Analysis: Markets Suspect New ECB Tool To Address Bond Stress Could Mimic Old Tools

Rather than invent a radical new instrument to ease bond market strains across the euro bloc, investors reckon the European Central Bank might get away with cobbling together the best parts of schemes already contained in its policy toolkit.

The ECB on Wednesday promised fresh support and the design of a potential new scheme to temper a market rout that has fanned fears of a new debt crisis on the euro currency area's southern rim.

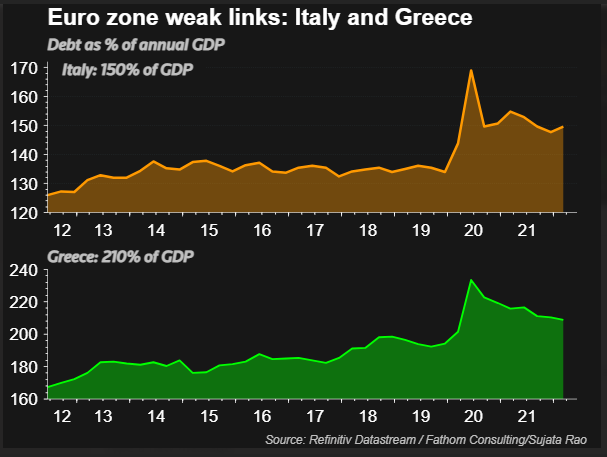

Its statement sent 10-year borrowing costs in Italy and Greece sliding as much as 40 basis points, the biggest daily move since March 2020 for the latter. In a week when yields across the bloc hit multi-year highs, the immediate reaction was one of relief.

So far, the ECB is likely to attach some loose conditions to the scheme, sources told Reuters later on Wednesday.

The ECB will spell out that the scheme's goal is simply to keep bond spreads in line with economic fundamentals, likely through quantitative benchmarks such as historical spreads, which then may be turned into a "traffic light" system to instruct staff on which country's bonds to buy and how much, the sources said.

"I hope that they have the intelligence to design (a new tool) in a way that's not too strict, keeping flexibility by purchases," said Patrick Krizan, senior economist at Allianz.

"The biggest error would be to be too committed and put themselves in a straitjacket."

The ECB has already drawn criticism for being too complacent over the risk that its plans to raise interest rates would lift borrowing costs for financially weaker nations such as Italy too far above those of safe-haven Germany.

With the bloc clearly facing that fragmentation problem, it is important for any new bond-buying tool from the ECB to be flexible, investors said.

So just like the pandemic-era PEPP emergency stimulus scheme, it would need to ditch the capital-key principle of buying bonds in relation to the size of economies, instead buying debt from countries which most need help.

GRAPHIC: Italy-Greece (

)

One suggestion is creating a new tool similar to the Outright Monetary Transactions (OMT) scheme, an unused crisis-time tool allowing for unlimited purchases of a country's debt.

The main sticking point for the original OMT programme is the requirement to sign up for a European Union bailout, often with unpopular conditions.

"The political price is quite high for the current OMT, so the ECB cannot do this alone, there must be something on the political side to design an OMT-light, which allows a country to be a bit protected," said Krizan.

Analysts said they would expect an OMT-like programme to come with conditions attached, but not ones as strict as those in the original programme. Sources told Reuters the upcoming scheme would feature loose conditions such as complying with the European Commission's economic recommendations.

Aside from fiscal requirements, "the size will be everything, the maturities of the bonds they will be looking at, these are the most important," said ING Bank senior rates strategist Antoine Bouvet.

The original OMT programme focused on buying shorter-dated bonds.

Yet another option is to design a package with traits of the OMT's precursor - the Securities Markets Programme (SMP), which did not include the OMT's strict, formal conditionality.

The SMP's positive was that it also allowed the ECB to buy bonds, without adding to stimulus already sloshing around the system, in a process economists refer to as sterilisation.

For this reason, France's central bank governor Francois Villeroy de Galhau has said bond purchases could again feature sterilisation.

The bank could also buy debt during a market stress episode, then sell gradually as conditions improve, thus avoiding increasing its overall balance sheet size, Villeroy has said.

The SMP had limited success however, and was terminated with a value of just 209 billion euros, not long after Draghi's July 2012 "whatever it takes" promise.

Still, Piet Christiansen, chief analyst at Danske Bank, expects something along the lines of the SMP.

"Sterilised purchases have been our baseline all throughout and I think that is what is to be expected, because the SMP programme was done in a way so it doesn't interfere with the monetary policy stance and the only way they could do that is by sterilizing the purchases," he said.

Investors urged the ECB to unveil detailed plans fast, warning that otherwise bond market relief would fade.

"At the end of the day people want to see action," said Francois Savary, chief investment officer at Prime Partners.

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets