The post-recovery US economy will still be weak and will get clobbered by commodities prices

By now, most smart money has typically pegged the US recovery in late 09, early 2010. ZH is somewhat dismayed to see the assumption being that once the economy gets going again, we're going to return to the '05-'07 levels of good times. However, we have to believe that we are merely going from disastrous to just kind of bad. Specifically, the next few years are not going to be pretty even once the deleveraging of the US economy is over. As we come out of it we're going to see a repeat of the infamous summer of '08 with oil hitting triple digits, except the header is likely going to be reflected across commodities not just oil. So, let's explore this idea...

THE US IS NOT RECOVERING INTO A POSITION OF STRENGTH

From a really macro view, 2000/2001 should have been the start of the corresponding secular bear market following the the post-'82 period but thanks to Greenspan's easy money, we managed to postpone the pain. The deleveraging that has occurred over this crisis can be viewed as correcting the past few years of easy money, but the underlying bear market still remains. The basis of the secular bear market is not particularly scientific, but given the 18 year movements from secular bull to bear to bull, etc. many were looking for the Internet bubble burst to merely be the start of the next secular bear market.

On a more specific level, it is very interesting to note Bernanke's views (and David Rosenberg's take on those views) on the recovery and the positioning of the US economy.

On the consumer side:

“… A number of factors are likely to continue to weigh on consumer spending, among them the weak labor market and the declines in equity and housing wealth that households have experienced over the past two years. In addition, credit conditions for consumers remain tight.

On unemployment:

“Even after a recovery gets under way, the rate of growth of real economic activity is likely to remain below its longer-run potential for a while, implying that the current slack in resource utilization will increase further. We expect that the recovery will only gradually gain momentum and that economic slack will diminish slowly. In particular, businesses are likely to be cautious about hiring, implying that the unemployment rate could remain high for a time, even after economic growth resumes.

On commercial real estate:

“Conditions in the commercial real estate sector are poor. Vacancy rates for existing office, industrial, and retail properties have been rising, prices of these properties have been falling, and, consequently, the number of new projects in the pipeline has been shrinking. Credit conditions in the commercial real estate sector are still severely strained, with no commercial mortgage-backed securities (CMBS) having been issued in almost a year.”

Finally, Rosenberg's summary of Bernanke's sentiment:

Bernanke knows any recovery will be fragile, at best The whole recovery story boils down to government stimulus, the arithmetic from lesser inventory withdrawal, a reduced drag from housing and hopes that overseas demand will underpin exports. While Bernanke did try and sound optimistic, something tells us that he knows that any recovery, when it occurs, is going to be fragile at best, unsustainable at worst. Invest accordingly.

We couldn't have said it better ourselves. The bottom line is, there are a number of factors coming into play that we simply do not see accounted for in the current recovery story. We have to agree with Rosenberg's assessment, particularly when you weigh the general sunny bullishness that Big Ben has exhibited (in comparison with the usual tempered language of central bankers).

COMMODITIES PRICES ARE GOING TO EXPLODE IN THE NEXT YEAR OR TWO

To be charitable, this is far from a controversial statement. However, despite the obviousness of it, we have to reiterate the point. There are two major factors that are going to make this time worse (or atleast different) in terms of commodity price shocks.

1) The US economy will not be leading the global economy out of the contagion

Pretty obvious, as we discussed above.

2) The US is consuming a lower market share of commodities, leading it to increasingly becoming a price-taker

Using the research we did into copper as an example, it's easy to see the shift and put some numbers on the anecdotal China gets larger picture. In just 3 years, the ratio of copper consumption in OECD:China:ROW went from 2:1:1 to 1.2:1.1:1.0. The specifics will vary from commodity to commodity but the larger trend remains.

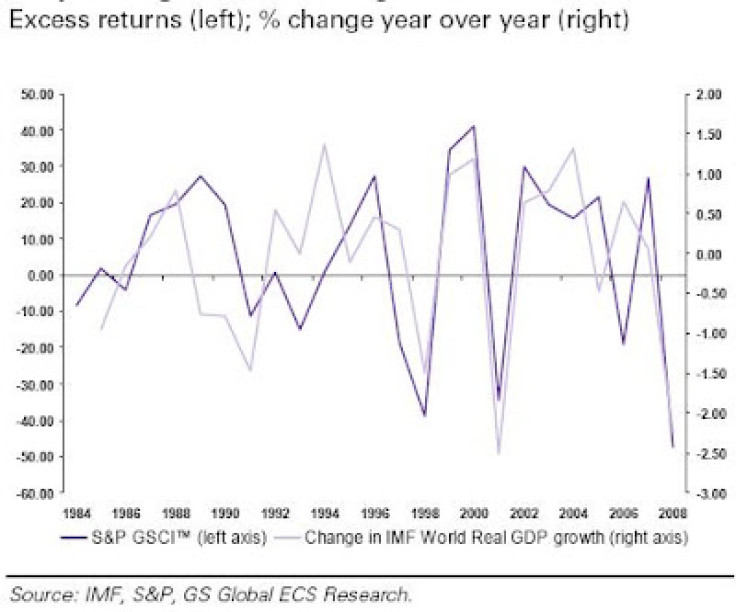

Commodity prices are highly responsive to the change of rate of GDP (as opposed to the actual level of GDP) and once we see the recovery kick in, prices will respond. Below, we see the correlation between commodities and rate of change of world GDP.

Thankfully, so far we have seen some respite following the dramatic crash of commodities last year (see below). However, a cursory glance is enough to tell that we shouldn't expect this to be a continuing dynamic in the larger economy; going from 1.0 to 1.6-1.7 in roughly 25 years (roughly a 2% clip) when the underlying is only increasing in industrial demand dictates a pretty strong signal that prices will continue to march back up.

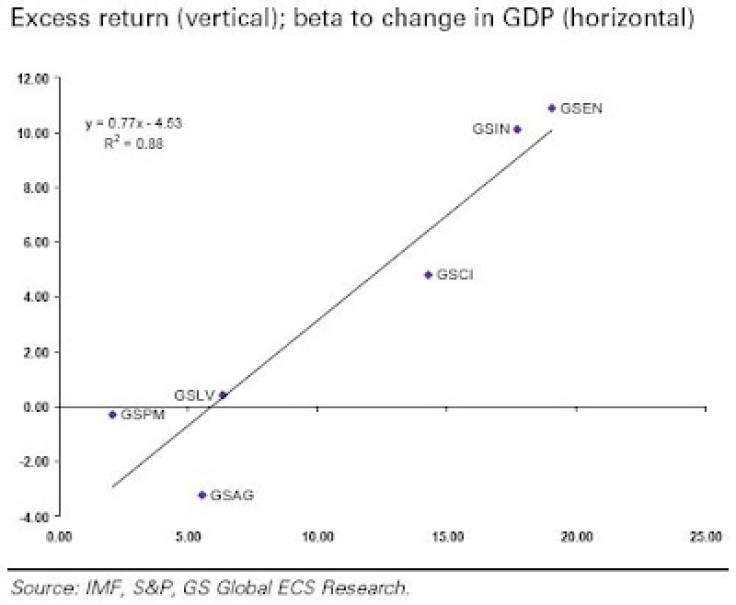

Finally to add to the pain, the most important commodities (industrials and energy) also happen to be the most cyclical/beta correlated. Basically, we will be paying higher and higher prices for important commodities that reflect a world getting rich faster than what we are actually experiencing.

Given that we have covered why the US may not be in the strongest position coming out of the contagion, it seems painfully obvious that there will be other countries that are better poised to put up the big growth numbers. That delta will be very painful to the US economy.

CONCLUSIONS

Ok, so we know the US economy is going to be running on fumes and commodities are going to get expensive - so what? Both messages have been tossed off the cuff by numerous talking heads but looking at it analytically and then combining the two leads to a very scary picture of what's in store. More specifically, the lab rats at ZH headquarters are now working on thinking about what price level action is going to look like, and what that implies for us as citizens first and investors second. We want to caution that this is more complicated than it initially seems as the kneejerk reaction to commodity price shock is stagflation - however, it would be short sighted to toss out that old chestnut without taking into account the massive market manipulations and macro shifts we have seen.

We welcome thoughts, comments, feedback, opposing publications. Additionally, any (good) pieces on price action movement/CPI predictions would be greatly appreciated - cornelius@zerohedge.com

-

French Air Traffic Controller Strike Threatens Flight Chaos

-

Azerbaijan Says 'Closer Than Ever' To Armenia Peace Deal Amid Border Talks

-

How UK's Biggest Water Supplier Sank Into Crisis

-

Taiwan Hit By Dozens Of Strong Aftershocks From Deadly Quake

-

Gaza Health System 'Completely Obliterated': UN Expert

-

In Ecuadoran Amazon, Butterflies Provide A Gauge Of Climate Change

-

50 Years On, Vintage Vehicles To Reenact Portugal's Carnation Revolution

-

Conflicts Push Military Spending To 'All-time High': Report

-

'Thank You, America:' Zelensky And Netanyahu Applaud House Passage Of Foreign Aid Package

-

Women Journalists Bear The Brunt Of Cyberbullying