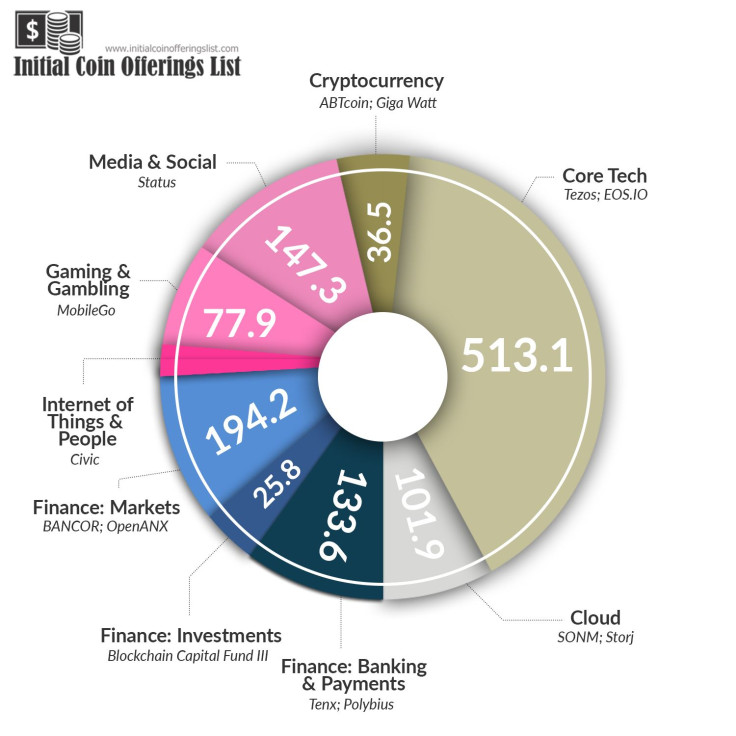

SEC Files Fraud Suit Against AriseBank ICO

Lawyers across the blockchain industry are grabbing stashes of metaphorical popcorn for 2018, because most expect the U.S. Securities and Exchange Commission to bring down the hammer on rogue token sales. Last week SEC chairman Jay Clayton delivered a passionate rebuke of the “disturbing” legal practices helping hundreds of startups raise money with initial coin offerings. The SEC promptly followed up by suing a Texas-based cryptocurrency banking company called AriseBank.

The SEC’s complaint against AriseBank, filed on Jan. 25, slammed the decentralized banking startup for using “social media, a celebrity endorsement, and other wide dissemination tactics to raise what it claims to be $600 million of its $1 billion goa l in just two months.”

In January, the startup promoted its ICO with questionable claims of acquiring two banks insured by the Federal Deposit Insurance Corporation. (The mergers were real, but the SEC stated both lacked FDIC insurance.) Plus, the SEC has repeatedly warned buyers against celebrity endorsements, such as the one boxer Evander Holyfield gave AriseBank, and other social media campaigns for unregistered securities.

It doesn’t matter whether the startup is selling a cryptocurrency or a traditional investment product, so far the SEC has been clear the same laws apply. A fraud by any other name will still land you in court. This banking startup failed to register AriseCoin with the SEC and even boasted on Facebook last October about being “geared up for the coming fight with the SEC." It’s no wonder why regulators singled out AriseBank. However, the case does raise questions about what it means to sell tokenized securities.

Most ICOs let almost anyone with enough ether tokens buy in without a background check or banking paperwork. If the tokens are later deemed securities, an investment product that can only be sold to accredited investors, these startups run the risk of winding up in court. Some projects are filtering prospective buyers with a simple agreement for registered tokens, aka SAFT. It basically collects all the same information a securities issuer might need without necessarily registering the token as a security before sale. If the startup manages to make a functional network or product before the SAFT agreement ends, that’s when investors get their digital loot. Likewise, the issuer will finally have to figure out if the token needs to be a registered security or if it can be sold to the public. The SAFT is a sophisticated way of preparing for the most difficult scenario and kicking the can down the road, hoping regulators will offer more clarity in 2018.

The nonprofit Coin Center in Washington, D.C. lauded this approach. Yet there are a wide range of opinions about the SAFT in the legal community. The SAFT is not an ironclad guarantee of compliance. Let’s imagine the SEC might offer clear guidance on what distinguishes a "utility" token product from a security token. What does selling tokens to accredited investors even mean?

The term “accredited” can be somewhat misleading. There is no investor driver’s test or license, at least not one buyers require for this context. In the U.S., an accredited investor is someone whose net worth exceeds $1 million, excluding the value of their primary residence. This terms also includes someone with an annual income of more than $200,000 for the past two years who has a reasonable expectation of reaping the same income this year. But just being rich doesn’t mean someone can automatically buy a security token. It’s all about the manner of sale.

For a 506B offering, these securities can’t be advertised to the general public. Generally speaking, the company can only sell these tokens to investors it already has an established relationship with. So in this case, the accredited investor has to be wealthy and connected. Then all the buyer does is check a box on a form to confirm he is rich enough to participate. This would mean ICOs couldn’t get celebrities to endorse startup tokens on social media or solicit the general public. The only way a cryptocurrency project could sell their securities to wealthy strangers, and continue the norm of mainstream marketing, is through a 506C. For this offering, the buyers can’t vouch for themselves. They need to produce bank statements, letters from an auditor, or some other proof that they’re wealthy enough to participate.

This is slightly more in line with the decentralization ethos, which upholds financial inclusion and engages buyers beyond the legacy venture capital bubble. But it still relies on wealth as a measure of intelligence and responsible decision-making. If cryptocurrency issuers really want to engage diverse buyers across a wide range of income levels, crowdfunding laws might provide a way. These token sales would need to aim for less money and faster tangible results. The issuer would also need to avoid language that portrays the token as an investment. Instead, cryptocurrency makers would stick to tokenized products and services.

People already fundraise for stuff like T-shirts and video games all the time. They just can’t promise the product will increase in value, yield dividends or suggest there will be a lucrative marketplace for re-selling said products. Crowdfunding projects raising up to a $1 million have a lot of flexibility. For Regulation A+ crowdfunding up to $50 million, there are significant accounting and reporting requirements even though the company doesn't have to jump through all the same hoops as a regular public company.

It’s impossible to say where the SEC will aim next. So far regulators appear to avoid cracking down on projects with cautious language, modest aims and a long-term approach to rolling out new technologies with baby steps. To the contrary, AriseBank’s 2017 Facebook post literally said their new type of digital asset was “out of the SEC's reach.” Startups that continue to flaunt existing laws risk regulators showing up on their doorstep with a lawsuit that, between the lines, reads: “You rang?”

Editor’s note: This is not investment advice or legal advice. Any following statements are not legal pronouncements or opinions regarding any specific project.

© Copyright IBTimes 2024. All rights reserved.

-

Senate Prevents Potential Air Travel Chaos, Reauthorizes FAA For Five-Years

-

Panama Papers Law Firm Boss Ramon Fonseca Dead

-

Pandemic Agreement Talks Go To The Wire

-

Low-cost MRI Paired With AI Produces High-quality Results

-

School's Out: How Climate Change Threatens Education

-

Hong Kong Demands Online Platforms Remove Banned Protest Song

-

2023 'Year Of Record Climatic Hazards' In Latin America: UN

-

Crypto Community Buzzes As Grayscale Withdraws Ethereum Futures ETF Application

-

Mongolia's Wildlife At Risk From Overgrazing

-

Milking Venom From Australia's Deadly Marine Animals