Analysis-Euro Back In Fashion As Traders Bet ECB Hawks Are Here To Stay

Investors are piling into derivatives linked to a rising euro, according to industry data and trading sources, as they bet the European Central Bank's hawkish tilt means the end to eight years of negative interest rates.

The euro has hit three-month highs near $1.15 since the ECB opened the door to a rate increase later in 2022 and said that a March 10 meeting would be crucial in deciding how quickly the central bank would reduce its bond-buying scheme.

ECB policymakers, including President Christine Lagarde, have since struck a more dovish tone. But many traders believe the shift in thinking is evident and markets must catch up with an ECB finally ready to tighten -- even if not as fast as rivals.

"There was not a lot priced in (to the euro) and people have been forced to look at the ECB and when it could tighten. German inflation is very high," said Antony Foster, head of G10 spot trading, EMEA, at Japanese bank Nomura.

The end of negative rates would mark a significant moment for euro zone markets, which have suffered persistent outflows and currency weakness that analysts attribute to sub-0% rates.

Those rates have made the euro a favourite for hedge funds to engage in lucrative carry trades -- the equivalent of borrowing in low-yielding currencies to invest in relatively higher-yielding ones.

A strategy of borrowing euros and investing them in U.S. dollars, Australian dollars and sterling posted a return of 5.3% last year, the highest since 2015, according to Refinitiv data.

Vasileios Gkionakis, head of European FX strategy at Citibank, said that the mentality of regarding the euro as a cheap currency to borrow was beginning to disappear.

"The ECB decision was a game changer for the euro," he said. "While we don't expect the euro and rest of the world yield differential to shrink dramatically, it is a big change in sentiment."

Nomura's Foster said clients had been buying large numbers of euro call options -- which give traders the right to buy euros in future at pre-determined prices -- between 1-month and 1-year maturities.

This includes call options on euro/dollar, on euro/Swiss franc and against Britain's sterling, which had hit a two-year high versus the single currency before the ECB meeting.

"The BoE seems to have moved early and that's been priced. But there could be a lot further for euro pricing to go," Foster added, referring to the Bank of England's rate increases in December and this month.

Industry data shows a shift in positioning in derivatives markets on euro/dollar -- a currency pair that has been stuck in a relatively tight trading range since 2015, frustrating bank traders that profit from higher volatility.

Three-month risk reversals on euro/dollar, a ratio of calls to puts on the single currency, have bounced from -0.7 to -0.2 this week, the highest level since July.

MORE MOMENTUM

Not everyone is bullish on the euro, and Thursday's forecast-beating U.S. inflation reading has markets once again betting on even faster tightening in the United States.

Analysts at HSBC argue that the United States has higher growth and high inflation that justifies "persistent tightening", whereas hiking euro zone rates would do little to resolve its stagflation.

Euro zone labour markets have much more slack to absorb workers before wage pressures build and ECB policymakers could easily flip back towards their decade-long dovish setting if inflation subsides.

The ECB will also be wary of any hawkish pricing that whacks up borrowing costs in the likes of Italy and Greece, where government bond yields have risen this month.

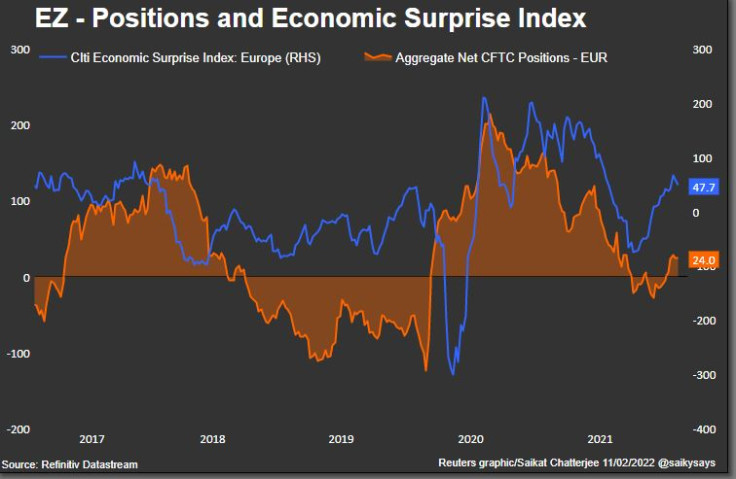

Speculative euro long positioning in futures markets has not increased in recent months, Commodity Futures Trading Commission data shows, even as economic data in the region has improved.

But it means the euro should have further to climb if positioning shifts.

Goldman Sachs this week said euro/dollar "fair value" was $1.30.

Faster Fed rate increases could hold back the euro in the short term, Goldman's analysts said, but they raised their year-end euro/dollar forecast to $1.20 from a previous $1.15, with a further rise to $1.25 predicted for end-2023 and $1.30 at end-2024.

(Graphic:

)

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets