Column-ECB Has Major Euro Headache; FX Market Offers No Relief: McGeever

The world's big four central banks are all in an unenviable position of fighting the highest inflation in decades without crashing their economies. From an exchange rate perspective, the European Central Bank's is the most unenviable of all.

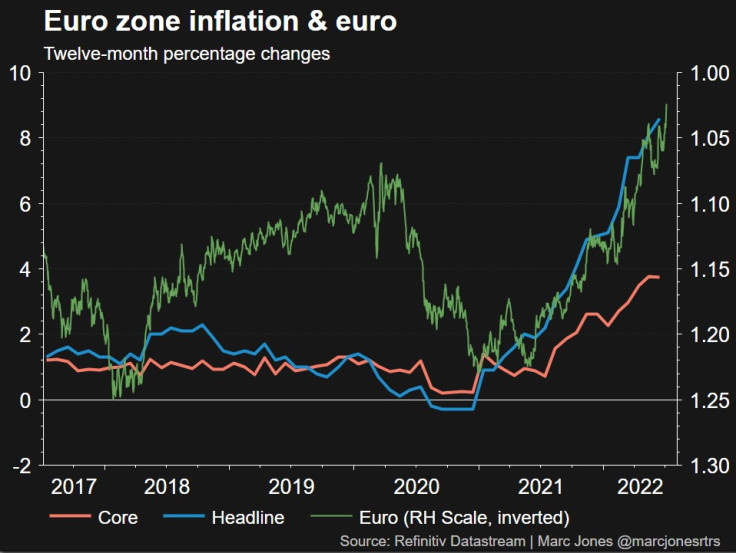

The euro sank on Wednesday to a 20-year low against the dollar of $1.0165, less than two cents from the psychologically significant barrier of parity. On Tuesday, its broader, real effective exchange rate hit its lowest since March, 2020.

The euro has fallen more than 10% against the dollar this year. While the real effective exchange rate has weakened much less, its fall of just under 3% in April-June was its biggest quarterly loss in over seven years.

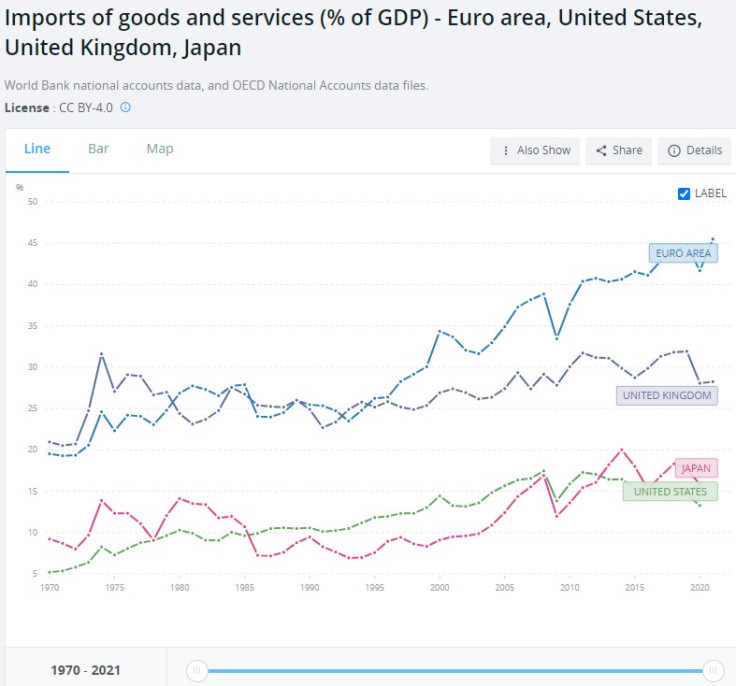

Exchange rate weakness boosts inflation in the euro zone more than it does in many other major economies. World Bank figures show that euro zone imports as a share of GDP last year were a record 45.5%, compared with 28% in Britain. Comparable figures for Japan and the United States in 2020 were 15.8% and 13.3%, respectively.

GRAPHIC:

Of course, this is offset by the weaker euro's boost to exports. But for a region that imported about 40% of its energy needs from Russia just before the war in Ukraine broke out, the terms of trade are deteriorating.

According to HSBC, a 10% fall in the trade-weighted euro adds around 1 percentage point to euro zone inflation after a year, while a similar rise in trade-weighted sterling adds 0.5 percentage point to UK inflation over the same period.

These rules of thumb tend to be better guides in more benign economic times, and relying on traditional economic models in the post-pandemic world is fraught with risk.

On the other hand, a flickering light may be better than no guiding light at all in such fog. The euro's rapid slide will be uncomfortable for the ECB.

"The euro is in a tricky position," notes Daragh Maher, Head of Research Americas at HSBC.

GRAPHIC:

GRAPHIC:

'UNBUYABLE'

No central bank wants a rapidly weakening exchange rate, but many are getting one, at least against the 20-year-high dollar. The Bank of England faces acute 'stagflation' risk and cable is below $1.20, while the Bank of Japan has seen the yen plunge to a 24-year low against the dollar and a 50-year low on a real effective basis.

Even the dollar itself faces potential downward pressure in the coming months as U.S. recession fears eat away at Treasury yields and erode market expectations for higher interest rates. So the euro is not alone.

Euro zone inflation is 8.6%, the highest since the euro was launched in 1999 and significantly above the ECB's 2% goal. The euro zone is facing recession risk, high and rising inflation, deteriorating external accounts, a crippling energy crisis, a cost of living squeeze, and 'fragmentation' risk from widening peripheral bond yield spreads.

GRAPHIC:

GRAPHIC:

Britain faces similar issues, even though possible UK fragmentation risk from Scottish independence may not be on the immediate horizon. But sterling has already fallen more than the euro this year. More bad news may be in sterling's price than the euro's.

The yen, meanwhile, could recover if global recession prompts investors in the world's largest creditor nation to bring money home, and traditional safe-haven demand for Japan's currency kicks in.

There is no obvious source of euro optimism. HSBC's Maher sees the euro weakening to $0.98 by the middle of next year, Jordan Rochester at Nomura predicts $0.95 by the end of this year, while Societe Generale's Kit Juckes thinks the euro is "effectively unbuyable" this summer.

"It's so unbuyable that a major political crisis in the UK isn't enough to drive euro/sterling higher," Juckes wrote on Wednesday, referring to a wave of resignations from British Prime Minister Boris Johnson's government.

ECB bulls rightly point out that the ECB pays attention to the broad, effective exchange rate, whose decline has been more gradual. And the Italian-German 10-year bond yield spread has narrowed 50 basis points in the last few weeks.

But the ECB under President Christine Lagarde's guidance must keep these spreads down. It remains to be seen if investors fully buy in, like they did with former ECB chief Mario Draghi's famous 2012 commitment to do 'whatever it takes to save the euro'.

"The market might be more skeptical this time around," Standard Bank's Steve Barrow wrote on Monday, adding that euro/dollar looks to be heading below parity.

Related columns:

- Hedge funds most cautious on dollar in 2 months (July 4)

- Upside down world of 'reverse currency wars' is real (June 22)

(The opinions expressed here are those of the author, a columnist for Reuters.)

(By Jamie McGeever; Editing by Bernadette Baum)

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets