Why Cisco’s Cybersecurity Business Is About To Take Off

Cisco's (NASDAQ:CSCO) cybersecurity business is getting better with each passing quarter. The networking specialist's cybersecurity revenue now exceeds many pure-play specialists thanks to the scale of its business, and it won't be long before it establishes a viselike grip over the market.

This article originally appeared in The Motley Fool.

Stepping on the gas

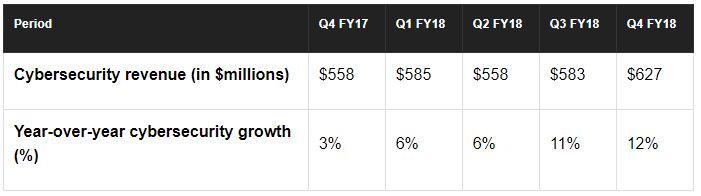

In the recently reported fourth quarter, Cisco's cybersecurity revenue shot up 12 percent annually to $627 million, making cybersecurity Cisco's fastest-growing segment. By comparison, pure-play cybersecurity company Check Point Software Technologies posted a revenue increase of just 2 percent last quarter.

What's even more impressive is that the networking giant's cybersecurity revenue growth has accelerated over time.

It is not difficult to understand how Cisco has managed to bump up the growth of its cybersecurity business. The company's legacy as a provider of networking equipment such as routers and switches gives it an immense advantage over pure-play rivals, since it can simply bundle its cybersecurity solutions at the hardware level.

This is what Cisco has been doing for the past few years through its "Security Everywhere" strategy. The company has been pushing its cybersecurity solutions into mission-critical areas such as networking hardware, the cloud, and endpoints, promising customers that it can better close gaps within the network to prevent, detect, or remedy attacks.

Cisco's cybersecurity revenue growth shows that the strategy is working. What's more, the company is doing the right thing by lapping up smaller companies to bolster its expertise in specific cybersecurity niches and to enhance the appeal of its offerings. For instance, Cisco recently acquired Duo Security for $2.35 billion, the latest in a line of cybersecurity-specific acquisitions made by the networking giant.

Duo adds a new dimension to Cisco's cybersecurity business thanks to its expertise in two-factor authentication. According to Verizon, 63 percent of data breaches are a result of using weak, default, and even stolen passwords. This is where multifactor authentication services come into play, as the user will have to authenticate access on at least two fronts.

Grand View Research estimates that demand for multifactor authentication will increase at an annual pace of 15 percent for the next seven years. So Cisco has entered yet another fast-growing pocket of the cybersecurity industry that should help boost its cybersecurity segment's growth and help drive greater profitability in the long run.

The bigger picture

Cybersecurity is Cisco's fastest-growing segment, but it only provides around 5 percent of its total revenue. This means that the cybersecurity business isn't moving the needle in a big way for Cisco just yet, but at the same time, investors cannot ignore that cybersecurity is driving a transformation at Cisco.

As it stands, recurring revenue now makes up 32 percent of the company's top line, up 1 percentage point from the prior-year period. Additionally, subscription revenue now makes up 56 percent of the company's software segment compared to 51 percent in the prior-year period. The improvement in these metrics led to a 23 percent annual jump in Cisco's deferred revenue from software and subscription sales last quarter to $6.1 billion.

This is a step in the right direction for Cisco, as recurring revenue sources generally yield higher profitability, since it costs less to service an existing customer than going out to acquire a new one. Additionally, Cisco can cross-sell any new cybersecurity features to its existing customers and boost margins, since it will be able to lower the cost of sales.

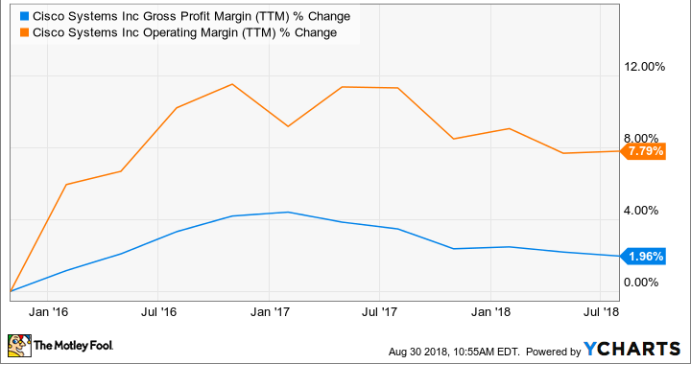

Now, there isn't any hard evidence to prove how much of a catalyst cybersecurity growth is to Cisco's margins, but there's a way to establish the positive correlation between the two. Back in 2016, cybersecurity was just 3.8 percent of Cisco's total revenue. As the contribution of this business to Cisco's top line has improved, so has the company's margin profile.

Cybersecurity could be a big driver of Cisco's growth in the long run, as the company is positioning itself to grab a bigger piece of this space by using acquisitions and its influence in networking hardware. At the same time, cybersecurity will allow the company to grow its business profitably because it has the potential to generate stronger margins. This is one of the reasons why analysts expect Cisco's earnings growth to clock a higher annual growth rate of nearly 9 percent over the next five years as compared to the 5.5 percent annual increase it has clocked in the last five.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool owns shares of and recommends Check Point Software Technologies. The Motley Fool recommends Verizon Communications. The Motley Fool has a disclosure policy.

- MOST POPULAR IN Business