Column-Cold Comfort In Re-steepening U.S. Yield Curve: Mike Dolan

Pretending it did not happen probably does not help much.

Given its track record in preceding the last four recession since 1990, the brief inversion of the U.S. bond yield curve between two and 10 years has unsurprisingly sounded alarms about another pending recession over the next 18 months.

In broad brush terms, these inversions reflect markets' belief that the Federal Reserve will have to move to 'restrictive' policies - with interest rate above long-term neutral estimates embedded in 10 year rates - in order to slow credit and the economy and squeeze out inflation.

And they nod to the fact that most economic cycles don't just end, they are typically killed by the Fed.

Deutsche Bank, for one, now sees the U.S. economy recording two consecutive quarters of contraction in the second half of next year as the Fed races to unwind pandemic supports and tightens policy to rein in the highest inflation rate in 40 years.

But as the spread between the two key short and long-term borrowing rates troughed about -7 basis points on April 1, many have dismissed the signal as something of a fools day joke.

The Fed itself claims it's a false flag and with less predictive power than shorter-term forward yield spreads that headed in the opposite direction.

Others blame massive Fed bond buying for snuffing out the true signal in long rates and that made it 'different this time'. Some investors just said they watch other healthier measures of the curve such as the spread between 3 months and 10 years, which is still positive to the tune of almost 2 percentage points.

And lo and behold, this week the 2-10 year curve reverted back positive and steepened to more than 10 basis points just as the Fed's hawkish rhetoric turned squarely to cutting its $9 trillion balance sheet - allowing bills and bonds to roll off as they mature and flagging possible outright sales ahead.

So a flash in the pan?

Maybe. But the history of the last four inversions of the 2-10 curve means a sudden re-steepening doesn't mean the real economy dodges the bullet - even though speculative traders continue to bet more steepening is ahead.

Before the recession actually hit in the middle of 1990, the 2-10 curve had already turned back positive - moving almost 50 bps higher from the most negative point of the inversion in April 1989.

Similarly, before recession hit in mid-2001, the 2-10 curve had already steepened by almost a full percentage point from the deepest inversion of -46bp in April 2000. And yet again, before the economic contraction around the banking crash of 2008.

People argue the toss about the faintest sliver of inversion that presaged 2020's shock. But most agree that even an all-seeing bond market couldn't have predicted the pandemic and so the jury's out on whether contraction would have ensued anyway.

All that likely happened in all these cases is the Fed saw the downturn coming and took its foot off the brake.

Graphic: YIELD CURVE BALL?-

Graphic: US Fed's 'Term Premium' still negative-

The big question now is whether the much-maligned 2-10 year curve is just re-adjusting to mirror what appears to be rosier signals from still floored short rates just as the long end of the curve is to be freed from Fed intervention.

The Fed this week blared out its intention to start slashing the balance sheet this year alongside planned steep rate rises, with the minutes of last month's meeting flagging a cut of almost $1.2 trillion over the next year or so.

And that seems to have helped steepen the curve a bit as long rate zoomed higher.

But it did nothing to lift the still-negative 'term premium' that's supposedly depressed by Fed distortions at the long end. All this week's movement coming 'real' or inflation-adjusted Treasury yields more reflective of Fed policy rate projections themselves.

What's more, the $1.2 trillion cut flagged over the next year is likely mostly in short-term bills and bonds. It will only bring the total balance sheet back to where it was in April of last year and would be still shy of what some Fed officials flagged earlier in the year as 'pure excess liquidity' of some $1.5 trillion.

Daily Fed money market drainage, via reverse repurchase tenders, were still as high as $1.7 trillion this week and suggest estimates of the excess have gotten bigger if anything.

But if it takes 12 months just to clip $1.2 trillion off the balance sheet, we're already at the cusp of when Deutsche Bank sees recession hitting.

All that questions just how much the Fed can realistically tighten before bowling over markets and the economy.

Societe Generale upped the ante on that this week by showing how its quantitative analysis of the combined impact of both Fed policy rate rises and ebbing bond purchases - modelled as a so-called 'shadow Fed funds rate' - meant the peak in Fed rates could be less than half the 3.5% markets currently expect.

Work by SG analyst Solomon Tadesse, flagged by strategist Albert Edwards, reckoned the near doubling of the Fed's balance sheet since 2019 mean their modeled shadow Fed rate was effectively -5% at its trough -- and still -2.5% even after the first Fed hike last month.

"But with the pace of QT likely accelerated, the actual FFR will struggle to get to 1% before the Fed needs to halt the tightening cycle. That is shocking," Edwards wrote.

Other columns:

COLUMN-Funds get steamrollered on steeper U.S. yield curve bets. Again: McGeever

COLUMN-Felling the 'magic money tree' as central banks call time :Mike Dolan

Graphic: Fed share of the Treasury market-

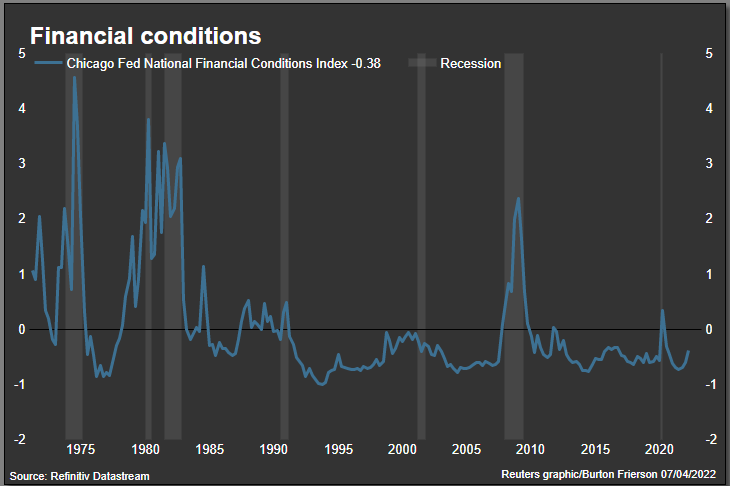

Graphic: US financial conditions-

The author is editor-at-large for finance and markets at Reuters News. Any views expressed here are his own

(by Mike Dolan, Twitter: @reutersMikeD; Editing by David Clarke)

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets