Hedge Fund Elliott Chases Oil And Gas Deals, Bucking Wall Street

Energy bankers who lost one client after another when poor returns pushed many investment firms out of the U.S. oil patch got a welcome email earlier this year.

Elliott Management, a hedge fund founded and co-led by billionaire Paul Singer and best known for its activist investing, wrote to the bankers in January inviting them to pitch opportunities to acquire U.S. oil and gas acreage, according to people familiar with the matter.

"They wanted to hear about everything," one banker who attended a meeting with Elliott said, referring to opportunities in U.S. shale basins.

It is a contrarian strategy; many investment firms have exited the sector, burned by big losses from when energy prices collapsed, most recently in 2020 when concerns over the COVID-19 pandemic briefly turned U.S. crude prices negative.

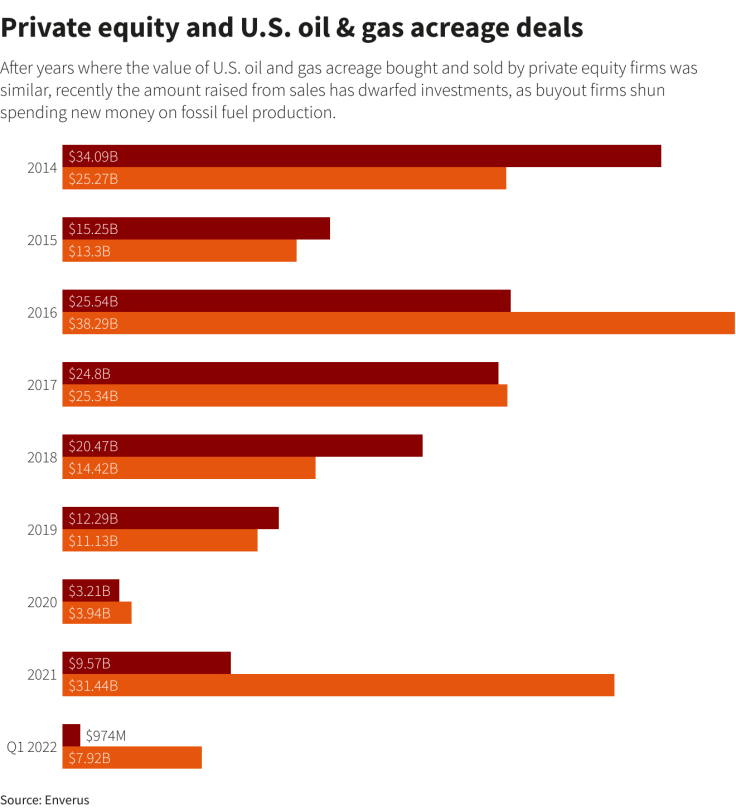

The few remaining are capitalizing on the current energy price rally to cash out on assets rather than buy new ones.

In considering these deals, Elliott is showing an appetite for risk that is rare among its Wall Street peers, the sources said.

Each shale basin has different economics, but were oil prices to remain above $100 per barrel, investment bankers estimate that Elliott could score investment gains of more than 80%.

Should U.S. crude, which briefly touched $130 in March following Russia's invasion of Ukraine, drop back to below $65, Elliott could start losing money, according to the bankers. Oil is currently trading around $110. [O/R]

Reuters spoke to more than a dozen industry sources about Elliott's plans, all on condition of anonymity to discuss confidential conversations.

Elliott declined comment.

Andrew Dittmar, director at energy consultancy Enverus, said he believed the upside was significantly greater than the downside for Elliott.

"At these prices, sticking a dollar in the ground in an oil or gas well is one of the best things you can do in North America as the returns are phenomenal," said Dittmar.

In the Eagle Ford shale basin in south Texas, for example, Enverus data indicates the average potential internal rate of return (IRR) available across 12,000 wells it tracks in the basin was around 140% when oil was at $70 per barrel and natural gas at $3.50 per million British thermal units (mmBtu).

U.S. natural gas futures are now at $8.75 per mmBtu. [NGA/] The typical benchmark return on private equity-like deals in the sector is 20%.

Elliott is looking to provide capital to management teams, who acquire land and develop oil and gas production, the sources said. Last year, Elliott invested in Validus Energy to help it buy Eagle Ford assets from Ovintiv Inc for $880 million.

The two backers, Elliott and Pontem Energy Capital, are now exploring a sale of Validus, with sources forecasting a price tag of more than $1.5 billion, including debt.

CLIMATE CONCERNS

Buyout firms active in the U.S. oil and gas sector sold three times as much in assets last year than they acquired on a dollar-for-dollar basis, according to Enverus. The trend has accelerated this year.

Graphic: Private equity and U.S. oil & gas acreage deals -

Many private equity firms and hedge funds have exited the sector to address concerns from their own investors that they were contributing to climate change. Elliott, which also invests in clean energy and has pushed green policies at firms it backs, does not disclose who its investors are, and it is not clear whether or how it has communicated its foray into the U.S. oil patch with them.

Singer has been a backer of politicians expressing skepticism about how big a problem carbon emissions are. A big financial supporter of the Republican Party in recent years, Singer also chairs the board of trustees at the Manhattan Institute, a think-tank promoting free markets whose energy advocacy skews heavily to long-term fossil fuel usage.

While acquisitions in the sector are new to Elliott's playbook, the West Palm Beach, Florida-based fund has been amassing stakes in oil and gas companies for years, with mixed results. It made money investing in Hess Corp, but its bets involving Roan Resources and Riviera Resources failed after both companies collapsed.

Elliott is expected to make a good return on Birch Resources, formed out of energy assets secured from the 2018 Chapter 11 bankruptcy agreement of Breitburn Energy Partners.

Founded by Singer in 1977 and currently managing around $51.5 billion, Elliott has earned a reputation as one of the most formidable activist investors, going up against corporate giants include AT&T Inc and SoftBank Group Corp.

Through its private equity arm Evergreen Coast Capital, Elliott has pushed more into leveraged buyouts. It has this year agreed a $10.1 billion purchase of TV ratings provider Nielsen Holdings and a $16.5 billion acquisition of software company Citrix Systems.

(The story amends Elliott's HQ in paragraph 20 to West Palm Beach, from New York)

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Business