Infographic: High Prices & Low Rates Drive Mortgage Refinance Boom

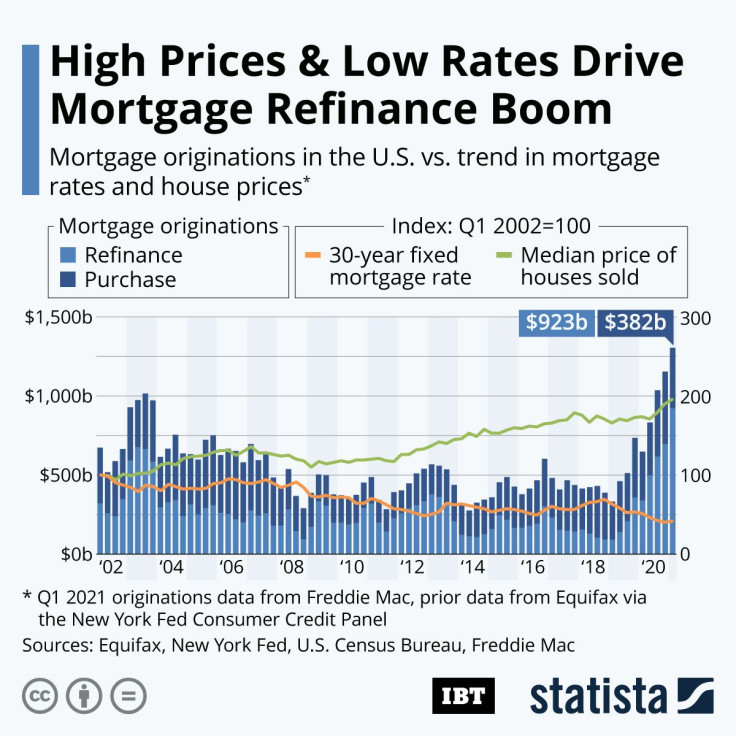

A combination of historically low mortgage rates and soaring home prices has led to a surge in mortgage refinances in the United States. According to Equifax data published by the New York Federal Reserve, mortgage originations nearly hit $1.2 trillion in Q4 2020, with refinances accounting for roughly 60 percent of that total. The refinance boom became even more apparent in early 2021, as existing homeowners refinancing their debt accounted for a whopping 70 percent of $1.3 trillion in mortgage originations in the first three months of the year according to Freddie Mac.

Homeowners are best situated to take advantage of the current market environment because they stand to profit from high house prices as well as low rates, while prospective buyers will see the positive effect of low mortgage rates at least partly canceled out by high home prices. Many homeowners even decide to take some cash when refinancing their mortgage, taking full advantage of their home equity. According to Freddie Mac, home owners cashed out $150 billion refinancing their mortgages last year, marking the highest volume since 2007.

As the following chart shows, mortgage refinances in Q4 2020 and Q1 2021 even surpassed the level seen during the refinance boom of 2003, albeit only in nominal terms. It also needs to be noted that back in 2003, only 30 percent of mortgage originations went to borrowers with excellent credit scores, while such super-prime borrowers accounted for more than 70 percent of origination volume in the past twelve months, making the current boom less worrisome than the 2003 refinance frenzy, which contributed to the financial crisis of 2008.

- MOST POPULAR IN Business