The Fed Wants To Cool The U.S. Housing Market. Here's What That Feels Like

In mid-April, months into an increasingly frustrating house hunt, Harsh Grewal and his wife settled on a place in a San Francisco suburb and were prepping a bid, above the listed price so they'd have a chance of besting other offers in one of the nation's hottest housing markets.

Then he checked his phone and saw several alerts, all touting reduced prices for other homes they'd been tracking. The Grewals pulled their offer and put their search on ice in hopes it was a sign the market was finally cooling. "I want to see where this goes, and where the dust settles," Grewal said.

That's exactly what Federal Reserve policymakers hope to see more of as they raise interest rates to bring down 40-year high inflation.

One leg of their effort is taking the heat out of the housing market, where low borrowing costs introduced to cushion the economy from the COVID-19 pandemic helped fuel a 35% rise in home prices over the past two years. While house prices are not part of the inflation indexes the Fed tracks, they do feed into other factors - such as rents - that are influential to inflation.

Rising rates mean borrowing for a house is suddenly more expensive. The 10-year Treasury note yield, a benchmark for mortgage rates, has risen on expectations of swift Fed rate hikes. The average 30-year-fixed home loan rate is now 5.37%, up more than 2 percentage points since the year began, according to the Mortgage Bankers Association.

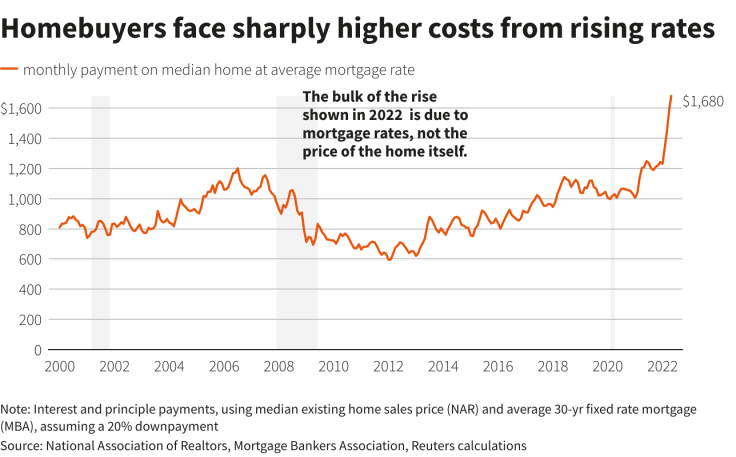

So buyers of a typical existing home, which went for $375,000 in March, will pay $440 more each month than they would have in December, if they put 20% down and borrow the rest at a fixed rate for a 30-year term.

Higher interest rates account for most of that. Meanwhile inflation is also driving up grocery bills and gasoline costs.

"The housing market is definitely out of whack," said Fed Governor Christopher Waller, who recounted last month how he sold his St. Louis home to an all-cash buyer with no inspection. "We'll see how the interest rates start cooling things off going forward."

New homebuyers face sharply higher costs

'AN INFLECTION POINT'

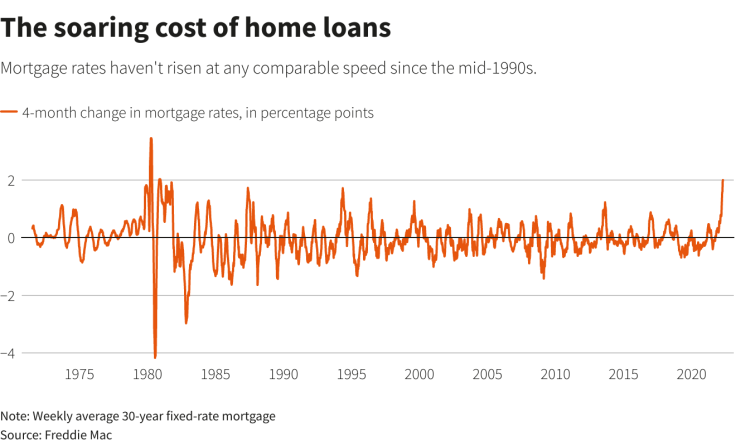

The last time mortgage rates rose this fast was in the spring of 1994. Total home sales fell 20% as the Fed lifted rates, and home price growth slowed.

Economists predict a sales drop and slowing price growth this time, too, perhaps to a roughly 5% annual rate by year end.

But an unprecedented collection of factors, including record-low housing stock, unusually high household savings, an extremely tight job market and increased worker mobility are creating crosscurrents that could blow that forecast off course.

Sales of previously owned homes were the lowest in nearly two years in March, according to the National Association of Realtors. Mortgage applications are down as well.

List-price drops like those the Grewals noticed are more common, accounting for 13% of homes for sale in the four weeks from mid-March to mid-April, according to real estate company Redfin, up from 9% a year earlier.

At the same time, mortgage applications remain above pre-COVID levels, and house prices hit a record as homes were snatched up typically within 17 days of listing.

Some of that could be a last-gasp effort of buyers, particularly those with pre-approved financing, racing to purchase homes before rates go even higher.

"The next couple of months things are going to heat up until we get to an inflection point," probably this summer, Zillow Economist Nicole Bachaud said.

The soaring cost of home loans

THIS TIME IS DIFFERENT?

The correlation between house price growth and mortgage rates, while still strong, has been declining though over the past 20 years, said Anne Thompson, a lecturer and research scientist at MIT who recently co-authored a paper with Yale University's Robert Shiller arguing that soaring prices do not appear to reflect a bubble.

"I wouldn't even necessarily call it a cooling, I'd call it a flattening of rates of appreciation, but not this year because there are still relatively low interest rates," Thompson said, noting that mortgage rates have historically been much higher.

Many regional markets remain very hot, particularly in the South, helped by buyers having more flexibility on where they work as well as strong wage gains amid a shortage of workers.

Those factors may also bolster housing sales even if higher rates take some of the steam out of price rises.

Rob Lubow, 35, and his husband worked remotely from their two-bedroom Austin, Texas, rental apartment until late last year when Lubow's firm began calling employees back to the office.

In January Lubow began looking for a new job that would let him work from home permanently. A month later he had one - and a 35% salary increase.

Austin home prices had climbed way above their $300,000 maximum reach. The median home price was $624,000 in March, up from $415,000 two years earlier, data from the Austin Board of Realtors shows.

Their remote-only jobs meant mobility, so last month they bought a three-bedroom house in Kingston, New York, for just under their budget. The median home price there is $280,000, according to Redfin, up almost 20% since last year.

"If people respond to higher housing costs by moving to more affordable places, that could lead to more home sales," Redfin Chief Economist Daryl Fairweather said.

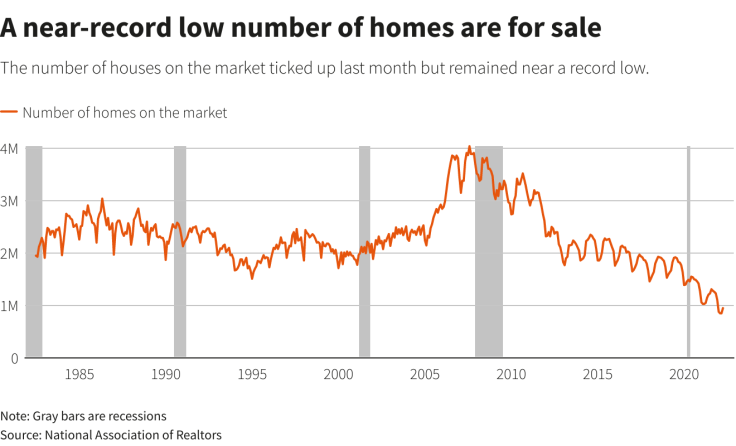

A near-record low number of homes are for sale

'INSANE'

Record low inventory over the past couple of years also means there is plenty of pent-up demand, particularly among Millennials ready to set up a home, whose share of purchases has been growing. But that is bumping up against Boomers, discouraged from downsizing by the rising costs of alternative housing, staying put and keeping the larger homes desired by younger people off the market at a time when too-few new homes are being built.

Meanwhile, data from the Realtors group shows the share of all-cash sales was the largest in nearly eight years in March, a sign supply is being gobbled up by institutional investors or second-home buyers.

Mike Wang, 33, works at a vitamin manufacturer and rents a Los Angeles apartment. He's had a number of promotions and now makes 50% more than he did three years ago. "Even with making more money than I could have hoped for when I was 20-something, house prices have far outpaced that - which when I think about that I'm like, holy cow, that is insane."

So Wang says he sees little choice but to wait in the hope prices slow as predicted and he can catch up enough to buy a house in a few years.

With so many people his age wanting to buy homes, and so few houses being built, he's not convinced it will happen that way.

"Having been surprised in the past, I wouldn't be surprised to see things buck all the analyst forecasts," Wang said.

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets