Fed Hawks, Doves Agree On Liftoff. What Happens Next Could Be A Battle

U.S. Federal Reserve officials agree inflation is too high and that interest rates should be increased at the upcoming meeting in March.

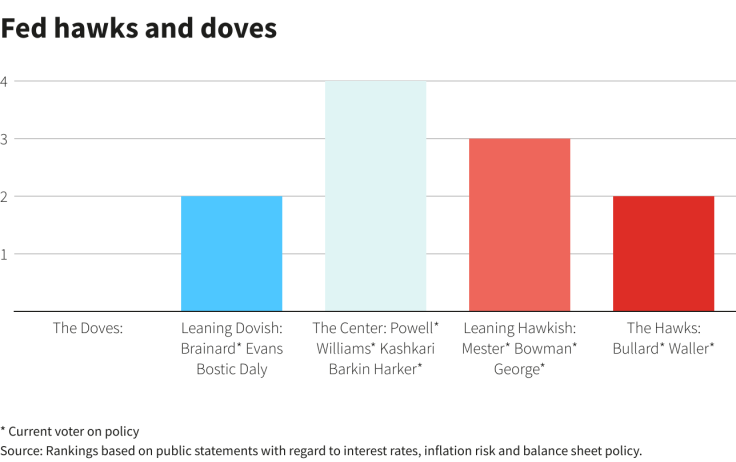

But if everyone seems a "hawk" for now, determined to bring down the highest inflation rates in 40 years, the 14 policymakers currently participating in Fed debates still have different ideas about the risks the U.S. economy is facing and how quickly the central bank needs to raise interest rates and take other steps to tighten credit.

The "doves" haven't gone away.

Rather, they are keeping a wary eye on how quickly inflation may slow, and how employment, wages and economic growth respond to rising interest rates. Depending on how these play out as the year progresses, the natural tension between hawks and doves may reemerge.

Indeed what distinguishes a Fed dove from a hawk these days is more a matter of nuance - a bit more faith, perhaps, that world supply chains will get sorted and ease inflation, or, on the other side, a bit more willingness to raise rates faster now just in case they don't.

Fed hawks and doves -

It's captured perhaps most vividly in the divide between a Charles Evans, president of the Chicago Federal Reserve, betting the Fed will get away with "less ultimate financial restrictiveness" than in prior years, and a James Bullard, head of the St. Louis Fed, thinking the Fed will have to carry more of the load in inflation control and that "it's important to get moving."

Fed officials are also drawing lines around what to do with its stash of asset holdings, with some saying that outright sales of the portfolio might be needed as a way to further tighten financial conditions

WHY ARE INTEREST RATES RISING?

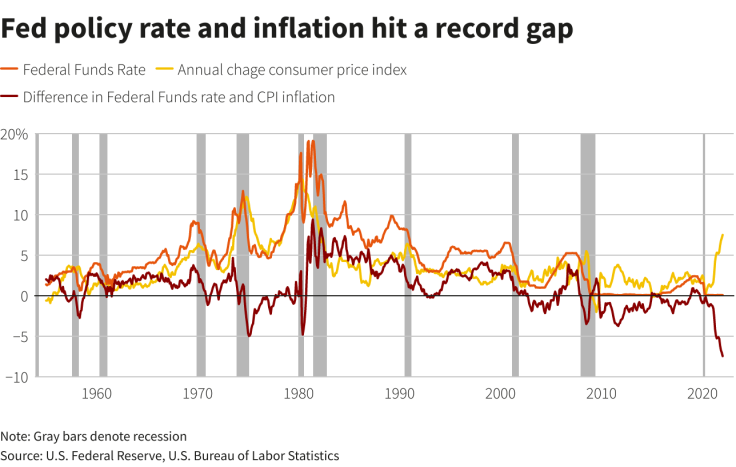

Yet even Evans agrees the Fed's current policy is "wrong-footed" given that consumer prices are rising 7% annually. The Fed aims to hold inflation to 2%. While the central bank uses a slightly different measure for its inflation target, that too has been running far above the Fed's comfort zone.

Monetary policy, meanwhile, remains at full throttle, stoking an economy that at present has no shortage of cash to spend and no lack of desire to spend it. The target interest rate remains near zero, where it was set at the start of the global coronavirus pandemic to fight a sharp economic downturn. While the Fed has curbed the pace of its monthly bondbuying - aimed at stabilizing financial markets and keeping borrowing rates low - there is no firm plan yet to shrink the nearly $9 trillion in government securities the central bank now holds.

Fed policy rate and inflation hit a record gap -

Given the situation, increases in the Federal Reserve's target interest rate are inevitable, and will likely be approved in quarter point increments at the next several Fed meetings.

As the Fed raises its policy rate, other interest rates tend to rise as well. Home and auto loans become more expensive as a result. Companies may pay more to finance their operations.

In theory that all helps slow the pace of price increases.

Both hawks and doves will be watching.

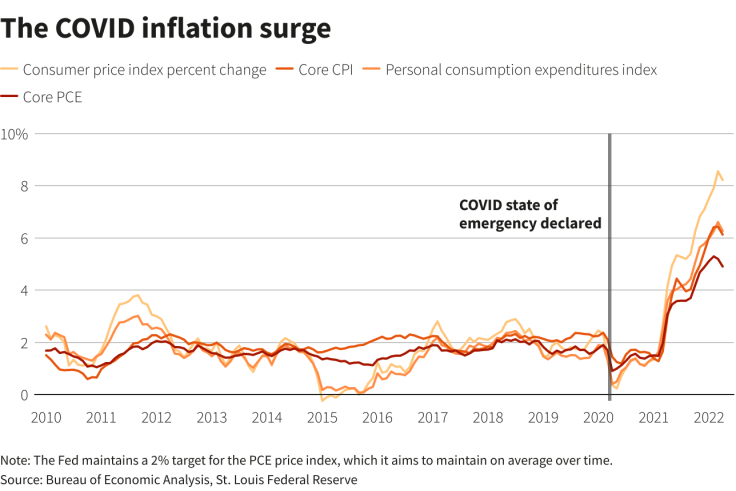

The COVID inflation surge -

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets