Valeant Pharmaceuticals Intl Inc (VRX): Amid Fraud Allegations And Sinking Stock Price, Four Big Questions Loom

A cloud of suspicion still hovers over Valeant Pharmaceuticals International Inc., but the company’s top executives have a chance this week to shed light on internal processes that have raised allegations of fraud. The accusations, centered on the Canadian pharmaceutical giant’s distribution and accounting model, sent the firm’s share price tumbling by 35 percent last week. Monday, Valeant is hoping to dispel investors’ doubts with a conference call set to begin before the U.S. equity market opens.

The stakes are high, and not just for Valeant. The company has become a trailblazer in its industry, delighting Wall Street with big acquisitions and steep price hikes on its medicines, frequently undertaken in tandem with layoffs and slashed research budgets at its acquired firms. But rumblings of discontent have been growing for months, as prominent investors such as Australian hedge-fund manager John Hempton have called aspects of Valeant’s business into question.

Central to the company’s strategy is its use of specialty pharmacies, whose importance to the sector has grown of late. One of these pharmacies, Philidor Rx Services, ignited the recent firestorm after Valeant Chairman and CEO J. Michael Pearson revealed that the firm had a previously undisclosed financial relationship with the distributor. It turns out Philidor and related companies are embroiled in a tangle of lawsuits and accusations of fraud.

Here are four unanswered questions that Valeant’s executives will likely face Monday.

1) How did Valeant come to issue an invoice to a company that says it has had no direct dealings with Valeant?

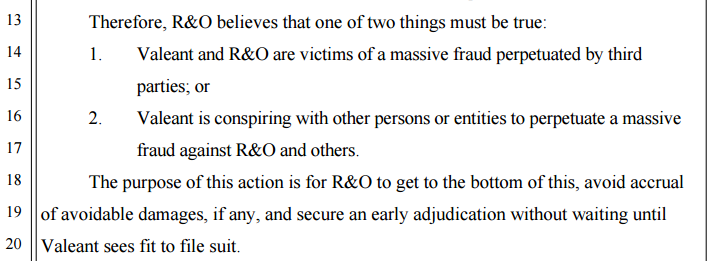

The thread that unraveled Valeant’s tangled pharmaceutical relationships was a lawsuit quietly filed this month by the California-based R&O Pharmacy, which disputed a $70 million invoice it received from Valeant’s chief legal officer. R&O claimed it never conducted any direct business with Valeant and that “massive fraud” was afoot.

In the lawsuit, R&O’s attorney speculated that either the pharmacy and Valeant were mutual victims of a third-party fraudster or Valeant orchestrated the alleged fraud itself.

As it turns out, the third party that R&O had in mind was likely the specialty pharmacy Philidor, which R&O had already accused of using an ownership stake in R&O to access the California drug market, ProPublica reported Friday.

In this scenario, it appears that Valeant shipped drugs to Philidor, which distributed them via mail order to patients in California -- where it was banned from doing business -- by allegedly using R&O’s credentials in the state. But something went awry, leaving an unmet liability of $70 million. The onus will be on Valeant Monday to explain how that happened. For investors, that explanation has so far been lacking.

2) How, exactly, are Philidor, R&O and all the other “captive” pharmacies related?

When the nonprofit Southern Investigative Reporting Foundation broke the news of R&O’s lawsuit against Valeant last Monday, worries grew. Wednesday, short-seller Citron Research issued an explosive note raising the possibility of an “Enron part deux” in the making. Citron alleged that Valeant was shipping inventory to warehouses it controlled, then booking fictitious revenue. Although there was no smoking gun in the allegations, Valeant’s stock ended the day down 19 percent.

Andrew Left, author of the Citron note, revealed that the websites for Philidor and R&O shared identical privacy notices and phone numbers (it was later shown that two separate websites existed for R&O, both with the same physical address). Why did these two apparently independent companies share basic infrastructure?

Earlier in the week, Valeant’s Pearson had disclosed that his company had an option to buy Philidor and had folded the pharmacy’s financials into its own -- satisfying some investors’ concerns that Valeant was booking false revenue in captive firms that it essentially controlled.

But the R&O revelations complicated the picture. Philidor later announced it had an option to acquire R&O, one of many pharmacies in Philidor’s network. The companies seem to operate as so-called variable interest entities, “ownership-light” vehicles that aren’t fully owned by their parent companies but share financials.

The arrangement has baffled some analysts. “On the surface of it, there is no real reason why they need to have these multiple special-purpose pharmacies that are all really part of Philidor,” Dimitry Khmelnitsky, an analyst with Veritas investment Research, told the Financial Post.

Investors will be curious to know how much of the murky structure Valeant knew about or helped engineer, especially given mounting allegations of fraud surrounding Philidor.

3) How does Valeant oversee the specialty pharmacies under its vast umbrella?

Most Wall Street analysts greeted the disclosures this week with relative calm, with some even seeing the cratered share price as presentin a good buying opportunity.

But one analyst, Alex Arfaei of the Bank of Montreal’s BMO Capital Markets, downgraded the company. “We find Valeant’s arrangements with the specialty pharmacy Philidor as not just aggressive, but questionable,” the analyst said in a note. This month, it also was revealed that Valeant had come under a federal probe over its drug pricing, distribution and patient assistance programs.

The list of alleged improprieties associated with Philidor has grown in recent days. The firm was denied a pharmacy license in California late last year over alleged false statements of fact in its application. For instance, California’s Board of Pharmacy said that Philidor claimed on its application to have no owners or shareholders, when in fact it had 16.

In its legal filings concerning Philidor, R&O challenged the company’s alleged use of a related firm, Isolani, to purchase a stake in R&O. Through that ownership stake -- which apparently was not registered with the authorities -- R&O says Philidor shipped drugs to patients using R&O’s billing information without its consent.

The legal case involving R&O and Philidor has yet to be resolved. But the allegations raise questions of how deeply Valeant has been involved in Philidor’s operations. Specialty pharmacies have attracted criticism for their aggressive sales practices and patient-assistance programs, which discount customer co-payments on expensive drugs.

Deutsche Bank analysts echoed wider concerns in a note to clients last week. “We remain cautious on the stock given uncertainties related to the U.S. drug-pricing environment, VRX’s specialty-pharmacy distribution model and related government inquiries.”

Valeant’s leadership has a tall order to fill in alleviating those uncertainties while showing that it has its distribution network under control.

“Investors will focus not only on valuation but will want to take a very detailed approach in understanding the company on a bottom-up basis,” the Deutsche Bank analysts continued. “It will be important to see how the company and management team deal with a period of adversity.”

4) What do these murky relationships say about Valeant’s balance sheet?

Questions about Valeant’s balance sheet are nothing new. Hempton, the Australian money manager who has a short position in Valeant’s shares, has been posting criticisms of the company’s financial statements since mid-2014.

Valeant has said it is scaling back the aggressive acquisition model that has propelled the company to success. As the firm pivots, analysts will be watching the towering stack of debt Valeant holds, a result of its pharmaceutical buying spree.

Valeant’s debt-to-equity ratio is more than eight times those of competitors such as Merck & Co. Inc. and Pfizer Inc. The market for bond insurance priced Valeant debt at levels that made it the riskiest of any health-care company in the world, the Financial Times reported.

“Valeant is changing its business model, including emphasizing research and development, which implies the prior business model was unsustainable,” Morgan Stanley analysts wrote Tuesday.

As Pearson and the rest of Valeant’s executive team attempt to reassure Wall Street about its dealings with Philidor and other specialty pharmacies, it will also be sending a message about its own internals. If bondholders aren’t assuaged, the cost of financing Valeant’s debt could balloon.

© Copyright IBTimes 2025. All rights reserved.

- MOST POPULAR IN Business