Non-GAAP Accounting (When Companies Get Creative With Their Financial Reporting) Faces Increased SEC Scrutiny

What Tesla Motors Inc. (NASDAQ:TSLA) has been doing with its lease program this year is a textbook example of how companies add revenue to their books in a way that doesn't comply with generally accepted accounting practices (GAAP).

Since the Palo Alto, Calif.-based maker of the Model S electric luxury sedan began leasing its vehicles earlier this year through a deal with U.S. Bancorp (NYSE:USB) and Wells Fargo & Co. (NYSE:WFC), it has reported tens of millions of dollars of “deferred” revenue and “deferred” gross profit.

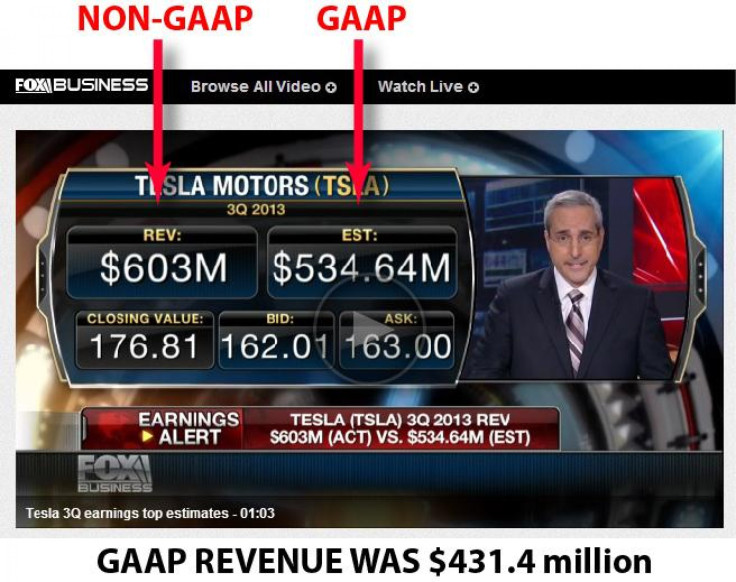

In the quarter ended Sept. 30, the company reported $171.2 million in revenue from this deferred lease accounting, compared with $431.6 million in revenue from selling its cars and other products and services.

In other words, the company is reporting revenue and income on what it expects to recover when it sells used Model S sedans from lease customers in the aftermarket (when they return their vehicles after 36 to 39 months). This creative accounting is an example of a non-GAAP (often called “adjusted” in the media) measure. Tesla isn’t violating any rules by doing this, because it offers both GAAP and non-GAAP accounting in its filings with the Securities and Exchange Commission.

Now, according to a report Wednesday in the Wall Street Journal, the SEC has established a task force to look into how companies report non-GAAP numbers, possibly as a lead into enacting enforcement measures. Speaking at an event hosted by the American Institute of Certified Public Accountants in Washington, D.C., David Woodcock, chairman of the SEC's new Financial Reporting and Audit Task Force, did not name any specific company. He did say one focus would be to examine if companies use financial terms with common meanings in different contexts to mislead investors.

The use of non-GAAP accounting is prevalent among, but not isolated to, technology startups, which often remove certain items like taxes in their non-GAAP accounting to turn a loss into a profit. Another common non-GAAP measure is reporting stock-based compensation expenses as gains in a quarter when insiders who have been given options to buy stock at below-market value (as part of their compensation) exercise them when the stock is rising.

The SEC task force was created in July and is comprised of 12 attorneys and accountants.

© Copyright IBTimes 2024. All rights reserved.

-

French Air Traffic Controller Strike Threatens Flight Chaos

-

Azerbaijan Says 'Closer Than Ever' To Armenia Peace Deal Amid Border Talks

-

How UK's Biggest Water Supplier Sank Into Crisis

-

Taiwan Hit By Dozens Of Strong Aftershocks From Deadly Quake

-

Gaza Health System 'Completely Obliterated': UN Expert

-

In Ecuadoran Amazon, Butterflies Provide A Gauge Of Climate Change

-

50 Years On, Vintage Vehicles To Reenact Portugal's Carnation Revolution

-

Conflicts Push Military Spending To 'All-time High': Report

-

'Thank You, America:' Zelensky And Netanyahu Applaud House Passage Of Foreign Aid Package

-

Women Journalists Bear The Brunt Of Cyberbullying