CEO Of Coeur Mining Inc, A Silver Mining Company, Talks Markets, Returns and Corporate Culture: Q&A

Top U.S. silver mining company Coeur Mining Inc (NYSE:CDE) spoke with International Business Times about its business, the silver market and industry, and the corporate culture within mining companies.

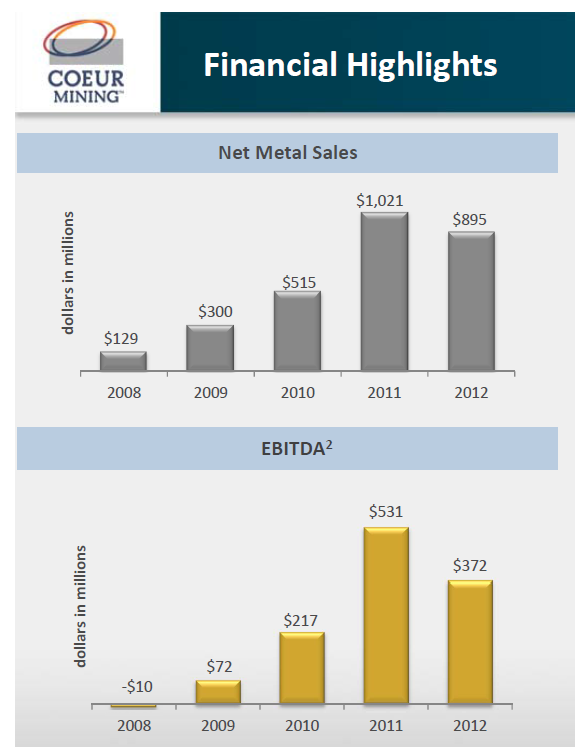

The $1.1 billion company, which calls itself the largest U.S.-based primary silver producer, lost about $69 million over the past three quarters, in a difficult commodities market. It notched annual losses from 2008 to 2011, but recovered in 2011 and 2012.

Edited excerpts from a phone conversation with Coeur CEO Mitchell Krebs follow.

How has the silver price decline in 2013 affected your business? (Silver fell 36 percent in 2013, the second-worst performer among commodities after corn, and worse still than gold’s much publicized 28 percent swoon.)

“It’s the first time in a long time that the industry had to deal with significant and sustained price declines,” said Krebs. Before 2013 price declines, Coeur tried to maximize cash flow by reducing operating costs and freeing up working capital.

“In this kind of cyclical commodities business, no matter where prices are, we always need to focus on reducing costs. It’s the one thing we have a little bit of control over,” he said.

Although cost restructuring was already underway by early 2013, when April and May arrived, with precious metal price freefalls, Coeur stepped up focus.

“There’s nothing like a good price decline to instill some urgency in people,” Krebs said. They cut back capital expenditure budgets for 2014, and ended up spending $100 million in capex in 2013, down from an initially projected $125 million. Exploration expenses were also slimmed down.

“You’ve got to find ways to grow the business that can provide an adequate rate of return even at lower prices,” continued Krebs. “That really shortens the list in terms of opportunities out there in a lower price environment,” he said, referring to new mine projects or acquisitions.

What’s your outlook for silver in 2014?

“I think we’re going to see continued choppiness and a fairly sideways silver price,” said Krebs. “Silver is a very volatile metal and will probably see a range of $18 up to $23 per ounce, throughout the year … Investors are trying to get a sense of global economy, whether there is or isn’t any hint of inflation, or the X-factor of some crisis, a political crisis or otherwise.”

Silver prices are forecast by London’s Capital Economics to hit $21.5 per ounce by the end of 2014, a small gain from the present $19.7/oz. Silver typically trades in tandem with gold, as the more influential yellow metal attracts heavier investment and can drag down silver in its wake.

How much does it cost you to produce silver?

Starting with Coeur’s next quarterly results, the company will release so-called ‘all-in sustaining cost’ metrics, which refer to the total costs required to mine a silver ounce from the ground. Previously, the silver and gold mining industry cited cash costs, which were expenses excluding big capital expenditures, exploration expenses, administrative and corporate overhead, and the like.

Critics who charged that Coeur’s production costs are higher than silver's price tag use “backward-looking” projections, according to Krebs.

“Our all-in sustaining costs is around that $20 an ounce mark,” he said, “and hopefully declining as we keep our focus on those [efficiency] areas,” he said. “Our costs continue to decline.”

Silver miners don’t have a much higher profit margin over gold miners, said Krebs, contrary to some perceptions. Gold miners have suffered this year as production costs per ounce of gold approach the selling price of gold, squeezing company margins.

Your net metal sales and raw earnings fell in 2012 from 2011. Have those picked up for 2013?

“We haven’t disclosed publicly what our 2013 full year numbers are,” Krebs said. The company is due to report its 2013 full year results later in February 2014, and will release mining production figures before that, in coming weeks.

Krebs defended losses by arguing that operating cash flows figures were more relevant in the capital-intensive mining industry, since these metrics strip out non-cash charges and derivative accounting.

“As we look to 2014, on current prices -- about $1250/oz. on gold and $20/oz. on silver -- we are about net cash flow break even for the year,” he said. A substantial cash flow surplus will meet deductions from capital expenditures and royalty payments, he said.

Gold mining stocks fared badly in 2013. Have silver mining stocks done better?

Silver mining companies have suffered from a “lost decade of shareholder value," Krebs said. That’s parallel to problems at gold miners, from mammoth Barrick Gold Corp. (TSE:ABX) to smaller rivals, who faced flack for poor corporate governance and spending without returning cash to shareholders.

“Our whole reason for being here as a company is to recognize the failings of the past, and to change the way we do thing going forward,” he said, citing recent corporate restructurings at Coeur.

Shareholders need to be coaxed off the sidelines and back into precious metal mining equities, he said. The formation of Coeur Capital, a subsidiary dedicated to silver streaming, royalties and acquisitions, is Coeur’s attempt to do that.

“Coeur Capital has much higher margins, is a higher return business, and is a less risky business. Those are all things concerning traditional mining companies that have really scared investors away,” he said.

Coeur’s stock as traded in New York has fallen 51 percent in the past year. Its Canadian stock in Toronto has fared almost as badly. Other silver companies, like Silver Wheaton Corp. (TSE:SLW), have said that recent low valuations have helped smart companies with cheap acquisitions.

“The risk profile of this industry, or at least the perception of it, has really become a major reason why investors are shunning equities in the precious metals sector,” he said. “We just need to be culturally very focused on the return side of the equation. … We [the industry] need to create that value proposition for investors that I think is really lacking right now.”

Last thoughts on Coeur Mining?

“Five years from now, I’d like to see from us … a much more diversified set of revenue streams, from more metals aside from just silver and gold,” Krebs said. The new mining investments, which could include lead, zinc and copper, must balance well with revenues from existing gold and silver properties.

“A portfolio of assets with poly-metallic types can get you much higher margins and give you more of a cushion against lower prices,” he said.

Thanks to the appearance of popular precious metals exchange traded-funds in 2004, investment in precious metals has changed entirely, according to Krebs. Those funds allowed investors easy exposure to metal prices, without the burden of buying physical metals.

“It used to be, you’d attract a premium valuation for being a pure play company, whether a silver company or otherwise. That was sort of the game,” he said. But ETFs now mean mining companies must compete like other companies, on their execution and returns to shareholders.

“We can’t just try to be a leveraged liquid play on a single metal,” he said. “That’s just not a sustainable business model.”

--

Industrial demand for silver should see “a little bit of an uptick”, thanks to a slowly improving global economy, said precious metals retailer Anthem Blanchard to IBTimes. But demand for silver among investors will likely depend on less predictable U.S. interest rates and monetary policy, he added.

Silver miners are expected to produce 800 million silver ounces in 2013, with about 75 percent stemming from silver as a mining by-product, according to November 2013 Thomson Reuters GFMS data. Silver is often produced as a byproduct in gold mines.

Rising mine production in 2013 and a lingering silver surplus from 2012 could prove negative for prices in 2014, according to the GFMS report. Global demand for silver in 2012 stood at about 1 billion ounces, or about 31,000 metric tons, according to the Silver Institute. The silver investment market was worth more than $7 billion globally in 2013.

Barclays PLC (LON:BARC) forecast on Thursday that silver prices could slump to as low as $15/oz in 2014, though it’ll likely average $19/oz.

“Underlying silver market fundamentals are set to remain unaccommodating in 2014 given a projected bloated surplus,” Barclays analysts wrote. Ironically, investors may not realize that at least 5 kilo tonnes of holdings in specialist silver funds are now loss-making, they said. Silver ETPs saw net inflows in 2013, contrasting with steep outflows from gold products.

Analysts polled by Thomson Reuters expect Coeur to report a loss of $16.3 million in its upcoming quarter, down from $36 million in profits a year before. The company recently acquired Vancouver-based Global Royalty Corp. for $23.8 million, in a bid to earn royalties from Global Royalty’s interests in Mexican and Ecuadorian mines, and diversify the business away from pure mining.

Some analysts are modestly upbeat about Coeur’s prospects.

Coeur is close to a meaningful turnaround, and could gain the confidence of investors, but its Nevadan Rochester mine must meet Wall Street expectations, wrote Chris Thompson, an analyst with Raymond James, in recent reports. The company’s production expenses are also high, at about $20/oz., and keeps it highly exposed to silver price fluctuations, he said.

“We believe that CDE [Coeur] is on the cusp of turning the corner in achieving operational consistency, and with that, market confidence … ” he wrote in a September 23 report. “We look for quarter-on-quarter operational improvements to justify our thesis.”

© Copyright IBTimes 2025. All rights reserved.

- MOST POPULAR IN Business