As ECB Pares Back Stimulus, Investors Alert For Fragmentation Risk

As the European Central Bank races towards the stimulus exit to tame record-high inflation, angst about whether it can contain stress in weaker economies is creeping back into corners of bond markets.

For sure, indicators of stress are comfortably below peaks seen at the height of the 2020 COVID-19 crisis, and nowhere near levels of the 2011-2012 euro zone debt crisis. Cohesion is stronger after the pandemic and war in Ukraine, while an 800 billion euro recovery fund supports the bloc and France last month re-elected a pro-European president.

Yet with inflation at 7.5%, ECB bond-buying stimulus will end soon -- challenging weaker southern European states and putting fragmentation risks back in focus as their government borrowing costs versus safer Germany shoot higher.

"It is something I worry about," said DZ Bank rates strategist Christian Lenk. "The million dollar question is where are bond spreads too wide that the ECB intervenes."

Here's a look at what stress indicators show.

1/ CANARY, COALMINE

If the premium investors demand to hold bonds from lower-rated states rises too far above top-rated Germany, the ECB's ability to transmit monetary policy effectively is challenged. So-called fragmentation risk could heighten economic instability.

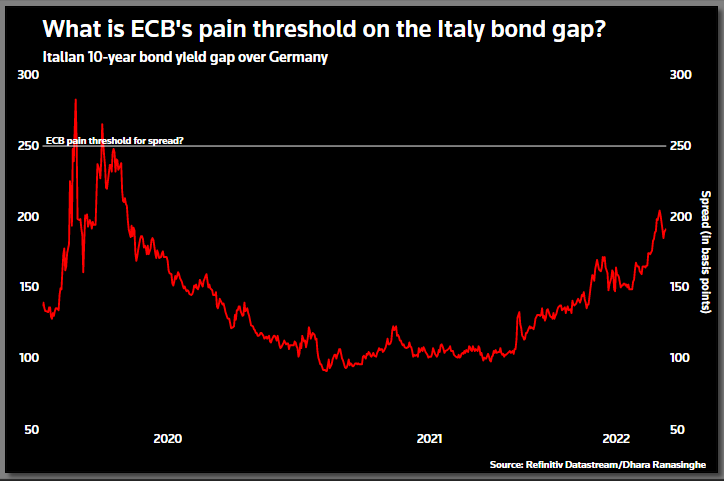

At 200 basis points (bps), highly-indebted Italy's 10-year bond yield gap over Germany is below peaks of more than 300 bps hit in March 2020 and 2018, when a new populist Italian government clashed with the European Union over budget policy.

But it is near the widest levels since May 2020 after widening 65 bps this year. Talk of ECB measures to contain spreads has grown; ING says markets could test the ECB's resolve by pushing Italy's spread to 250 bps.

Graphic:Italy's 10-year bond yield gap over Germany-

A blowout in this spread prompted the ECB to launch its emergency stimulus scheme in March 2020, as a pandemic-induced financial rout raised fears about the currency bloc's viability.

2/ INSURANCE POLICY

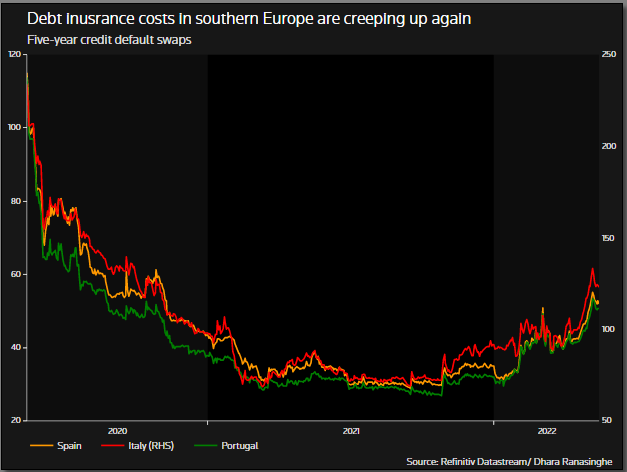

The cost of insuring against a debt default in southern Europe has risen recently to the highest since 2020, although credit default swaps (CDS) sit below previous peaks.

Graphic:CDS in southern Europe creeping higher again-

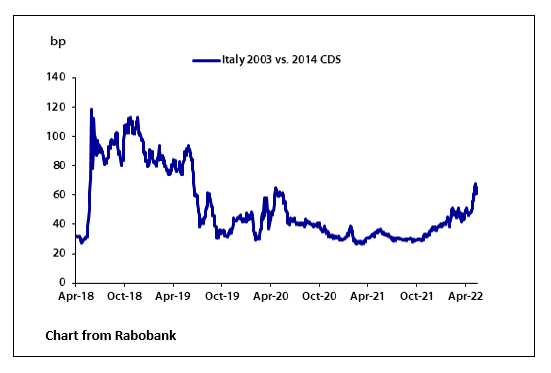

Another gauge of fragmentation risk is the spread between CDS contracts issued under trade body International Swaps and Derivatives Association's (ISDA) 2003 definition and those issued under its 2014 guidelines. The latter includes guidance on redenomination risk and carries a premium.

The gap between two such Italian CDS contracts is roughly 64 bps, around the widest since April 2020, Rabobank said.

Rabobank's head of rates strategy Richard McGuire notes the spread was double current levels in 2018. "From an historical perspective this gives investors cause to be alert rather than alarmed," he added.

Graphic:Italy 2003 CDS vs Italy 2014 CDS-

3/ LIFE AFTER 2013

How investors trade bonds issued before and after 2013 is also worth watching.

That year, regulators said European government bond contracts should contain collective action clauses (CACs), meaning majority bondholder approval is needed for a restructuring including a change in the currency of payment.

UniCredit estimates that roughly 415 billion euros of Italian bonds are not covered by CACs.

An Italian bond issued in 2008, before the CAC ruling and maturing next year, has risen 72 bps this year. A one-year Italian bond issued in 2022 and maturing 2023, is up a similar amount.

If the 2022 bond outperforms its non-CAC peer, that would suggest fragmentation worries are returning.

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets