The 2% Target: Central Banks' Inflation Touchstone Faces Post-pandemic Reckoning

Top central bankers, who credit the use of a 2% inflation target with anchoring decades of stable prices, are facing the first full-on test of how well that approach to monetary policy works once prices have erupted, and how strictly they'll enforce it if damage to their economies intensifies.

By announcing an inflation goal, central bankers feel they build credibility for themselves and focus the planning of households and firms in ways that help keep inflation controlled. It's a concept that seemed supported by the facts as the use of inflation targeting spread across the developed world from New Zealand in 1990 through Europe and to the United States and Japan in 2012 and 2013.

Those decades, up to the end of the first year of the coronavirus pandemic in 2020, saw inflation largely contained.

But they also coincided with trends in globalization, technology and demographics that helped. Since the onset of the pandemic and continuing with Russia's invasion of Ukraine, those same forces may now be pushing prices in the other direction, challenging that shared monetary policy framework with a sort of adversity it has never confronted and, with ongoing supply shocks, may find hard to accommodate.

"Looking ahead, we may face a period of structurally higher inflation compared to the past two decades. The deflationary impact of localization is dissipating, and there will be inflationary pressures from global trade, climate transition, demographics and politics," said Claudio Boric, head of the monetary and economic department at the Bank for International Settlements, an umbrella group for central banks.

Yet Borio said he did not favor increasing central banks' inflation targets, an opinion that has become widespread among top policymakers - from hawk to dove - despite similarly broad concerns that the recent outbreak of inflation may be even more persistent than expected and the return to 2% all the more difficult to engineer.

At least at this point, the greater worry among central bankers is lost credibility should they not toe the line they drew for themselves.

"Is 2% sort of a magical number?" U.S. Federal Reserve Vice Chair Lael Brainard said at a forum earlier this month. "Probably not. But it's our number, and we are very committed to bringing inflation back to 2% ... Achieving that target is just core to our overall monetary policy," Brainard said, a sentiment echoed in central bank headquarters from Frankfurt to London to Tokyo.

"Let me be quite clear, there are no ifs or buts in our commitment to the 2% inflation target," Bank of England Governor Andrew Bailey said last year. "That's our job, and that's what we will do."

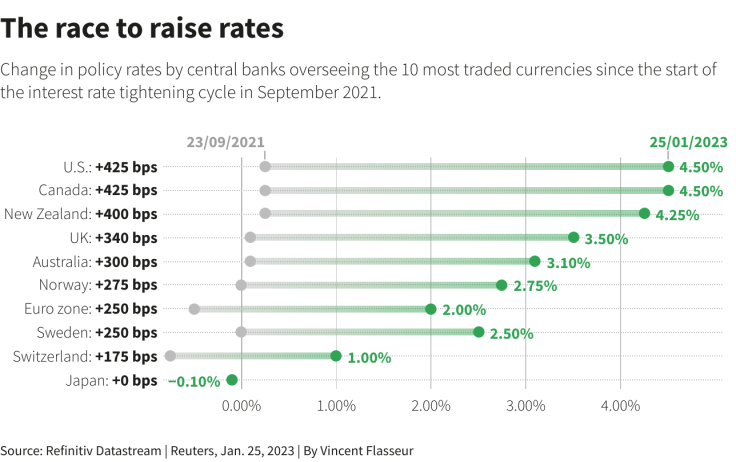

Graphic: The race to raise rates

NOT THE 'MOST SCIENTIFIC PROCESS'

The Fed is expected at its two-day policy meeting this week, as it has each year since 2012, to recommit to 2% inflation as the rate "most consistent over the longer run with the Federal Reserve's statutory mandate" from the U.S. Congress to promote "stable prices" alongside maximum employment.

Though the U.S. central bank has made major changes along the way to its "Statement on Long-Run Goals and Monetary Policy Strategy," it has never put the inflation target itself up for grabs on the grounds that a promise is a promise, and only renegotiated at great risk.

Yet the 2% number, as Brainard suggested, has no particular import in itself. Though now a global norm, it was less a product of deep analysis or statistical estimation than a best guess about an inflation rate that would capture the benefits central banks see in setting some sort of target, while remaining low enough that the public, in effect, wouldn't notice.

Coming out of the high inflation environment of the 1970s and 1980s, policymakers recognized the need to cement their own inflation-fighting credibility, and saw commitment to an announced inflation target as an easy-to-communicate way to both steer public expectations and, assuming they stuck with it, build trust.

At the same time, they wanted an inflation level consistent with long-term price stability, what former Fed Chair Alan Greenspan in one mid-1990s debate defined as a "state in which expected changes in the general price level do not effectively alter business or household decisions."

While some inflation hawks still argue that level would be zero, there's a broad consensus that modestly rising prices are healthy for an economy. It gives firms a way to adjust "real" labor costs without curbing hiring, and it gives central banks more room, through higher nominal interest rates, to manage economic downturns with interest rate cuts rather than the bond purchases and other less conventional measures used once policy rates hit the zero or near-zero level.

Officials in New Zealand, under political pressure to staunch high inflation in the 1980s, first put the idea into practice with an initial target between 0% and 2%.

"It wasn't the most scientific process in the entire world," said Michael Reddell, a former Reserve Bank of New Zealand economist. "Nobody had done this before us."

'OUR NORTH STAR'

Still, it stuck. It spread. And it arguably helped.

"I personally think that number made sense based on all the history, experience, and research ... It has served us incredibly well," New York Fed President John Williams said earlier this month. "That has helped transparency. It is helping the markets, and people understand what our North Star is."

The debate yet to be joined, however, is what happens if the North Star proves less a destination than an untouchable symbol - if the path back to 2%, already expected to be slow, stalls in the post-pandemic economy.

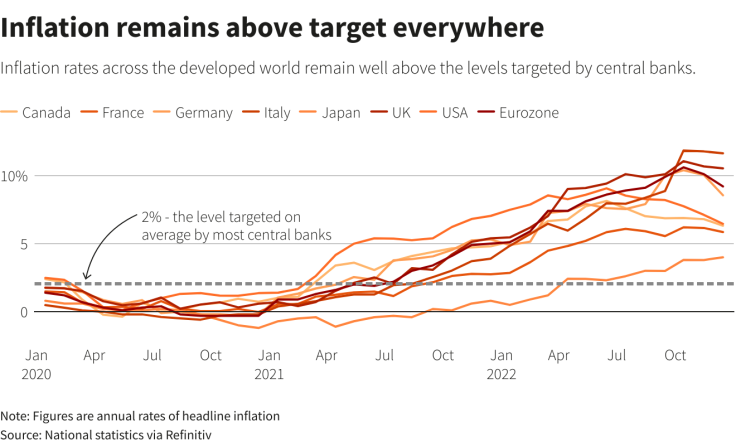

Graphic: Inflation remains above target everywhere

Economists and policymakers don't expect inflation to fall in a quick and linear fashion. Some even consider the current phase the easy part, with consensus among officials that interest rates needed to rise, and an initial slowing of inflation underway without any serious damage, notably, to job markets.

Policymakers insist they'll deliver that last mile back to their inflation goal.

But for all the focus on returning to 2% inflation, they've also acknowledged the debate could get more complicated as they study how inflation and the economy react to the interest rate increases approved so far, with more in the pipeline.

The rapid rate hikes of last year were "really important to demonstrate that resolve and to make sure people understood that 2% inflation is still the right anchor," Brainard said. "We're in a somewhat different position today ... Now we're in an environment where we're balancing risks on both sides."

Fed officials have forecast their tightening efforts could cost 1.5 million American jobs this year. Should inflation prove stickier than expected, achieving the central bank's 2% inflation goal could mean even more losses.

While recent data suggests "slightly better prospects" for an outcome where inflation slows to target without deep damage to employment or economic growth, Brainard said, "it is a very uncertain environment and you just can't rule out worse trade-offs."

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Business