Past Fed Hiking Cycles, From Sanguine To Severe, May Say Little About This One

U.S. politicians know high inflation can bring careers in public office to an early end, but it is ultimately up to the unelected officials of the Federal Reserve to control what is considered first and foremost a "monetary phenomenon."

With inflation at a 40-year high, war in Europe threatening to push it higher, and consumers feeling the weight of higher gasoline and food prices and, for many, a cut in the purchasing power of their wages, the heat is once again on the Fed.

The U.S. central bank's main tool in managing inflation is the federal funds rate, an interest rate that governs short-term loans among financial institutions and forms a sort of bedrock for other types of loans. It has been set near zero since the start of the coronavirus pandemic, and is a big reason why home mortgages, for example, have been so cheap.

That is now changing. The Fed on Wednesday, as part of an effort to control inflation, which by the central bank's preferred measure is running at 6% annually, voted to increase the federal funds rate by a quarter of a percentage point to a target range of 0.25%-0.50%. What's more, Fed policymakers laid out a plan for what amounts to a rate hike at each of their remaining six meetings this year in an old-school battle against inflation few of them saw coming.

The aim of rate-increase cycles like this are to temper consumer and business spending. If interest rates on home equity loans rise, for example, consumers won't be as likely to tap them to pay for renovations or new furniture. By curbing demand, prices should rise less quickly. Ultimately, the Fed wants inflation to be around 2% annually.

Not all of the Fed's efforts to tighten monetary policy have worked the same way. Some have led to recessions that lowered inflation but also killed jobs and economic growth, a "hard landing" in Fed parlance.

What will happen this time? There are no perfect parallels in recent decades, but each hiking cycle may hold lessons.

Fed hard and soft landings

THE 1970S AND EARLY 1980S: OIL SHOCKS, STAGFLATION, RECESSION

One of the Fed's most glaring policy mistakes also set the stage for one of its most notable, and notably painful, successes.

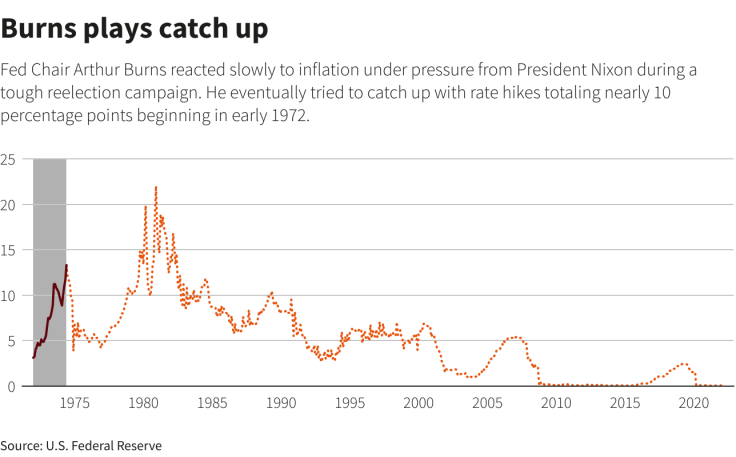

Fed Chair Arthur Burns was late to begin raising interest rates in the early 1970s after coming under pressure from then-President Richard Nixon to keep unemployment low ahead of the 1974 presidential election. Inflation took off, and while Burns eventually raised rates, larger problems were ahead.

Burns plays catch up

Current Fed officials don't like to discuss resemblances between now and the 1970s. But there are similarities. Rising wages, loose monetary policy, ultra-low unemployment, and, now, an oil shock. An embargo by Arab states in 1973 and the Iranian revolution six years later led to skyrocketing prices and some fuel rationing in the United States.

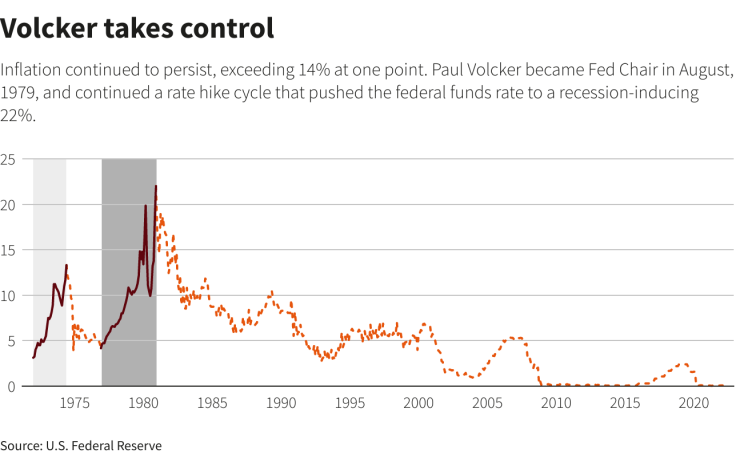

Inflation at the peak exceeded 14%, and it fell to Fed Chair Paul Volcker to break the cycle. He did, but pushed interest rates so high - home loans, at 18%, were as expensive as credit cards are today - the economy fell into two recessions in short order.

It was tough medicine some say the economy needed. But it was costly: The unemployment rate topped 10% in 1982.

Volcker takes control

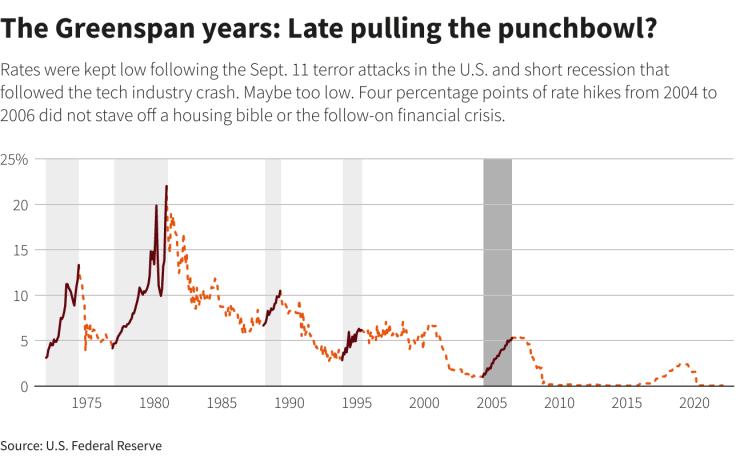

GREENSPAN: THE ANCHOR, MODERATION AND CRISIS

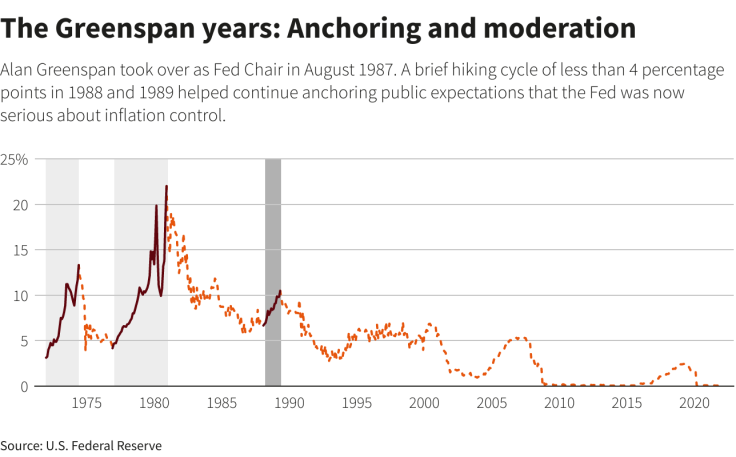

Alan Greenspan took over as Fed chief in 1987 and for much of his tenure was credited with finishing the work Volcker had begun. Under Greenspan the Fed cemented public trust that the Fed would keep inflation under control, creating a psychological "anchor" that may serve to temper actual price increases.

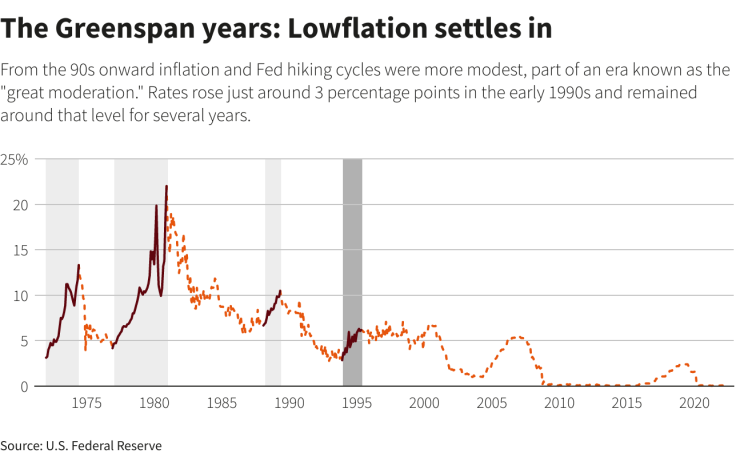

Greenspan's several hiking cycles were not as violent as Volcker's, and he is credited with what is considered a classic "soft landing" in the early 1990s when policy tightened without a recession. A short downturn started the new century, but was also attributed to a crash in technology stocks.

Greenspan's oracular standing took a hit less than two years after his departure in early 2006 from the Fed when a crisis that began in the U.S. housing market triggered a global meltdown. His willingness to leave interest rates low and take a lighter touch to banking regulation - a market-based view that investors would take rational risks if left alone - is cited by some as a cause of the crisis.

Interest rates did rise from 2004 to 2006, though the ensuing 2007-2009 recession in the United States was less about the level of borrowing costs than the earlier spread of bad mortgage bets through the financial system.

The Greenspan years: Anchoring and moderation

The Greenspan years: Lowflation settles in

The Greenspan years: Late pulling the punchbowl?

A NEW ERA?

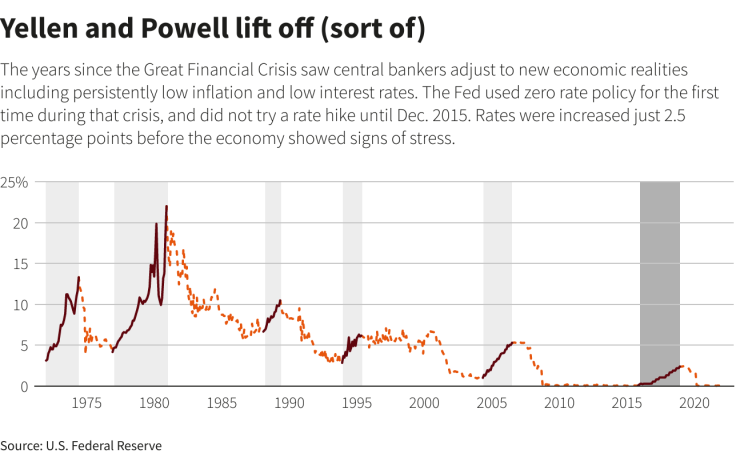

Since the financial crisis and recession more than a decade ago, U.S. central bankers have come to grips with a new world in which inflation seemed safely stuck near or even below their 2% target, and interest rates globally appeared in decline.

The Fed for the first time ever cut rates to near zero during that crisis, and they remained there until late 2015. When Fed Chair Janet Yellen and her successor, Jerome Powell, lifted rates, they did not get as far as expected. Even before the coronavirus pandemic caused a recession, the economy was showing signs of stress, and the hiking cycle was cut short.

Yellen and Powell lift off (sort of)

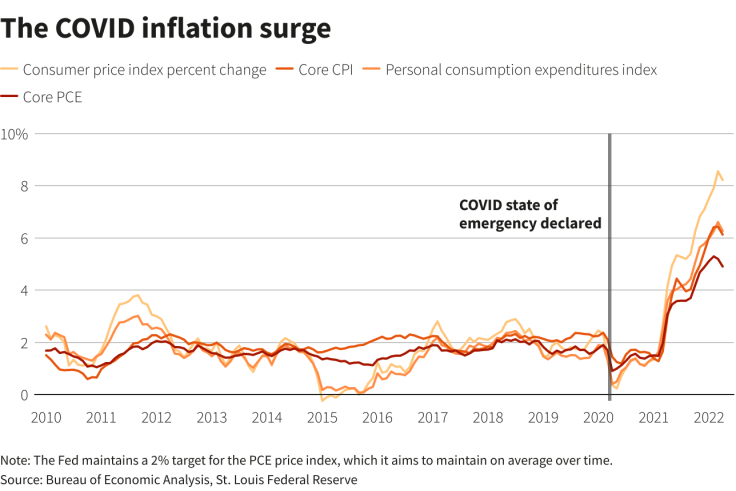

The outcome this time will depend on many things, including whether the war in Ukraine ends or intensifies. The energy shock resulting from Russia's invasion of its neighbor is already looking less persistent than those of the 1970s. Investors and analysts do not expect the Fed will need to resort to Volcker-style aggressiveness for prices to ease.

That doesn't mean it will be easy. In fact the Fed is banking that inflation snaps back to the trend in place before the pandemic. But with the economy now on a path to less globalization, more expensive supply chains, and tighter job markets, that is far from assured.

The post-COVID liftoff https://tmsnrt.rs/3wkV4fM

The COVID inflation surge

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets