Euro Slips Below $1.06 For First Time Since 2017

The euro fell below $1.06 for the first time in five years against a broadly strong U.S. dollar on Wednesday amid rising concerns around energy safety and growth slowdown in China and Europe.

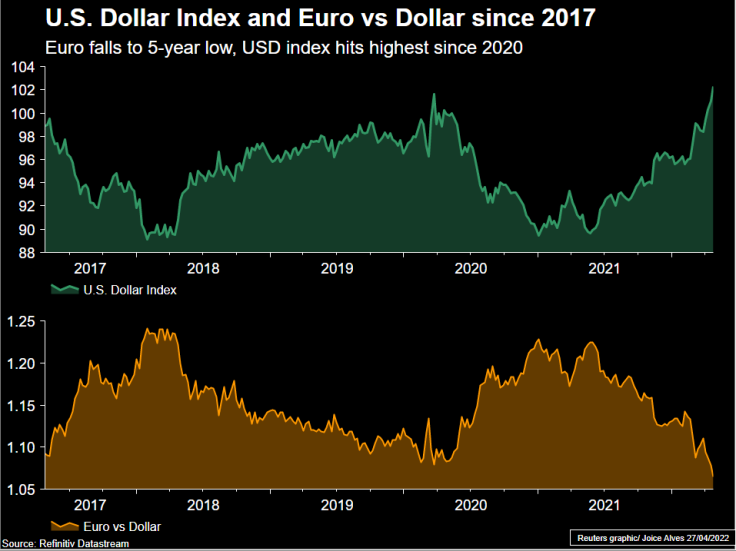

The euro slipped to a five-year low of $1.05860 after Russia's Gazprom said it would cut gas supply to Poland and Bulgaria, as the crisis over Russia's invasion of Ukraine deepened. It was 0.3% lower at $1.0607 at 1100 GMT.

The single currency has fallen more than 4% so far in April and is heading for its worst monthly loss in more than seven years as uncertainty around the war in Ukraine and China's COVID lockdown measures led traders to ditch the euro in favour of the safe-haven dollar.

"Exaggerating the downside risk for euro/dollar have been the COVID lockdown fears for China," said Jane Foley, Head of FX Strategy at Rabobank London.

Additionally, "fears over energy security in Europe have been hugely amplified by reports regarding the severing of Russian gas supplies to Poland," she added.

Economic growth concerns are rising. Data showed consumer confidence in France, the euro zone's second largest economy, fell more than expected in April.

In the meantime, the U.S. dollar index, which measures the greenback performance against a basket of six major currencies, rose 0.3% to 102.7, after touching its highest since the early days of the pandemic.

Graphic: Euro and Dollar -

Also supporting the dollar index, traders wager that rates are going up faster in the United States than any other major economy.

"The U.S. dollar benefits from the prospect of an ongoing flight to safety liquidity bid," Jeremy Stretch, head of G10 FX strategy at CIBC, said.

"The U.S. looks set to be less impacted than others, notably Europe and Japan, from the energy price spike. As a consequence of the latter, the Fed (Federal Reserve) remains the most hawkish central bank and the dollar remains well supported, even if it remains rather overbought," he added.

Elsewhere, the Chinese yuan took a breather after falling to a 13-month low on Monday, steadying at 6.5500 per dollar. [CNY/] Data also showed Chinese industrial profit growth accelerated in March.

Sterling, which has dropped more than 2% on the dollar this week as soft retail sales data prompted a re-think of Britain's rates outlook, hit a fresh 21-month low of $1.2536.

Commodity currencies have also sold lately in favour of the safety of the U.S. dollar, driving the New Zealand dollar to its lowest level since January at $0.6551.

The Norwegian crown slipped against the dollar to its lowest level of 9.2200 since November 2020. It was last flat at 9.2360 crowns.

The Australian dollar briefly touched its lowest level since February but caught some wind after Australian consumer prices surged at their fastest annual pace in two decades, spurring speculation that interest rates could be lifted from record lows as soon as next week. The Aussie was up 0.3% at $0.7147. [AUD/]

The stronger dollar also dented an attempted bounce for the yen, which had enjoyed some support from safety flows and positioning for the risk of a policy shift. The yen last traded 0.7% lower at 127.90 per dollar.

The Bank of Japan meets on Thursday and it is set to maintain ultra-low interest rates, as rising raw material costs force it to focus on underpinning a fragile economic recovery.

The South Korean won sank into a two-year trough after North Korea pledged to boost its nuclear arsenal.

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets