Column-Ukraine Crisis Re-focuses World Investment Themes: McGeever

"A major geopolitical realignment is taking place," which, like 9/11, "shapes major governments' foreign and military policies unpredictably for years to come."

So wrote Citi's market strategy team at the weekend in response to the unprecedented financial sanctions imposed on Moscow by many nations - and some remarkable policy U-turns in European capitals - after Russia invaded Ukraine.

If a global geopolitical shift of that magnitude is underway, it surely follows that a similarly seismic, multi-year shift in the global investment landscape is also upon us.

The immediate playbook for investors will be to 'de-risk,' and pile into the safest or most liquid assets. This means moving out of stocks, credit, and emerging market assets, and into U.S. Treasuries, top-rated government bonds and the dollar.

But then what? Out of crisis always emerges opportunity.

"We are likely to see military, infrastructure and cyber security spending in the West not only increased but also speeded up," Stefan Kreuzkamp, chief investment officer at DWS, wrote on Tuesday.

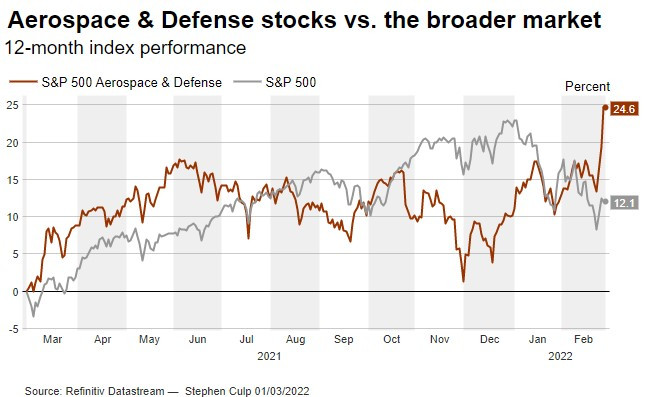

Defense and aerospace stocks have soared since German Chancellor Olaf Scholz's bombshell on Sunday that Germany will commit about 100 billion euros ($118 billion) to a fund for its military and ramp up defense spending to more than 2% of gross domestic product, finally meeting a NATO target set out 16 years ago.

If all NATO countries agree to the 2% of GDP target, billions more will flood into defense and related sectors.

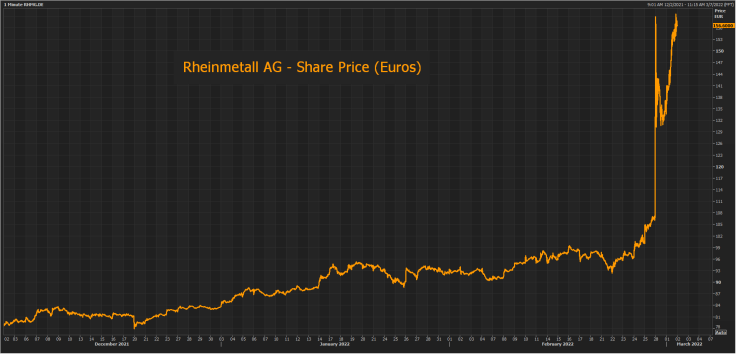

Graphic - Germany's Rheinmetall AG -Share Price:

Graphic - U.S. Defense & Aerospace Stocks:

Germany's Rheinmetall AG jumped a record 25% on Monday and gained a further 18% on Tuesday to hit a new high of 159 euros a share. Military sensor maker Hensoldt rocketed 42% on Monday and added a further 20% on Tuesday to 25 euros a share.

"That is an area you would expect to see continued growth, especially if this extra spending from Germany and Europe comes through," said Crit Thomas, investment strategist at Touchstone Investments, which oversees $34 billion in assets.

If so, it would be a reversal of the 'peace dividend' that followed the collapse of the Soviet Union and end of the Cold War three decades ago. The idea then was less defense spending would help reduce government borrowing, potentially paving the way for tax cuts.

That may flip in the coming years.

FOCUS ON VALUATIONS

JPMorgan economists said Berlin's defense pivot is one of a "number of profound political and policy implications" resulting from the Russia-Ukraine war that will reverberate for years to come.

Others may prove equally important. Take energy.

As worries intensify over supply and the impact of sanctions, near-term prices are spiking higher. Brent crude oil has leapt back above $100 a barrel, and some analysts say European natural gas prices for the 2022-23 winter could be even higher than this winter.

Europe, which depends on Russia for about 40% of its natural gas, will reduce that dependency and seek alternative sources. Italy's foreign minister said on Monday that Rome will buy more from Algeria.

These changes will take a long time to come into effect, but once they do, the upshot may be that greater supply from other countries simply raises aggregate global supply. If so, price pressures may eventually be to the downside, not the upside.

Not only is Europe seeking to wean itself off Russian energy, it is leading the world's climate-driven shift away from fossil fuels.

Germany's government is preparing to speed up passage of the Renewable Energy Sources Act through its parliament so that it can come into force by July, according to a document seen by Reuters.

European offshore wind companies Vestas Wind Systems, Nordex and Orsted on Monday jumped more than 15%, 13%, and 10%, respectively. Investor interest in clean and renewable energy is only liable to increase.

On a broader index level, equity strategists at Citi note that investors' response to most geopolitical events of recent decades has been simply to 'buy the dip'.

But Phil Toews, who oversees $2.2 billion at Toews Asset Management, reckons this approach can no longer be taken for granted because inflation is so high now that borrowing costs are bound to rise. Perhaps significantly.

He argues that the medium-term to long-term outlook boils down to valuation as much as sector. He notes that the S&P 500 index's 12-month trailing valuation is still above 20 times earnings, consistent with a bear market.

When it is back down to the historical average around 15 times earnings, then it's game on.

"Once valuations are washed out, regardless of the geopolitics, you can approach the markets with a new perspective. There will be potentially very good opportunities out there eventually," Toews predicts.

Graphic - S&P 500 Trailing PE:

(The opinions expressed here are those of the author, a columnist for Reuters.)

(By Jamie McGeever; Editing by Paul Simao)

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets