Coronavirus Recession: If You Think The First Quarter Was Bad, Just Wait For The Second

KEY POINTS

- The contraction was led by a 7.6% drop in personal consumption, the largest plunge since 1980

- Major drops were felt in healthcare and purchases of motor vehicles and parts

- Fourth quarter GDP was revised to show an increase of 2.1%

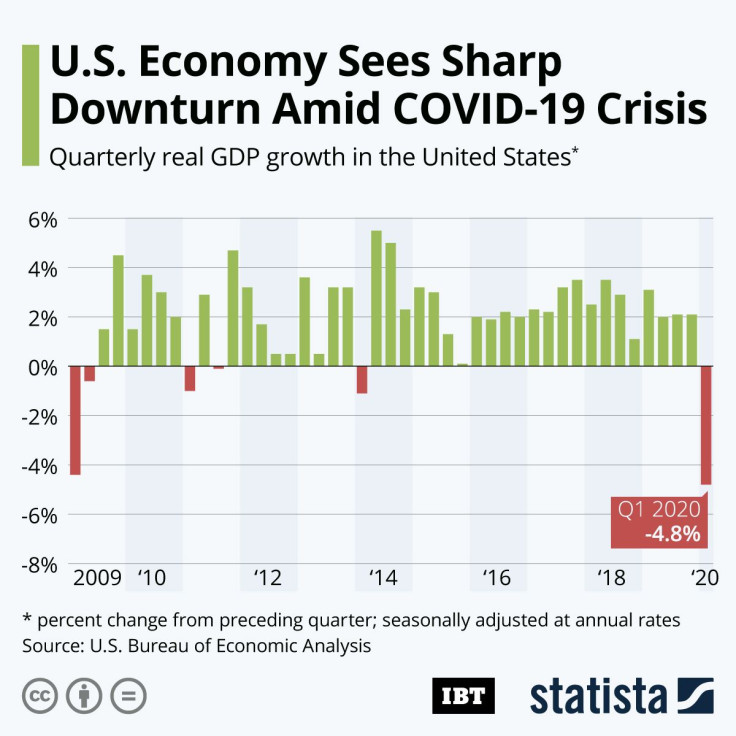

The federal government confirmed Wednesday what economists have been saying for weeks: The expansion is over and the U.S. economy is in recession as a result of the coronavirus pandemic. The Bureau of Economic Analysis reported the economy contracted 4.8% in the first quarter, the largest quarterly contraction since 2008 – and the second quarter is expected to be worse.

The government revised the fourth quarter gross domestic product to show it increased by 2.1%.

Technically, the definition of a recession is two quarters of contraction, but economists agree the stay-at-home orders have brought the U.S. economy to a virtual halt. The only questions are how severe the downturn will be and how long it will take to recover.

“The decline in first quarter GDP was, in part, due to the response to the spread of COVID-19, as governments issued ‘stay-at-home’ orders in March,” the bureau said in a rare statement. “This led to rapid changes in demand, as businesses and schools switched to remote work or canceled operations, and consumers canceled, restricted or redirected their spending.”

The numbers will be revised at the end of May.

The announcement came as the Federal Reserve was wrapping up its regular two-day meeting.

A 7.6% reduction in personal consumption expenditures drove the contraction, led by drops in services led by healthcare and a fall in goods purchases led by motor vehicles and parts. The plunge was the largest decline since 1980. Government spending also fell markedly ahead of passage of more than $2 trillion in coronavirus relief programs. A $484 billion package was approved last week and negotiations are underway for yet another measure.

Grant Thornton chief economist Diane Swonk lamented the government’s response to the virus so far, focusing on Republican reluctance to provide support to state and local governments that have been left primarily on their own to battle the pandemic.

State and local employment is key to a more robust recovery or a deeper recession. Congress has the power to decide how much they really want to get the economy going again.

— Diane Swonk (@DianeSwonk) April 29, 2020

What keeps me awake at night besides the obvious fear of contagion in my own family?

— Diane Swonk (@DianeSwonk) April 29, 2020

The inability of our elected officials to course correct and provide support were it is needed in a faltering economy.

One thing this crisis has given us is foresight - use it.

Cailin Birch, global economist at the Economist Intelligence Unit, said the second quarter figures will be much more meaningful, reflecting the full impact of the pandemic.

"The real figure to watch will be second-quarter GDP, as much of the negative economic impact will be felt in April-June. Early indicators are flashing strongly negative," Birch wrote ahead of Wednesday’s release.

“The economy will continue to fall until the country opens back up,” Chris Rupkey, chief economist at MUFG in New York, told Reuters. “If the economy fell this hard in the first quarter, with less than a month of pandemic lockdown for most states, don’t ask how far it will crater in the second quarter.”

The White House already is bracing for a “big negative number” in the second quarter and projecting unemployment as high as 20% -- a level not seen since the Great Depression. More than 26 million Americans have filed unemployment claims since mid-March when stay-at-home orders started taking effect, wiping out all the gains made since the Great Recession. At the same time, administration officials are predicting a sharp rebound in the third and fourth quarters.

"The way we've been thinking about this based on evidence from around the world is that each week of lockdown probably knocked off between 0.5 and 1 percentage points off annual growth," Michael Grady, chief economist at Aviva Investors, told CNN.

Goldman Sachs economist Spencer Hill said in a note the initial estimate is likely much more optimistic than the reality.

“Reflecting the onset of recession in the U.S. and the scope for additional economic measurement challenges unique to the coronavirus, we believe the wedge between growth data and economic reality is large and rising,” Hill wrote in a research note.

© Copyright IBTimes 2026. All rights reserved.

- MOST POPULAR IN Business