In Canada, Hot Inflation Opens Rare Attack On Central Bank

The Bank of Canada has come under a rare attack from critics after misjudging inflation and locking itself into rigid forward guidance that prevented it from reacting swiftly as prices surged and Canada's economy began to overheat.

One of the world's leading central banks, it is now being forced to play catch-up, hiking interest rates more aggressively than originally expected just as Canadian household debt levels hit new highs, surging far above other G7 nations.

With a possible recession looming, the bank is facing questions from politicians, economists and even the general public about the opacity of its decision-making process and renewed calls for it to release minutes, a common practice among many of its peers.

For its part, the Bank of Canada has admitted missteps and is promising more transparency, including an analysis of inflation forecast errors, due in July.

But it still faces near daily attacks by politician Pierre Poilievre, the frontrunner to lead the opposition Conservative Party, who regularly takes to social media to accuse the central bank of being both incompetent and a government puppet.

He has also pledged to fire Governor Tiff Macklem if elected, a move that would require changing the law but that nevertheless underscores the level of discontent.

"Is there always room for more transparency? Probably. That's something that we're reflecting on right now," Senior Deputy Governor Carolyn Rogers told Reuters in an interview this month. "It's something we think about a lot."

The Bank of Canada, which is independent in setting policy, has not faced this level of political heat since the early 1990s, when then-Liberal opposition leader Jean Chretien railed against Governor John Crow over his high-interest rate policy.

Poilievre, not yet an opposition leader, is unlikely to become prime minister anytime before 2025, when the next election is due. But his attacks come at a time when public trust that the central bank will curb inflation is vital for the economy.

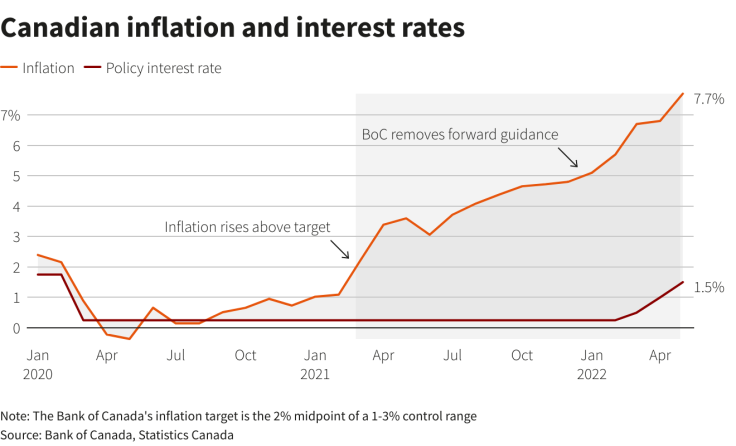

The Bank of Canada, like many other central banks, held that inflation was "temporary" or "transitory" into the fall of 2021, and did not start raising rates until March 2022, when inflation was already more than double the 2% target.

GRAPHIC: Canadian inflation and interest rates (

)

Prices are now rising at levels not seen since 1983, hitting 7.7% in May, and above target for 15 months. With the price of everyday essentials surging, the risk of inflation becoming entrenched is growing.

A Conference Board of Canada survey released this week found three-quarters of Canadians expect inflation to still be above target in three years. And the Bank of Canada's own data shows declining trust in its ability to keep inflation low and stable.

"How do we maintain credibility? The number one thing we do is we get inflation back to target and we're absolutely focused on doing that," Rogers said.

"It's not going to happen overnight," she added. "But we have laid on a path and we're on the job."

'A FAIRLY SERIOUS COMMUNICATIONS MISTAKE'

The slow start came in part because the bank locked itself into forward guidance in July 2020, promising to keep interest rates at rock-bottom levels until "the economic slack is absorbed," which was expected to take years.

"If you've got a mortgage or if you're considering making a major purchase... you can be confident rates will be low for a long time," Macklem said in July 2020.

Sticking to the forward guidance was necessary, said Rogers, because "that's how we know it'll work next time".

But doing so tied the bank's hands and forced it to react more slowly than it typically would have as parts of the economy overheated, according to interviews with economists and a former central banker.

Macklem also signaled he wanted a full labor market recovery before raising rates, which was later confirmed when the bank's policy mandate was renewed in December, creating an even more dovish outlook for rates.

David Dodge, Bank of Canada governor from 2001 to 2008, said Canadians were led to believe the central bank was not overly worried about inflation and therefore would hold interest rates "at essentially zero forever, come hell or high water."

That was "a fairly serious communications mistake," Dodge told Reuters.

Dodge and others Reuters spoke to all made it clear the central bank was correct to respond forcefully at the onset of pandemic and said the unprecedented nature of the crisis made outcomes difficult to predict.

"We got a lot right. We got some things wrong. We've been transparent about that," Rogers said. "Our job relies on our ability to forecast and in this environment forecasting has been a really big challenge for everyone."

STILL STIMULATING

Trudeau and Finance Minister Chrystia Freeland have defended the central bank's independence and attributed surging prices to global supply chain woes and the unexpected war in Europe.

"Nobody gets everything right," said a senior government source. "But what (the Bank of Canada) didn't get right was that (Vladimir) Putin was going to invade Ukraine."

Economists agree the war in Ukraine complicated the situation and drove inflation sharply higher, though it was already becoming persistent before the invasion. Complicating the situation, the central bank is now raising rates even as the federal government continues to unroll stimulus.

Freeland's office defends that choice, saying this year's budget is on "a path of swift fiscal tightening - particularly by the standards of our peers," a ministry spokeswoman said.

With markets betting on a 75-basis-point increase in July, economists say the aggressive tightening risks undermining the bank's credibility with a public promised cheap money but now facing surging debt servicing costs.

Canada's once red hot housing market is already showing cracks from higher interest rates, with sales plunging and prices falling off February's peak.

And the higher rates don't seem to be helping slow runaway prices, said Ottawa resident David Strva, adding he wasn't sure he trusted the Bank of Canada to get inflation back to target.

"If they're only increasing interest rates and that's the main control they have, I'm not sure how much that'll do," he said with a shrug. "Inflation is still going up."

One way to win back public trust is to release minutes of central bank meetings, said Derek Holt, vice president of capital markets economics at Scotiabank.

"The Bank of Canada says that it is consensus-driven, so if that's really true in reality, then they should have absolutely no problem disclosing how this consensus was achieved," he said.

For its part, the Bank of Canada says the fact it takes decisions by consensus is exactly why it does not need formal minutes, and that its quarterly monetary policy report statements "bring transparency to the deliberations."

Rogers said the bank does its best to "lay out the different perspectives" in its speeches and statements.

But so far, it is doing little to quell critics. Poilievre, a populist and Bitcoin enthusiast, continues to drive the narrative across social media, with tweets and Facebook posts that get thousands of likes from his half million followers.

"They did what Trudeau told them: print money for deficits, causing runaway inflation & a dangerous housing bubble," he wrote in a tweet earlier this month.

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Business