All Systems Go For Fed's Liftoff Of U.S. Interest Rates

The Federal Reserve on Wednesday will close the door on its ultra-easy pandemic-era monetary policy and step up the fight against stubbornly high inflation with the first in what is likely to be a series of interest rate hikes

this year.

The shift, beginning with an expected quarter-percentage-point increase in the U.S. central bank's benchmark overnight interest rate, has been in the works since last fall and has already driven up the cost of home mortgages and other key types of credit in anticipation of what the Fed will do to curb prices that are rising at their fastest pace in 40 years.

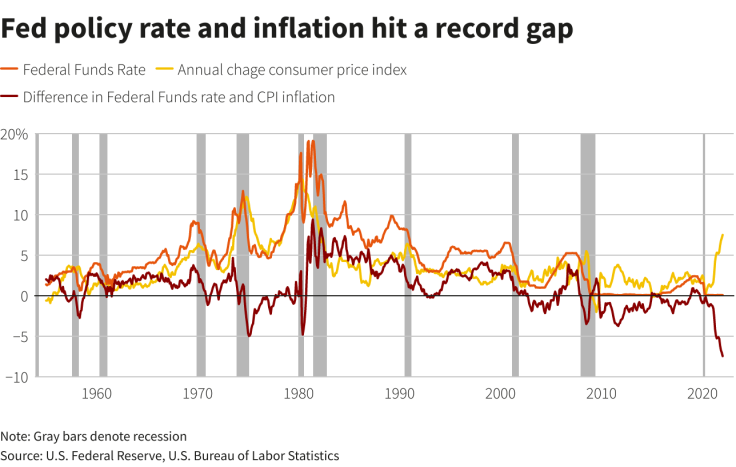

Graphic: Fed policy rate and inflation hit a record gap Fed policy rate and inflation hit a record gap:

Yet the urgency surrounding the Fed's policy meeting this week has intensified because inflation has shown no signs of easing and may even rise further on the back of Russia's invasion of Ukraine, which fueled an oil price spike this month.

The precise language of the Fed's new policy statement and the details of updated quarterly economic and interest rate projections will provide the first concrete guidance about how all that has influenced policymakers, and in particular whether it has rattled faith that the current economic expansion can stay on track even as inflation is driven lower.

U.S. retail sales data released on Wednesday showed what may be early evidence of consumers pulling back. Sales rose 0.3% in February, below the Reuters consensus forecast of a 0.4% gain, and spending on more expensive gas helped divert consumers' cash away from other goods. A majority of respondents in a recent Reuters/Ipsos poll said they would trim spending on restaurants and movies, to areas already hard hit by the COVID-19 pandemic, if gas prices continued to rise.

Fed Chair Jerome Powell, speaking to lawmakers in Congress earlier this month, said he felt it was "more likely than not that we can achieve what we call a soft landing ... which is get inflation back under control without a recession."

But he also acknowledged the central bank was in uncertain terrain, perhaps more reminiscent of the high-inflation days of the 1970s than of the weak inflation environment that has conditioned monetary policy since the early 1990s.

"We haven't faced this challenge in a long time," Powell said in testimony before the U.S. House of Representatives Financial Services Committee. "But we all know the history and we all know what we need to do."

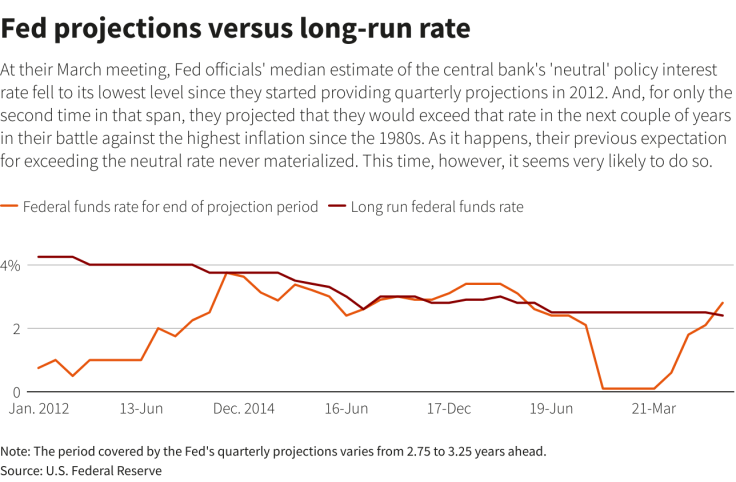

The new projections due to be issued alongside the policy statement at 2 p.m. EDT (1800 GMT) will show just how aggressive officials think they may need to be, and whether policymakers see the target federal funds rate rising to the sort of restrictive levels that could actually crimp the economy and increase unemployment.

