JD.com Earnings: 352 Million Active Users Drove 16% Sales Growth

China-based online retailer JD.com (NASDAQ:JD) reported fourth-quarter results last week. The company overcame soft demand for big-ticket electronics and home appliances to produce 16% sales growth in a wide range of lower-priced products.

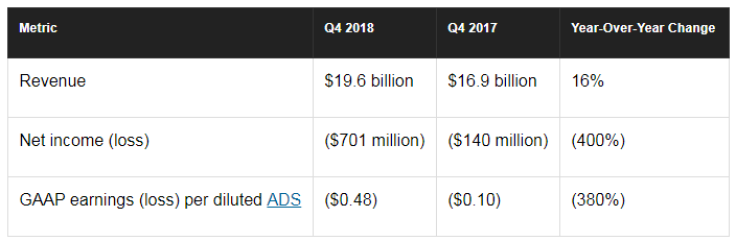

JD's fourth-quarter results: The raw numbers

What happened with JD this quarter?

- JD's management had expected to report roughly 20% sales growth in the fourth quarter, measured in constant currencies. From that currency-agnostic angle, the company's actual sales growth landed at 22%.

- The company managed 352 million active user accounts in the fourth quarter, a 20% year-over-year increase.

- 2.6% of JD's incoming revenues were funneled into technology and content expenses, up from 1.9% in the year-ago period. The company is making a concerted investment in "top R&D talent and technology infrastructure." The booming R&D budgets should stabilize in 2019.

- The gross market value, or GMV, of JD's total retail and marketplace operations added up to $75 billion in the fourth quarter, 28% above the year-ago reading. JD will stop publishing this data point on a quarterly basis, saving its GMV data for each fiscal year's full-year report. Management claims that JD's growing services revenues are making the GMV metric less useful, and this model matches the reporting habits of fellow e-commerce titan Alibaba (NYSE:BABA). For the record, JD's full-year GMV stopped at $250 billion in 2018. Alibaba's latest available GMV data stood at $768 billion for the fiscal year that ended in March 2018.

What management had to say

In a conference call with financial analysts, CEO Richard Liu highlighted the diversifying nature of JD's business model.

"During the fourth quarter of 2018, our net revenues grew 22.4%, a solid performance on top of an exceptionally strong fourth quarter in 2017 despite relatively soft consumption in large ticket electronics and appliance categories," Liu said. "Revenues from general merchandise categories grew 38% during the quarter, driven by home goods, skincare, and cosmetics categories. In addition, fulfilled marketplace GMV again grew over 40% year-over-year, as we continue to improve marketplace operations."

Furthermore, JD's service revenues grew nearly 46% thanks to a thriving advertising service and a strong interest in JD's third-party logistics program. So the company reduces the financial damage from slow sales in some key product categories by throwing its weight behind other product categories with a healthier outlook.

Looking ahead

For the first quarter of 2019, JD's revenue guidance points to roughly 20% year-over-year growth at approximately $17.5 billion. CFO Sidney Huang was "cautiously optimistic" regarding accelerated growth in the second half of the new fiscal year as the Chinese government's recently announced business-friendly policies start to take effect. The company is also increasing its marketing and infrastructure investments in smaller Chinese cities, without taking anything away from the saturation JD applies to the largest metropolises. In other words, the huge R&D growth of 2018 should shift into a heavier emphasis on sales and marketing in 2019.

This article originally appeared in the Motley Fool.

Anders Bylund owns shares of Alibaba Group Holding. The Motley Fool owns shares of and recommends JD.com. The Motley Fool has a disclosure policy.

-

IMF Says Global Debt Levels Face 'Great Election Year' Risk

-

Divisions Among Colombia's FARC Dissidents Complicate Peace Talks

-

French Far Right Gets Youthful Vibe With 28-year-old Leader

-

US Fed's Powell Says Inflation Fight May Take 'Longer Than Expected'

-

Mideast-related Oil Price Spike Threatens 'Relatively Good' Economic Outlook: IMF Chief Economist

-

Wine Growers 'On Tip Of Africa' Race To Adapt To Climate Change

-

Despite Olympic Truce, Games Wrestle With Political Fallout

-

What Will The Fed Do With The Latest Inflation Numbers?

-

US Retail Sales Up More Than Expected In March

-

Alexandre De Moraes: Brazil Judge In Feud With Elon Musk