Column-Entangled Fears Of Fed Error And Ukraine Crisis: Mike Dolan

Keen to downplay anxieties about war in Europe, global investors appear to fear a monetary policy miscalculation even more.

Their problem is that two are hugely intertwined right now.

World markets gyrated over the past week as fears of a Russian invasion of Ukraine ebbed and flowed - and with them the chance of a standoff between nuclear powers in NATO and Moscow.

As Brent crude oil prices raced toward $100 per barrel as a result, market tension over how the U.S. Federal Reserve and other central banks rein in 40-year-high inflation rates went up several gears.

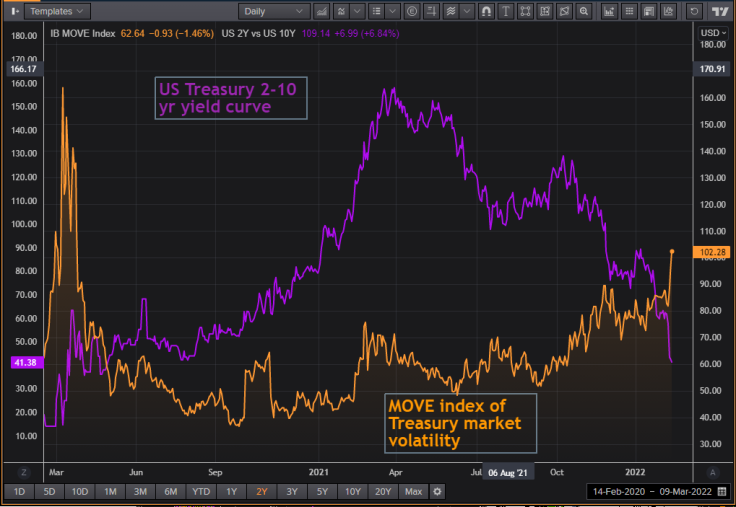

Confusion abounded as talk of emergency interest rate rises and surging oil prices sent bond yields spiking higher, even as some sought "safety" there due to the threat of conflict.

The upshot was surging volatility in U.S. Treasury markets, where the MOVE index of implied volatility hit its highest since the COVID shock of March 2020.

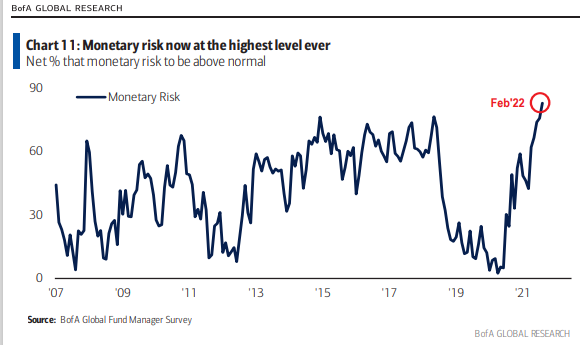

But where to focus? More global fund managers surveyed by Bank of America this month identified "monetary risks" - as opposed to geopolitical, credit, business cycle or trade risks - as the biggest threat to financial market stability than at any point in near 20 years of polling.

Although the survey was conducted before the latest ratchet in Ukraine tensions, a net 64% of respondents saw either hawkish central banks or inflation as the biggest "tail risks". Just 7% opted for the Russia-Ukraine conflict.

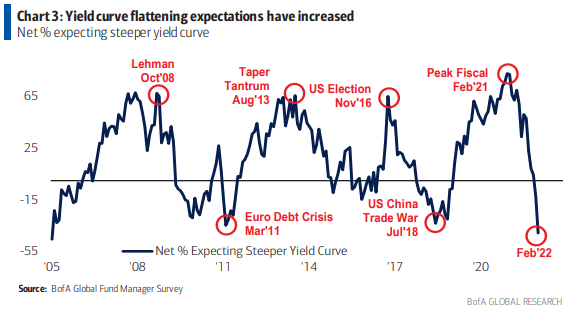

All this angst led to the highest net cash reading in portfolios since the pandemic first unfolded, heightened recession fears, and the biggest net share of funds betting on a flatter yield curve since 2005.

But the worry list speaks loudly to investor fears of central bank policy errors, in part due to the still wild pandemic-related and now geopolitical distortions. Misinterpret the inflation surge and tighten too much or too hastily - or even underestimate it, allow high inflation to fester and then have to squeeze harder eventually to wrest back control.

Neither is a great recipe for holding bonds or equities.

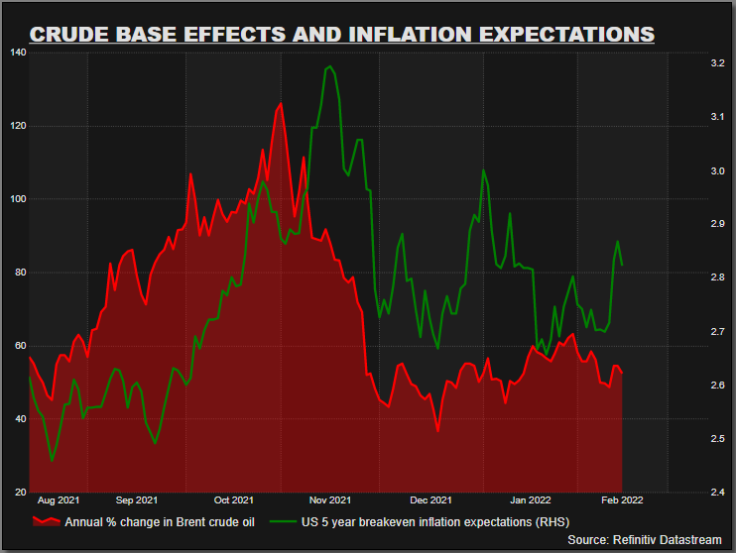

(Graphic: Crude base effects and inflation expectations,

)

(Graphic: Treasury bond volatility and the Yield Curve,

)

SELF-FULFILLING

And yet the sort of comments made by St Louis Fed chief and voting Fed policymaker James Bullard over the past week - which spurred frantic market talk of the first inter-meeting Fed hike in almost 30 years - merely reinforced those fears.

Bullard said he favoured a full percentage point increase in the Fed's main interest rate by midyear - mainly because the Fed's "credibility is on the line".

While some investors doubt the Fed will be that aggressive, it's unnerving to think central bankers might act just to be seen by markets, governments and the public to be "doing something" - even as their own analysis shows there's little they can do to ease an energy supply or geopolitical shock.

What's more, spooking markets in that direction can have a dynamic of its own if authorities then feel they then need to catch up.

PIMCO's Tiffany Wilding said she sees "virtually zero" chance of an intermeeting Fed hike and also doubts it will opt for a large 50 basis point rise in March.

But even if the "rollercoaster" ride for U.S. bond investors seemed extreme, there was danger "market pricing may become a self-fulfilling prophecy," she added.

Unigestion multi-asset manager Salman Baig also thinks the Fed will have more patience than markets now bet.

But he added: "Tightening into decelerating growth runs the risk of further slowdown, raising the concern of a policy mistake that would put a serious dent into 2022 earnings."

But all the furtive movement of tanks and troops in eastern Europe does have a role in seeding such a mistake.

Although concerns have risen about broadening price pressures, the assumption in market and policymaking circles late last year was that even a flatlining oil price would see annual base effects get crushed early this year and take pressure off headline inflation rates everywhere in 2022.

To the extent the Ukraine tensions were largely behind the 35% surge in Brent crude over the past month, then they have put paid to that hope to date. Along with the Omicron wave of COVID, this was likely a significant factor in the Fed's hawkish pivot around new year.

Instead of subsiding, year-on-year oil price gains - closely correlated to inflation expectations in bond markets - have stayed about 45% since November. If they had stayed at late November prices, those gains would have been wiped out by now.

The near 5% recoil in Brent on Tuesday amid some tentative de-escalation of the Ukraine standoff gives a small glimpse of how much the latest oil spike was down to those tensions. And indeed many fund managers have upped oil exposure precisely as a portfolio hedge to those geopolitical tensions.

The picture is amplified in Europe of course due to the quadrupling of natural gas prices over the past year - and Tuesday's Ukraine relief saw a near 10% retreat in those.

And so these monetary and geopolitical risks are joined at the hip and hard to disentangle completely. War and an energy shock could simply up the risk of hawkish error. Avoiding those may be needed to confirm the still-benign year end forecasts.

(Graphic: BofA chart on funds' fear of monetary policy risks,

)

(Graphic: BofA chart on funds' yield curve expectations,

)

The author is editor-at-large for finance and markets at Reuters News. Any views expressed here are his own

(By Mike Dolan, Twitter: @reutersMikeD; Editing by David Holmes)

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets