annual income from those investments. Those kind of “pass-through” earnings — which experts say disproportionately flow to high-income households — could get new exemptions under the legislation that Congress is now finalizing.

The original House and Senate bills both aimed to reduce levies on income generated by partnerships that pass their income through to their investors. Both bills, though, included some limits on the tax breaks for pass-through income -- and the final legislation now being worked out in Washington could still eliminate, reduce or cap those tax cuts. Congressional negotiators are reportedly close to agreeing to a 20 percent deduction for pass-through income, with Republicans arguing the deductions would help small businesses.

If the GOP ends up applying a 20 percent deduction to all such passive real-estate income, those 13 legislators who have overseen the tax bill could be permitted to deduct a total of between $520,000 and $3.2 million from their taxable income each year, based on their 2016 filings.

"Congress is not just rigging the system for the idle rich in return for campaign contributions, but is made up in no small part of the type of rich people who want the system rigged,” Jeff Hauser, director of the Revolving Door Project, told IBT. “Too many things which sound like legally problematic conflicts of interest are often legal. The data illustrate why this rushed process is so corrupt. Before passing this bill, there should be time for constituents to force their representatives to justify why their conflicts of interest do not invalidate the broader tax cut bill."

‘Pass-Through Entities Likely To Benefit’

Pass-through business structures are prominent in real estate investing. By one estimate of IRS data, more than a third of all income generated by pass-through entities come from real-estate related businesses.

In general, the tax bills passed by the House and Senate aim to reduce levies on income from these entities, such as limited partnerships (LPs), limited liability corporations (LLCs) and S-Corporations. These vehicles are attractive to business owners because they aren’t subject to corporate taxes. Instead, the business income is “passed through” the entity to its owners, who then pay individual income taxes on that income. Real Estate Investment Trusts (REITs), publicly traded pass-through entities that own income-producing real estate, are also eligible for the tax break.

Under current law, the highest income earners can end up having their pass-through income taxed at the highest 39.6 percent rate. But the House- and Senate-passed tax bills are both designed to reduce taxes on that income, with the goal of giving pass-through entities a tax cut comparable to the bill's other reductions in corporate rates.

“Passive investors in pass-through entities (are) likely to benefit substantially from lower rates under the House plan, but their eligibility for tax deductions are limited by wage provisions under the Senate proposal,” noted a recent report from researchers at real estate services firm Cushman & Wakefield.

How much of a windfall the new tax bill ultimately provides to investors in pass-through vehicles — including those in Congress — will be contingent on any caps or limits lawmakers place on the deductions.

The Senate bill allows 23 percent of pass-through income to be deducted from taxable income, but would limit the deduction to 50 percent of the amount the partnership pays out in wages. The House bill has fewer limits, and instead of giving the tax break as a deduction, simply caps taxes on pass-through income at 25 percent.

Both bills also included other limits on deductions for “professional services” such as lawyers and accountants who operate their businesses as pass-through entities. However, the House-Senate conference negotiators are under no obligation to incorporate any of these limits into the final bill.

A House of Landlords

The current Congress that is sculpting the final pass-through provisions is filled with Republican lawmakers who have income-generating ownership stakes in real-estate-related partnerships. That includes lawmakers on the Senate Finance Committee, House Ways and Means Committee, and House-Senate conference committee now ironing out the final bill.

For example, Tennessee Republican Rep. Diane Black serves on the conference committee as well as on the House Ways and Means Committee that oversaw the original House version of the tax bill. Black and her husband, the CEO of forensic science company Aegis Sciences Corp., co-own Ebon Falcon LLC, a real estate company that owns 12 properties including the Aegis building and several nearby properties, according to Rep. Black’s 2016 financial disclosure.

The properties, mostly in Nashville, appear to be commercial, and together they represent between $21.7 and $108 million in value and between $1.7 and $10.5 million in annual rental income. Black, who is Congress’ 11th-richest member, has a current net worth of $46 million, according to Roll Call.

Recently, IBT reported that Black’s former chief of staff has been lobbying the House on real estate issues this year on behalf of the National Association of Real Estate Investment Trusts.

Florida Republican Rep. Vern Buchanan is also on the Ways and Means Committee. Earlier this year, he sponsored standalone legislation to reduce the tax on pass-through entities, saying “it’s clearly time that Washington stopped punishing small businesses and started helping them.” Buchanan’s most recent financial disclosure forms show that he owns between $7 million and $32 million of investments in real-estate related partnerships. In 2016, he earned up to $2 million in annual income from those investments.

Family connections are also at play. For instance, Rep. Tom Reed (R-NY) — who sits on the House Ways and Means Committee that wrote the lower chamber’s version of the tax bill — is married to a partner at a real estate LLC, R&R Properties, LLC, from which he and his wife receive income of between $15,000 and $50,000 per year. Reed’s wife is also a partner at R&R Resource Recovery, LLC, the Reeds’ debt collection family business, which specializes in recovering medical debt. The business provides the Reeds with between $15,000 and $50,000 a year in income.

Paul Ryan’s Pass-Through Income

Speaker Paul Ryan has shepherded the tax legislation through the House, and he appointed the House members on the conference committee that is now finalizing the bill. He and his wife could also benefit from pass-through provisions in the tax bill.

According to the Wisconsin lawmaker’s 2016 financial disclosure, the couple holds interests in several LLCs reportedly run by Janna Little Ryan’s father, an oil and gas lawyer, including mineral rights and real estate firm Little Land Company LP, gravel rights business Blondie & Brownie, LLC and mining and mineral rights company AVA O Limited CO.

The companies reportedly lease land for mining and drilling to leading fossil fuel companies in Oklahoma and Texas including Chesapeake Energy, Devon Energy and ExxonMobil.

Ryan’s stakes in these partnerships are worth between $250,000 and $615,000, with annual profits of more than $115,000. Under the pass-through provision in the tax bill, the speaker could potentially deduct part of these earnings from his taxable income.

Wealthiest Lawmakers Could Benefit

IBT additionally calculated how much real estate some of the wealthiest Republican lawmakers own.

For example, during the fall, Wisconsin Republican Sen. Ron Johnson — the 26th-richest member of Congress — withheld his support for the bill, leveraging his vote to pressure lawmakers to add provisions to the bill increasing tax breaks for investors in pass-through entities. The most recent federal records show Johnson has up to $30 million of ownership stakes in three LLCs that generate rental income. Johnson earned between $115,000 and $1,050,000 of income from those investments in 2016. Levies on that income could be reduced by the GOP’s pass-through tax provisions.

Similarly, Rep. Darrell Issa (R-CA), the second-richest member of Congress, is the owner of 11 different real estate partnerships that, in total, are worth between $21.5 and $103 million, and generate between $410,000 and $5 million in annual income. Dave Trott (R-MI), the seventh-richest member of Congress, has interests in two real estate LLCs worth between $6 and $27 million and generating between $1.1 and as $6.1 million in annual income.

Congress’ third-richest member, Rep. Michael McCaul (R-TX), has up to $750,000 worth of real estate partnerships, and Rep. Chris Collins (R-NY), the 20th-richest member, holds as much as $12.5 million in real estate partnership interests that delivers up to $350,000 in annual income.

Others who directly own residential rentals may also get a boost from the tax bill, which reduces the tax benefits of homeownership, eliminating the deduction for property taxes and lowering the limit on the mortgage interest deduction. This could drive up demand in the rental market, benefiting those who own rentals.

Some members of the conference committee generate income from their rentals, including Republican Rep. John Shimkus of Illinois, who owns a rental property worth up to $100,000 in Collinsville, Illinois and takes in between $15,001 and $50,000 per year in rent from his “second home” in Washington, D.C., which is worth up to $1 million.

Also on the committee, Rep. Greg Walden (R-OR) owns a “tower property” in his hometown of Hood River, Oregon with a maximum value of $500,000, generating up to $50,000 of income per year, as well as a “home lot” in Lake Havasu City, Arizona, which appears undeveloped, according to Zillow.

As the tax legislation moves ahead and its details are finalized, its most vociferous critics have continued to single out the tax cuts for pass-through income as a particularly problematic part of the overall legislation, which they argue is designed to redistribute wealth to the very rich. A recent study from researchers at the U.S. Treasury Department, the University of Chicago and the University of California-Berkeley underscores their argument.

“Pass-through income (is) especially concentrated among high-earners,” they wrote in their 2015 report for the National Bureau of Economic Research. “Relative to households in the bottom half of the income distribution, households in the top 1 percent of the income distribution are over 50 times as likely to receive positive partnership income. And the average top 1 percent household earns over 600 times the amount of partnership income as the average household in the bottom half. Overall, 69 percent of pass-through income earned by individuals accrues to the top 1 percent.”

© Copyright IBTimes 2024. All rights reserved.

-

Mideast-related Oil Price Spike Threatens 'Relatively Good' Economic Outlook: IMF Chief Economist

-

Wine Growers 'On Tip Of Africa' Race To Adapt To Climate Change

-

Despite Olympic Truce, Games Wrestle With Political Fallout

-

What Will The Fed Do With The Latest Inflation Numbers?

-

US Retail Sales Up More Than Expected In March

-

Australia's Great Barrier Reef Struggles To Survive

-

Alexandre De Moraes: Brazil Judge In Feud With Elon Musk

-

Paris 2024 Games Flame To Be Lit In Ancient Olympia

-

How The US Helped Counter Iran's Attack On Israel

-

How The Premier League Title Race Stands With Six Games To Go