Wells Fargo & Co (WFC) Q4 Earnings Preview: Picking Low-Hanging Fruits

Wells Fargo & Co. (NYSE:WFC), a bellwether for the mortgage and housing sectors, is expected to beat earnings estimates when it reports fourth-quarter results, largely by relying on cutting expenses and releasing reserves set aside for bad loans as higher rates continue to reduce mortgage refinancing activity.

“Wells Fargo will hit its numbers because Wells Fargo knows how to manipulate its balance sheet in fashions that will generate the profit," said influential bank analyst Dick Bove of Rafferty Capital. He is also the author of a new book, “Guardians of Prosperity: Why America Needs Big Banks.”

"All they have to do is change the method in which they hedge their mortgages and they’ll hit their numbers,” he added.

The San Francisco-based lender, which reports earnings on Tuesday before markets open, is likely to book its 16th consecutive quarter of profit growth. Analysts polled by Thomson Reuters are projecting fourth-quarter net income of $5.29 billion, or 99 cents a share, compared with $4.66 billion, or 91 cents a share, in the year-ago period. Excluding one-time items, EPS is likely to come in at 98 cents a share, versus 92 cents a share a year earlier.

Keith Horowitz at Citigroup expects Wells Fargo to beat the consensus estimate by 2 cents, driven primarily by lower expenses as compensation expenses continue to come down on actions taken in the third-quarter.

“While we expect a beat, we expect to see relatively lower earnings quality as the bottom line is driven by one-time gains similar to the third quarter,” Horowitz added.

Reserve releases, an accounting maneuver that enables banks to add any money set aside (for bad loans when credit quality improves) to profits, come at a time when banks are being slammed by revenue slowdowns.

In a Jan. 6 note, UBS equity research analyst Derek De Vries forecast that Wells Fargo will pad its bottom line with $755 million from reserve releases in the fourth quarter. By comparison, the lender released $900 million in the third quarter and $250 million in the fourth quarter of 2012.

Revenue is a good indicator of a bank’s actual performance. Banks can pull all kinds of accounting tricks to make their earnings look better in any given quarter, but that is harder to do so with revenue. Revenue is projected to decline by 6 percent to $20.66 billion in the last three months of 2013, from $21.95 billion a year ago.

For the full year, Wells Fargo will probably record net income of $20.83 billion, or $3.86 per share, on revenue of $84.18 billion. In 2012, the bank earned $17.80 billion, or $3.36 a share, on revenue of $86.09 billion.

The bank took a hit to its efficiency ratio, a measure of expenses divided by revenue, in the third quarter. Wells Fargo’s efficiency ratio was 59.1 percent, higher than the 55 percent to 59 percent target executives have talked about in the past.

Executives attributed the decline in efficiency to lower mortgage banking revenue and said once that expense cuts are fully realized, the company should become more efficient.

“We expect our efficiency ratio to improve in the fourth quarter,” Wells Fargo’s Chief Financial Officer Timothy Sloan said at an industry conference on Nov. 13.

Mortgage Slump

“In the fourth quarter we expect mortgage originations to decline from the third-quarter levels, both reflecting lower refinance volume and normal fourth-quarter seasonality in the purchase market,” Sloan said in November. “But our expectation is that margins are going to stabilize.”

The end of a three-decade period of falling mortgage rates has caused many borrowers to pull back from refinancing their homes. As a result, banks began slimming down their own operations, which they had bulked up in recent years to take advantage of all-time low interest rates.

Wells Fargo said that it spent about $63 million in severance pay to the 6,200 employees it let go since the refinancing slump began in the summer. But those expense cuts still have not come through in third-quarter earnings as the bank continues to spend on severance pay. Executives said at the Nov. 13 industry conference that the job cuts will lead to lower expenses in the fourth quarter. The full benefit of those cuts will be seen by the first quarter of 2014, they added.

"Personnel expenses should decline in the fourth quarter due to the reduction of 6,200 full-time equivalents we've announced in our mortgage business and will be fully reflected in our expenses in the first quarter of 2014,” Sloan said.

The nation’s fourth-largest bank by assets has seen its mortgage-banking income tumble since a rise this summer in long-term interest rates tempered homeowners' desire to refinance. The bank saw its mortgage-banking income fall 43 percent to $1.61 billion in the third quarter. Mortgage originations, which include loans for home purchases and refinancing, fell 42 percent to $80 billion.

The Mortgage Bankers Association this week plans to cut its 2014 forecast for loan originations, which includes loans for home purchases and refinancing. The current forecast of $1.2 trillion would represent the lowest level in 14 years.

From 2000 to 2003 alone, mortgage rates fell from a peak of 8 percent to a low of 5 percent, and refinance volumes soared to $2.5 trillion in 2003, from $230 billion in 2000.

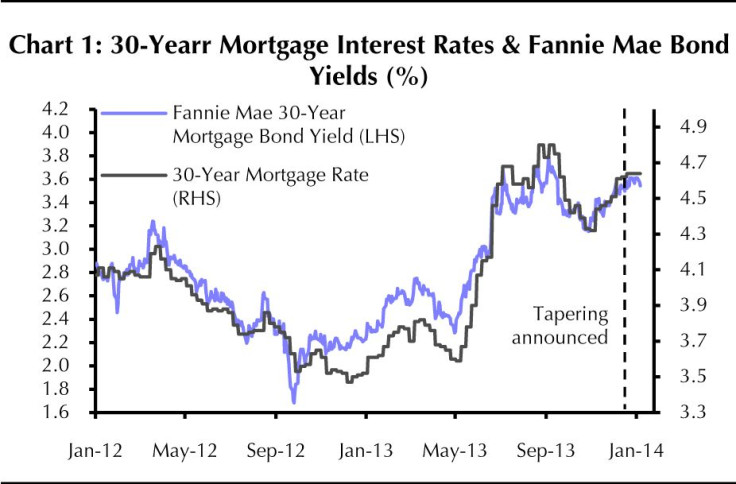

The rate on a 30-year fixed-rate mortgage averaged 4.6 percent in December, up from 3.35 percent in early May.

Most of this increase occurred in the weeks before the Federal Reserve’s announcement on Dec. 18 that it will begin tapering its asset purchases this year, reflecting a degree of market uncertainty about the Fed’s approach, according to Capital Economics' Paul Diggle.

The slight increase in mortgage interest rates in the closing months of last year has been reflected in lower mortgage applications, Diggle noted. Applications for remortgaging fell by 23 percent month-on-month in December to a new post-crash low. And applications for home purchases fell by 5.7 percent month-on-month, reaching their lowest level since early- 2012.

While long-term interest rates rose, the Fed is still keeping short-term interest rates low, and this will continue to pressure lenders’ net interest margin, which is a key measure of lending profitability.

Citigroup’s Horowitz expects Wells Fargo’s fourth-quarter net interest margin to drop to 3.34 percent. In the first three quarters of 2013, the bank’s NIM fell from 3.48 percent, to 3.46 percent and then to 3.38 percent.

Fannie Mae

Wells Fargo on Dec. 30 reached a $591 million deal with Fannie Mae to settle claims that it sold defective mortgages to the government-controlled home-loan financier.

Adjusted for credits related to previous repurchases, Wells Fargo will pay $541 million. It said it had set aside sufficient funds for the settlement. The bank said the deal resolves all of the potential buyback demands it had pertaining to loans sold to Fannie Mae that were originated before 2009.

In September, Wells Fargo agreed to pay a net $780 million to the smaller Freddie Mac to resolve similar repurchase claims.

Stock Performance

As the U.S. economy improves, bank stocks are once again back in favor. Financial shares rose 33 percent last year in their strongest annual showing since 1997, outpacing the 30 percent increase in the broader S&P 500 (INDEXSP:.INX) index.

All but two of the 35 analysts following Wells Fargo recommend clients either buy or hold the stock, according to Thomson Reuters.

Wells Fargo has increased its common dividend rate from 5 cents a share in the fourth quarter of 2009 to 30 cents a share in the third quarter of 2013.

“We've reduced our common share count by $28.4 million from the second quarter. We purchased 50.9 million shares and we executed a $400 million forward contract that is expected to settle in the fourth quarter for approximately 9.8 million shares,” Sloan said during the company’s third-quarter earnings conference call on Oct. 11.

Wells Fargo and JPMorgan Chase & Co. (NYSE:JPM) will kick off fourth-quarter bank earnings season on Tuesday with other big banks like Bank of America Corp. (NYSE:BAC), Citigroup Inc. (NYSE:C) and Goldman Sachs Group Inc. (NYSE:GS) following later in the week.

Shares of Wells Fargo closed down 0.48 percent, or 22 cents, to $45.94 a share in Friday’s session. In the past 12 months, the stock has gained 30.9 percent.

© Copyright IBTimes 2025. All rights reserved.

- MOST POPULAR IN Business