Analysis-U.S. Treasury Yield Curve Divergence Sends Mixed Recession Signals

Two measures of the U.S. Treasury yield curve that are widely watched for recession warnings have veered in opposite directions, raising questions as to what degree central bank bond buying and other technical factors may be distorting the signals on the economy's path.

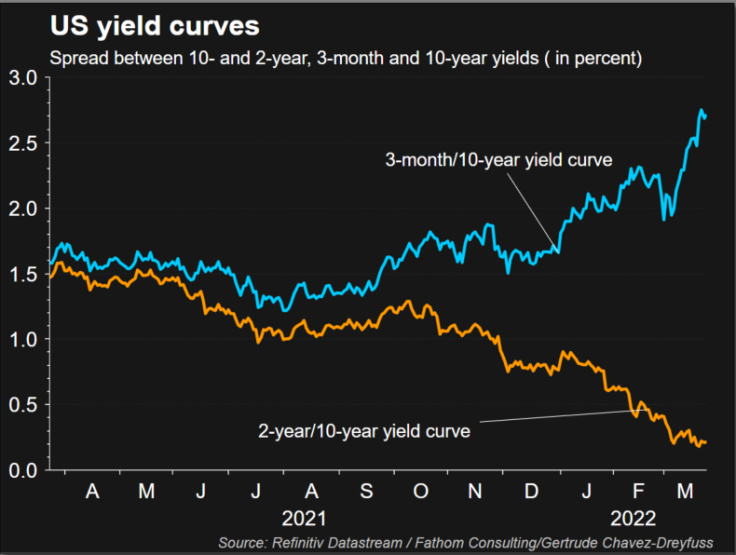

The spread between the yield on 3-month Treasury bills and 10-year notes this month has been widening, which can be an indicator of an economic expansion. On Friday, that curve reached its steepest in more than five years at 196 basis points.

The U.S. 2-year to 10-year curve, on the other hand, has flattened dramatically this year and is close to inverting, where the longer maturity would yield less than the shorter.

Graphic: US yield curves:

Typically, yield curves slope upward as investors demand a higher return on longer-term debt as it carries greater risk because of the higher probability of inflation or default.

A steepening curve typically signals expectations of stronger economic activity, higher inflation, and higher interest rates. A flattening curve suggests investors have lost confidence in the economy's growth outlook.

Inversions are considered a harbinger of eventual recession. But the signal right now is not clear.

"There is a technical issue here," said Ben Emons, managing director of global macro strategy at Medley Global Advisors. "The 3-month T-bill yield is still lower...because it doesn't reflect rate hikes in the future. But it will rise, as the Fed hikes rates."

U.S. two-year yields, on the other hand, are a really good indicator of where Federal Reserve policy is headed over the next two years, Emons added, and it's showing a much steeper path of rate hikes.

The 2s/10s spread was last at 20.10 basis points, having on Monday compressed to 11.4 basis points, its tightest since March 9, 2020, before the onset of the coronavirus pandemic.

The Fed raised short-term interest rates by 0.25 percentage point last week, the first hike since late 2018. U.S. rate futures on Friday priced in a roughly 75% chance of a half-percentage point tightening at its monetary policy meeting in May. For 2022, the futures market expects about 200 basis points of cumulative hikes by the Fed.

"If policy unfolds as the market expects, the 3-month/10-year curve will begin to flatten as more rate hikes become priced into the 3-month tenor," said Dan Belton, fixed income strategist, at BMO Capital.

"The divergence in 3-month and 2-yr Treasury rates suggests that the market is pricing in an increasingly hawkish Fed over the next two years."

The last time the 3-month/10-year curve inverted was in February 2020. A month later, the Fed cut the benchmark overnight lending rate to near zero as the coronavirus pandemic wrought economic havoc around the world.

The 2s-10s inversions, on the other hand, preceded the last eight recessions, including 10 of the last 13, according to BoFA Securities in a research note. The last time this curve inverted was in 2019. The following year, the United States entered a recession, though one caused by the global pandemic.

Graphic: US yield curves/Fed tightening:

U.S. 2s/10s CURVE HAS QUESTIONS TOO

But the 2-year/10-year yield curve also has its technical issues, and not everyone is convinced it's telling the true story.

"Something like 2s/10s, or 5s/30s, will definitely tell you that we're a lot flatter than we've ever been at the start of a hiking cycle," said Gennadiy Goldberg, senior rates strategist at TD Securities.

"Part of that is just the sheer amount of Treasuries that the Fed bought during their COVID QE (quantitative easing) program." Analysts said the Fed's QE the last two years has resulted in an undervalued U.S. 10-year yield and could explain away the disparity in the two yield curves.

Stan Shipley, fixed income strategist, at Evercore ISI in New York cited research which suggests the 10-year yield would be around 3.60% without that stimulus. When the Fed starts shrinking its balance sheet via quantitative tightening, Shipley said the 10-year yield will rise to fair value.

The U.S. 10-year yield was last at 2.475% after hitting a peak of 2.5% on Friday, the highest since May 2019.

"Without QE/balance sheet expansion, the 10-year and 2-year spread would be around 140 basis points, which is hardly threatening and consistent with the 10-year and 3-month spread," Shipley said.

The Evercore analyst thinks the 10-year yield should approach fair value in the first half of 2024, or about 120 basis points higher than the current level.

The U.S. 2-year yield, on the other hand, is fairly priced and Shipley expects the 2s-10s curve to widen.

What does it mean for the U.S. economy?

"Some of the 2-10 shape is down to the fact this is a far more aggressively priced Fed cycle than usual, the notion of how quickly the Fed will move is very front-loaded," said Timothy Graf, head of EMEA macro strategy, at State Street.

"I suspect we will get a growth slowdown but will it lead to recession? It may be next year's story. Households will want to see the fuel prices coming down but generally household balance sheets are in pretty good shape."

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Business