RIP MySpace, Long Live Facebook - MySpace sold for $35 mln to Specific Media

Embattled social networking site MySpace has been sold by its owner News Corp. to digital media company Specific Media for a rumored $35 million, a deal that clinches the position of Facebook as the lord, king and master of social networking world.

As part of the deal, about half of MySpace's 400-odd employees will lose their jobs while News Corp. will take a minority equity share (reportedly something between 5-10 percent) in Specific Media.

The deal will also see MySpace CEO quit his post after a 2-month transitory period. My time here at MySpace represents the most engaging and challenging time of my professional career, Jones wrote. I have found our team to be comprised of the best people I have come across in our industry.

Specific Media is very happy about the deal as it got MySpace for a steal. MySpace is a recognized leader that has pioneered the social media space. The company has transformed the ways in which audiences discover, consume and engage with content online.

There are many synergies between our companies as we are both focused on enhancing digital media experiences by fueling connections with relevance and interest, he said. We look forward to combining our platforms to drive the next generation of digital innovation, CEO Tim Vanderhook said in a statement.

The deal will give Specific Media instant access to the data of 30 million-odd MySpace users for targeted advertisements besides giving the company a media platform of its own from where it can sell its ads.

Though the price tag represents a fraction of what News Corp. bought MySpace for, market analysts said News Corp. is better off by putting the loss making site on the block.

News Corp. bought MySpace for $580 million in 2005 as part of its ongoing efforts to drive up digital media traffic.

And, despite undergoing a massive redesign last year, which included remodeling MySpace as an entertainment and music hub, MySpace failed to keep up with No.1 social networking site Facebook.

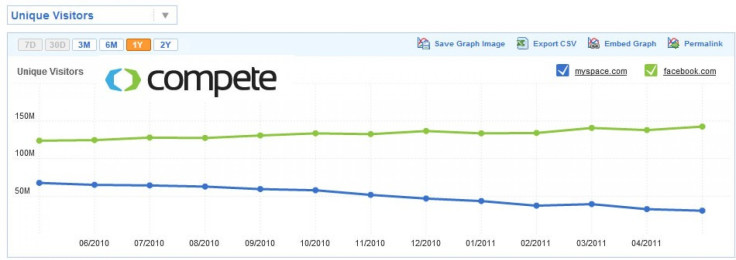

According to data from Compete.com, MySpace pulled in 30.79 million unique visitors last month, down 6.34 percent compared with the previous month and down 54.47 percent on a year-on-year basis.

On the other hand, Facebook pulled in 142.66 million unique visitors last month, up 3.44 percent compared to previous month and 15.26 percent on a year-to-year basis. Currently, Facebook pulls in nearly 5 times more traffic than MySpace.

However, the sale of MySpace is not new and in fact as early as February this year, it was rumored that MySpace would be put up on the block. At that time, News Corp. CEO Chase Carey had said that it was the right moment to sell off MySpace to a new buyer in order for the site to reach its full potential.

And, when News Corp. failed to find a potential suitor, it also reduced MySpace's total workforce by 47 percent or around 500 employees to make MySpace look more attractive to suitors.

And, though a loss of around $550 million is a huge amount, things weren't this bad five years back.

In 2006, after News Corp. bought MySpace, the 100 millionth MySpace account was created and it appeared that MySpace would continue to rule the social network world. It was already crushing smaller rivals like Friendster and Facebook was still taking its baby steps.

However, things began to go wrong quickly from 2007 - Facebook overtook MySpace in terms of traffic and Twitter tweeted. Data privacy concerns surfaced and top talents like former Facebook executive Owen Van Natta, who News Corp. had roped in to head MySpace, left. Revenue tumbled and web traffic screeched to a grinding halt.

Today, Facebook boasts of 750 million users while MySpace is struggling to retain a number that is less than one-tenth of Facebook's.

Hence, the demise of MySpace was inevitable.

But, oh, how much News Corp. must probably be wishing now that it bought a stake in Facebook instead. Why? In 2007, Microsoft bought 1.6 percent stake in Facebook for $240 million and recently Facebook's value has been estimated at $70 billion.

© Copyright IBTimes 2025. All rights reserved.

- MOST POPULAR IN Technology