Taxpayer Loss From From General Motors (GM) Bailout Near $10 Billion And Rising

The taxpayer’s cost of rescuing General Motors Corp. (NYSE:GM) is about to top $10 billion, but GM’s TARP era isn’t over yet.

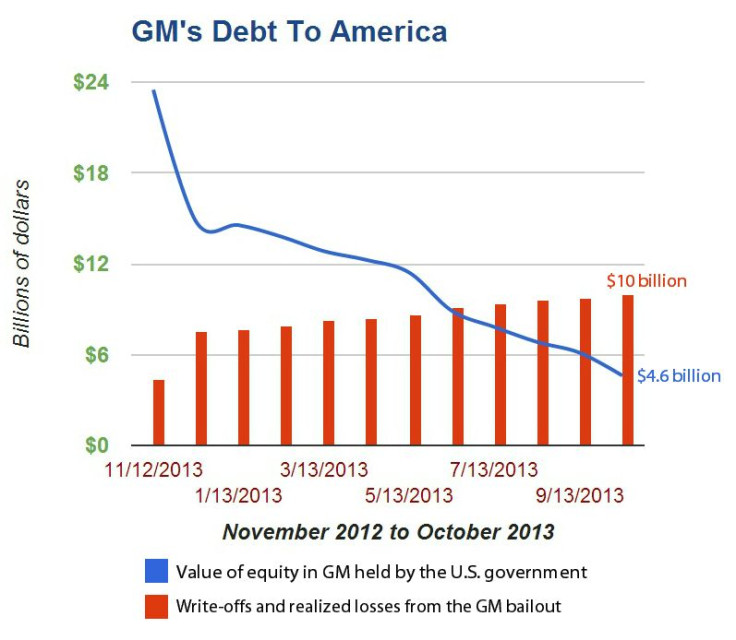

The U.S. Treasury Department’s latest estimate on the cost to the taxpayer for rescuing GM in 2009 is out and has officially hit almost $10 billion, and counting. The estimate was released Tuesday after markets closed. According to Deutsche Bank Markets Research, the government sold about 34 million GM shares in October, well above the monthly average since January of 12 million shares. This leaves about 67 million shares remaining.

This is the sum taxpayers have so far forked over to the private sector for rescuing the world’s second largest automaker in the wake of the subprime mortgage meltdown, the global recession and the ensuing auto industry crisis. More precisely, GM’s too-big-to-fail quality has cost taxpayers $9.98 billion as of this week, but that figure will grow.

Here’s why:

In the wake of the of the $51-billion bailout of GM as part of the massive $475-billion Troubled Asset Relief Program (TARP) that also rescued Chrysler (which cost the taxpayer $1.9 billion in unrecoverable losses), the U.S. government ended up owning nearly 61 percent of the new post-bankruptcy GM. The government has reduced its stake since, namely through the November 2010 IPO that sent GM back to the stock exchange; the sale of stock to GM in December 2012; and since then through a series of stock sales.

But the investment has not turned out as intended.

For one thing the effective original cost of U.S. government shares in GM was $43.52 per share, according to the U.S. Treasury. In other words, when the U.S. government started selling GM shares following the company’s 2010 IPO it would have had to sell at that minimum price to recover the remaining amount owed to it by selling its stake.

The problem is GM’s stock hasn’t touched $43 a share. The stock price peaked in January 2011 at $39.98 and bottomed out at $19.36 in July 2012. So each time the government has sold a share at under $43, the target value of the next share it sells has to be higher. GM’s stock is currently trading around $38.

This means that it will be impossible at this point for the government to recover what’s owed by GM. The best it can hope for is that GM’s stock stays as high as possible so it can recover as much of the remaining $4.6 billion in potentially recoverable equity.

GM itself isn’t in a great financial position to start paying out of its own balance sheet. As of its most recent quarter ended Sept. 30 GM had $28.6 billion in cash and $62.6 billion in short-term obligations. Analysts polled by Thomson Reuters expect GM to report 2013 net income of $5.6 billion, or $3.39 per share, on $155.2 billion in revenue.

That’s a lot of cash, but a company the size of GM with GM’s balance sheet, with an operating expense alone of $12.2 billion a month, GM needs as much money right now as it can get just to stay competitive and to keep its more than 200,000 employees employed.

© Copyright IBTimes 2026. All rights reserved.

- MOST POPULAR IN Business