China's Debt-crippled Evergrande Defaults: Fitch

Debt-crippled Chinese property giant Evergande has defaulted for the first time, Fitch Ratings agency said Thursday, as authorities scrambled to avoid contagion throughout the world's second biggest economy.

The Chinese government sparked a crisis within the property industry when it launched a drive last year to curb excessive debt among real estate firms as well as rampant consumer speculation.

Companies that had accrued huge debt to expand suddenly found the taps turned off and began struggling to complete projects, pay contractors and meet both domestic and foreign repayments.

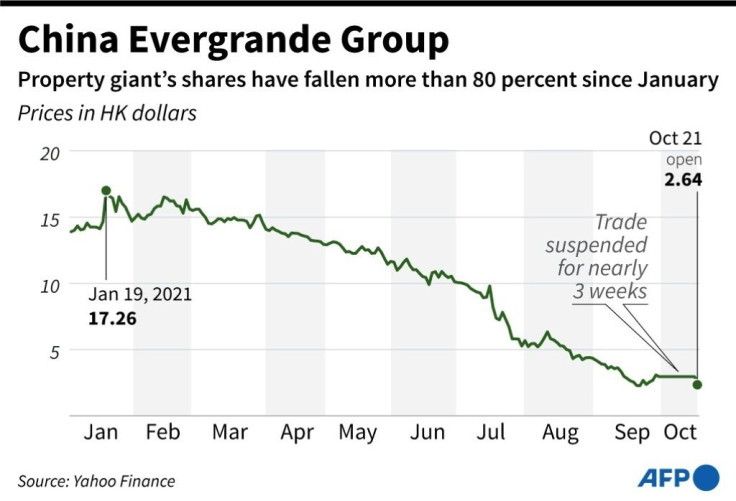

Real estate behemoth Evergrande had been the highest-profile firm to become embroiled in the crisis, struggling for months to raise capital to pay off $300 billion in debt.

On Thursday, Fitch confirmed the company had defaulted for the first time on more than $1.2 billion worth of bond debt, as it downgraded the firm's status to a restricted default rating.

Fitch also declared Kaisa, a smaller property company but one of China's most indebted, had defaulted on $400 million of bonds.

More than 10 Chinese real estate firms have now defaulted in the second half of this year.

But Ashley Alder, head of Hong Kong's Securities and Futures Commission, played down concerns that China's property sector woes could snowball into a something resembling the 2008 global crash.

"It's a significant event, you can't possibly underplay it, but it's basically not that category of event for the financial system," he told Bloomberg Television.

China's property sector is one of the main drivers of the nation's economy and keys to the wealth of the booming middle class.

Intent on maintaining "social stability", Beijing has been working to avoid a massive fallout from the collapse of Evergrande.

But it has eschewed a government bailout.

Instead, a "risk management committee" stacked with officials from state entities was last week sent in to clean up the current mess.

Yi Gang, governor of the People's Bank of China, said Thursday Beijing planned to handle Evergrande's future in a market-oriented way.

"The rights and interests of creditors and shareholders will be fully respected in accordance to their legal seniority," Chinese state media quoted Yi as saying in a pre-recorded video message to a top-level seminar in Hong Kong.

But even with those assurances, investors remain in the dark about what the future holds and what Beijing's overall plan is.

Neither Evergrande, nor Kaisa, have yet to make any comments on the default reports and what they plan to do next.

"In the next step, I think all the creditors will sue Evergrande," Chen Long, a partner at research firm Plenum told AFP, adding Fitch's announcement formalised what investors already knew about the defaults.

Evergrande will have "to enter a period of restructuring," he said, adding that while creditors will hope to secure assets on the mainland "I don't think it will be very successful".

Evergrande's troubles first surfaced this year when it detailed how heavily leveraged the firm had become.

The eye-watering figures shook China's credit markets because of the sheer size of the company and the potential fallout should it collapse.

Last month it missed its first foreign bond repayment but there was a 30-day grace period attached. That ran out on Tuesday with some bond owners complaining they had yet to be repaid.

Questions had swirled over whether Evergrande is simply too big to be allowed to fail, given its collapse could send shock waves through the wider Chinese economy.

But it become increasingly clear in recent days that Beijing was willing to close the chapter on the 25-year-old real estate empire that has typified China's breakneck growth in recent decades.

After Evergrande said Friday it may not be able to meet its financial obligations, the government summoned the company's founder, Xu Jiayin, and the new risk management committee was announced.

Financial media in Hong Kong have reported that Xu, a billionaire who is also known as Hui Ka Yan in Cantonese, has been selling some of his own luxury assets to raise funds.

According to Bloomberg News, before Thursday, at least 10 lower-rated real estate firms have now defaulted on onshore or offshore bonds since the summer.

Before Thursday, Chinese borrowers had defaulted on a record $10.2 billion of offshore bonds, Bloomberg had reported, with real estate firms accounting for 36 percent of those non-repayments.

© Copyright AFP 2024. All rights reserved.

-

IMF Says Global Debt Levels Face 'Great Election Year' Risk

-

Divisions Among Colombia's FARC Dissidents Complicate Peace Talks

-

French Far Right Gets Youthful Vibe With 28-year-old Leader

-

US Fed's Powell Says Inflation Fight May Take 'Longer Than Expected'

-

Mideast-related Oil Price Spike Threatens 'Relatively Good' Economic Outlook: IMF Chief Economist

-

Wine Growers 'On Tip Of Africa' Race To Adapt To Climate Change

-

Despite Olympic Truce, Games Wrestle With Political Fallout

-

What Will The Fed Do With The Latest Inflation Numbers?

-

US Retail Sales Up More Than Expected In March

-

Alexandre De Moraes: Brazil Judge In Feud With Elon Musk