Since the 2007-2009 financial crisis and recession, the Fed has penciled in those sorts of restrictive policies only once, in response to former President Donald Trump's run-up of deficit spending in 2017 and 2018, but rates never rose that high before the economy started to buckle.

Graphic: Fed projections versus long-run rate:

Inflation is now the motivation. The Fed's preferred gauge of price pressures is currently increasing at an annual rate that is triple the central bank's 2% target, and the environment of war, rising energy costs, and climbing wages has drawn parallels to the 1970s and early 1980s when the Fed pushed the economy into recession to break the cycle.

If the pandemic led to unpredictable economics, developments in Europe have made the situation almost Byzantine when it comes to forecasting.

The price of U.S. West Texas Intermediate crude, for example, rose about 33% to $123 a barrel in the days following Russia's Feb. 24 attack on Ukraine. On Wednesday, it was trading at about $98 a barrel.

But that decline in oil prices has been driven largely by new coronavirus-related lockdowns in China that could cause economic problems of their own - including more inflation.

The situation "couldn't be worse for the Federal Reserve, which is already chasing inflation for the first time since the 1980s. The disruptions we are seeing are adding fuel to a well kindled inflation fire," wrote Diane Swonk, chief economist at GrantThonton.

Powell "will be walking a tightrope, balancing the need to raise rates and rein in a more systemic rise in inflation with the need to avert a meltdown" if the central bank is seen raising rates so fast it might risk a recession, she added.

A 'NIMBLE' APPROACH

Powell is scheduled to hold a news conference half an hour after the release of the policy statement and projections. In addition to elaborating on the statement, he will likely provide an update on the discussions of when and how fast to reduce the Fed's roughly $8.5 trillion portfolio of government bonds and mortgage-backed securities, a second tool for tightening monetary policy that will be deployed later in the year.

Powell has used words like "nimble" to describe his approach to a situation in which policymakers may have to adapt on the fly, and in which they have been repeatedly fooled by economic developments from a faster-than-expected recovery to the slow return of workers to jobs.

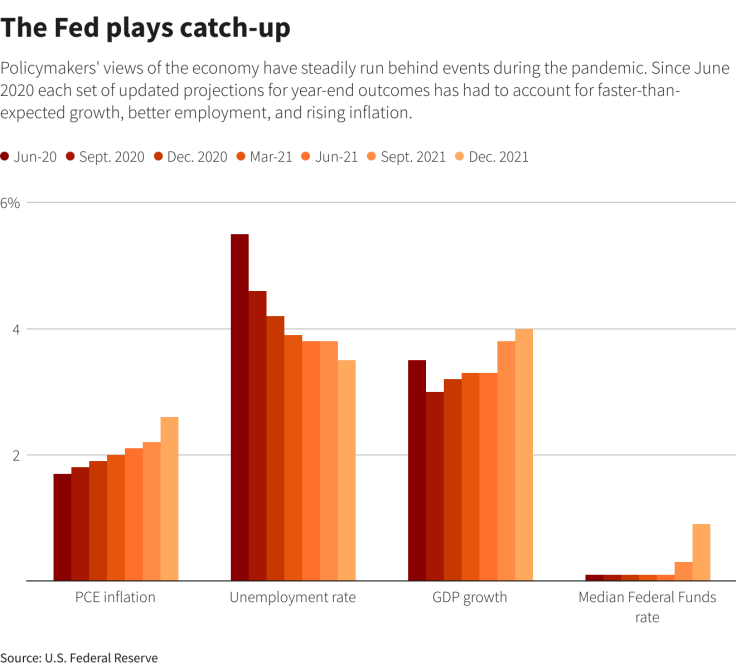

Graphic: The Fed plays catch-up:

The language of the new policy statement and the details of the new projections will, however, put the Fed's broader thinking on display.

As of December, most Fed officials felt they could get a grip on inflation with a relatively light touch that involved increasing the target federal funds rate, currently near zero, to just 2.1% by the end of 2024, a level still not considered restrictive by policymakers.

But policymakers at that point also felt inflation for 2022 would be just 2.6% and on its way down as the U.S. and world economies worked through the supply chain issues and other problems created by the pandemic - an outlook that also is proving out of step.

Given the level of inflation, "the message has to be at least somewhat hawkish," wrote Evercore ISI analysts Krishna Guha and Peter Williams, even if the volatile events of recent weeks mean officials will also want to stress "that now more than ever nothing is set in stone."

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets