Delta Air Lines, Inc. Earnings: A Big Step Forward

Delta Air Lines (NYSE:DAL) stock has been stagnant for years as the company has struggled to meet its earnings targets. During 2015 and 2016, Delta gradually surrendered virtually all of its savings from falling fuel prices through unit revenue declines. In 2017 and 2018, fuel prices have rebounded quickly, more than offsetting the benefit from a return to unit revenue growth.

This article originally appeared in the Motley Fool.

During 2018, Delta's management has repeatedly projected that the carrier would be able to stabilize its profitability by year-end. A recent fuel price spike appeared to put this target in jeopardy.

However, on Thursday, Delta Air Lines reported slightly better than expected earnings for the third quarter. Moreover, its Q4 guidance showed that it is on track to stabilize its pre-tax margin this quarter, before hopefully expanding its margins in 2019.

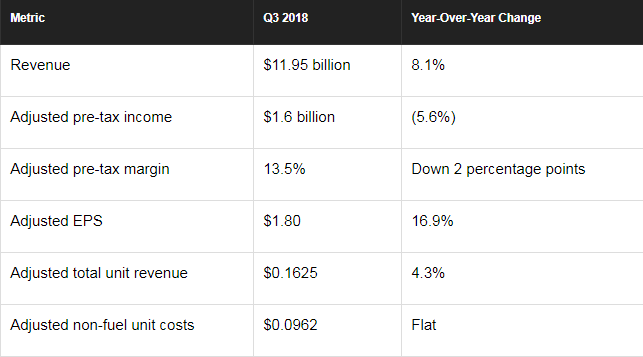

Delta earnings by the numbers

Last quarter, Delta posted solid growth in revenue per available seat mile (RASM), despite facing a roughly 0.5 percentage point headwind from Hurricane Florence. Meanwhile, the company was able to keep its non-fuel unit costs flat on a year-over-year basis.

Rising fuel prices still drove some margin erosion during the third quarter. Nevertheless, Delta managed to boost adjusted EPS by 17% year over year, as its tax rate plunged due to federal tax reform. Here are the details of Delta's Q3 performance.

Delta's adjusted earnings per share of $1.80 was at the high end of the updated guidance range published earlier this month. This beat the average analyst estimate of $1.74.

Strong demand in the domestic and transatlantic markets

Delta's strong third-quarter revenue performance was driven by the domestic and transatlantic regions. Delta increased its domestic capacity 5.6% year over year in the third quarter, but it still managed to grow RASM by 3.3%, pushing total revenue in the region up 9.2%.

Meanwhile, the transatlantic market continued to benefit from stellar demand. RASM surged 7.8% on a 2.7% capacity increase, leading to a 10.7% uptick in revenue.

By contrast, unit revenue declined in Latin America, due to the strong dollar and economic weakness in certain markets there. And while RASM did rise 4.8% in the transpacific market, Delta had to reduce capacity in that region by 1.7% to achieve this result. Fortunately, Delta gets more than 85% of its passenger revenue from the domestic and transatlantic regions, so weaker conditions in other markets don't hurt its revenue growth too much.

The outlook is promising

Looking to the fourth quarter, Delta expects to notch another solid 3% to 5% RASM gain. Additionally, adjusted non-fuel unit costs should decline as much as 1%.

As a result, while fuel costs are on track to rise to about $2.50 per gallon -- compared to $2.22 per gallon last quarter -- management is projecting that Delta will report a pre-tax margin between 9% and 11%. That would be right in line with its Q4 2017 pre-tax margin of 10%.

Delta's fleet renewal strategy is contributing to this improving margin trajectory by allowing the carrier to hold its non-fuel unit costs flat and reduce its fuel consumption. With new aircraft set to arrive at a rapid rate over the next two years, fuel efficiency will continue to improve, while maintenance costs should decline.

The exact timing of Delta's return to margin expansion will depend on where oil prices go from here. Nevertheless, the carrier's solid Q3 performance and Q4 outlook should give investors comfort that Delta Air Lines is on the right track.

Adam Levine-Weinberg owns shares of Delta Air Lines. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

- MOST POPULAR IN Business