Pity Poor ECB - Bluff, Error Or Remix?

The European Central Bank's decision to keep on tightening despite fear of war and stagflation has been criticised as either bluff or error - but may just reflect a deliberate shift in Europe's economic policy mix.

The ECB On Thursday was the first of the 'Big Four' central banks to meet since Russia's invasion of Ukraine and the related energy price explosion, with markets on tenterhooks as to whether inflation or growth implications would take precedence.

Many investors were instantly surprised it opted so clearly for the former, accelerating a wind down of its main bond buying programme through the third quarter of this year and goosing market bets on interest rate rises by the end of the year.

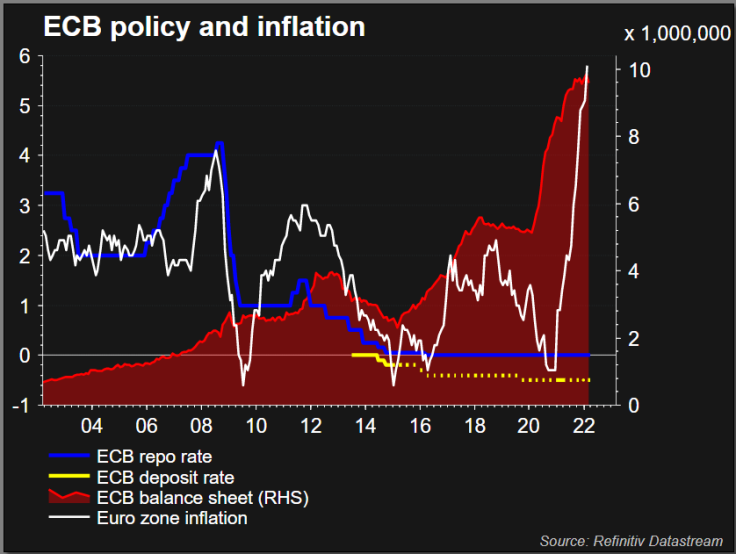

ECB policy and inflation

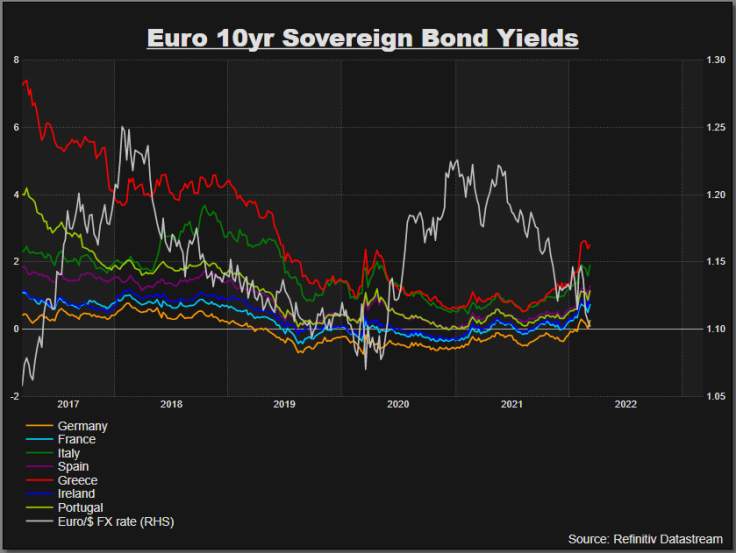

Euro sovereign bond yields and euro FX

Money markets now discount almost 45bps of ECB rate rises by yearend - bringing its deeply negative deposit rate back close to zero for the first time in eight years - compared with about 30bp of hikes just prior to the meeting. And the prospect of less bond buying along with an end to negative interest rates was enough to jar euro government bonds and send long-term borrowing costs across the zone surging.

The ECB's cover for its hawkish tilt was revised forecasts showing inflation back above its 2% target next year - a higher landing point from this year's record 5.1%.

And yet it set the scene with loud caveats about Ukraine and sky-high energy prices that also saw it cut this year's growth forecast by half a point to 3.7% and providing an "alternative" worst-case scenario. ECB chief Christine Lagarde talked of "huge" uncertainty and stressed "maximum optionality" and "maximum agility and flexibility."

And this is where investors guessed a bluff of sorts.

Fidelity International's Anna Stupnytska insisted the energy shock around Ukraine could push the euro zone into recession in the second half of the year and market pricing was way off.

"We do not expect the ECB to hike rates this year, despite change in market pricing," she said. "The risk is skewed towards more QE, not less, especially if gas supplies from Russia to Europe are disrupted going forward."

Goldman Sachs Asset Management's Gurpreet Gill also doubted a 2022 rate hike, saying the prospects were "limited."

Others chimed in that there was a high chance this week's plan would be reversed.

"At a minimum, war-related uncertainty will ensure the ECB proceeds cautiously and gradually," Federated Hermes's Silvia Dall'Angelo said. "In the worst-case scenario, it is possible the ECB will have to resort to a new emergency package of measures and delay lift off."

NEEDLE AND COMPASS

The prospect of a climbdown reminded many of former ECB chief Jean Claude Trichet's two quickly reversed attempts to raise interest rates in the middle the 2008 banking crash and again as the euro sovereign debt crisis raged in 2011. His repeated excuse back then was that the ECB had a singular inflation focus and mandate.

"To be unkind, there was a whiff of Trichet's 'there is only one needle in our compass' in the actions today, a line that has become associated with central bank obstinance and ultimately policy error," Janus Henderson Investors' Andrew Mulliner said.

"Understanding precisely what the ECB were trying to achieve today, if not tighter monetary conditions, is a challenge."

GAM Investments' Charles Hepworth was just as critical. "It all feels like a d?j? vu sense of continual policy mistakes by the ECB," he said

And yet many more sympathise with the plight of central bankers caught between a rock and a hard place right now, facing an unenviable mix of war and stagflation ahead.

"Make no mistake, if the conflict is prolonged and elevated energy prices weigh heavily on household consumptions and confidence, the ECB will find it immensely tough to raise rates this year," Principal Global Investors' Seema Shah said. "Who would want to be a central banker in this situation?"

But for all the investor doubts, Reuters sources say that only a handful of the ECB's governing council were against ending the asset purchase scheme by the end of Q3.

What some suspect is that faced with the twin shock of energy-spurred inflation and demand destruction, European Union governments on an "economic war" footing and their main central bank will end up splitting the policy challenge more evenly than they over the past 12 years.

With inflation absent for so many years and Germany insisting on a tight rein on euro budgets through sovereign debt crises a decade ago, cyclical demand and credit management was left almost entirely to the ECB.

But as inflation returns, exaggerated by the oil and gas squeeze around Russia's invasion of Ukraine, the ECB may now see its main job as normalising monetary policy while governments more readily foot the bill to ease the pain on household incomes.

And this week's EU summit in Versailles provides the counter punch to this week's ECB move.

"It looks like the fiscal levers available at both the EU and national levels will have to do the heavy lifting in response to negative and possibly worsening consequences of the war in Ukraine," Dall'Angelo at Federated Hermes said.

The problem is that by emphasising a hard end to new asset purchases rather than the rise in policy rates ahead, the ECB has spooked the very bond markets needed to finance that fiscal offset. Who'd be a central banker indeed.

The author is editor-at-large for finance and markets at Reuters News. Any views expressed here are his own

(by Mike Dolan, Twitter: @reutersMikeD; Editing by Andrew Heavens)

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets