Retailers' Results May Be Next Test For Rally In U.S. Stocks

Earnings results from major retailers in the coming weeks will test the strength of the U.S. stock market rally, as investors gain insight into the health of consumer spending and the fallout on company bottom lines from inflation.

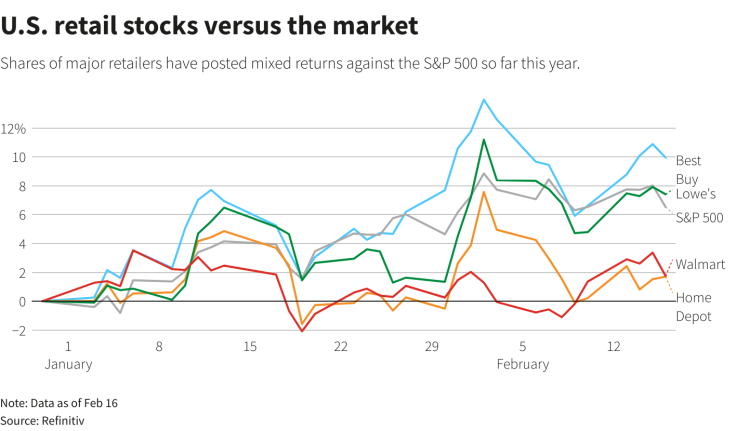

As a tepid fourth-quarter results season comes to an end, Walmart and Home Depot are set to report in the coming week, with other high-profile retailers including Best Buy and Lowe's due the following week.

How consumers are faring amid soaring prices will be a critical topic for investors, as some have become more confident that the economy will be able to avoid a severe downturn even as the Federal Reserve continues hiking rates to tamp down inflation.

One sign of economic resilience came in the past week, when monthly data showed U.S. retail sales increased by the most in nearly two years in January.

"The retail sales numbers were reasonably strong, and we want to see that confirmation come from the retailers themselves," said Paul Nolte, market strategist at Murphy and Sylvest Wealth Management.

Nolte is considering buying home-improvement retailer stocks that were hit hard in 2022 as the housing market struggled.

Stocks have run up despite underwhelming fourth-quarter earnings that has S&P 500 firms on track to post a 2.8% drop in profits from the year-ago period, according to Refintiv IBES. Other companies set to report next week include chip company Nvidia, COVID-19 vaccine maker Moderna and e-commerce firm eBay.

The S&P 500 has gained 6.5% so far in 2023 as of Thursday, with stocks bouncing back from a brutal performance last year.

Retail stocks have put up mixed returns so far in 2023. The SPDR S&P Retail ETF, which weights small and large companies fairly evenly, has jumped 17% this year. But the performance has been less rosy for some of the biggest companies.

Shares of Walmart, the world's largest retailer by sales, have gained only 1.7% in 2023, while shares of Home Depot, the top U.S. home improvement chain, are also up 1.7%. Both companies are set to report on Tuesday and will "set the stage for everyone else," according to JPMorgan retail analysts.

"We expect HD and WMT's tone on guidance and the consumer to be cautious at best," the JPMorgan analysts wrote in an earnings preview note this week. They rate Walmart shares "neutral" and Home Depot as "overweight."

GRAPHIC: U.S. retail stocks versus the market (

)

Among the other retailers set to report in the coming week are TJX Companies and Bath & Body Works.

Peter Tuz, president of Chase Investment Counsel, said he will be watching to see if retailers have been able to push up prices to match their costs.

His firm holds shares of a variety of retailers including discounter Dollar Tree and specialty retailers Crocs and Ulta Beauty, but does not own broad retailers like Walmart and Amazon.

"We are clearly emphasizing retailers in select industries versus the mass market retailers," Tuz said. "With the mass retailers, it's just harder to identify what is going to make them grow."

Investors next week will also focus on Wednesday's release of minutes from the Fed's latest meeting, when the central bank scaled back its rate hikes to a quarter-point after a year of heftier raises.

Since that meeting, data has shown U.S. consumer prices accelerating and monthly producer prices increasing by the most in seven months in January.

Together with a strong U.S. jobs report, the data has led investors to push up expectations for how high the Fed will raise rates and how long they will stay elevated, with futures now pricing in a peak rate of over 5.2% in July.

Extremely robust retailer earnings could fuel worries about a more hawkish response from the Fed, said Chuck Carlson, chief executive officer at Horizon Investment Services.

"If those numbers come in and are really, really, really strong, that could be this idea that too much good news is bad news from a Fed perspective," Carlson said.

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets