Fed Tapering: Winners & Losers When QE Ends

The Federal Reserve is close to tapering down its $85 billion-a-month asset purchase program known as quantitative easing, or QE. Most economists expect the central bank to make the move by the end of this year, and a sizeable number expect reduced buying to begin as early as September.

In Wednesday’s press conference, Fed Chairman Ben Bernanke will likely reiterate his comments from his recent congressional testimony, including how bond-buying may be adjusted up or down conditionally based on the incoming data and the Fed’s economic outlook.

“We expect the chairman to highlight that tapering is not necessarily tightening, but instead is a slowing in the pace of accommodation,” Barclays Capital economist Michael Gapen said in a research note.

Whether Bernanke succeeds in convincing markets that tapering is conditional on incoming data as opposed to a foregone conclusion -- and that a willingness to taper should be separated from the remaining components of the exit strategy -- remains an open question. Markets will likely continue to view any move to withdraw policy as the first step of many and, as a result, volatility is likely to remain elevated as the market balances incoming data with Fed communications about its policy stance, Gapen said.

Here’s a look at some of the potential winners and losers when the Fed eventually tapers, according to UBS strategist Boris Rjavinski’s analysis of different types of U.S. investors.

Winners

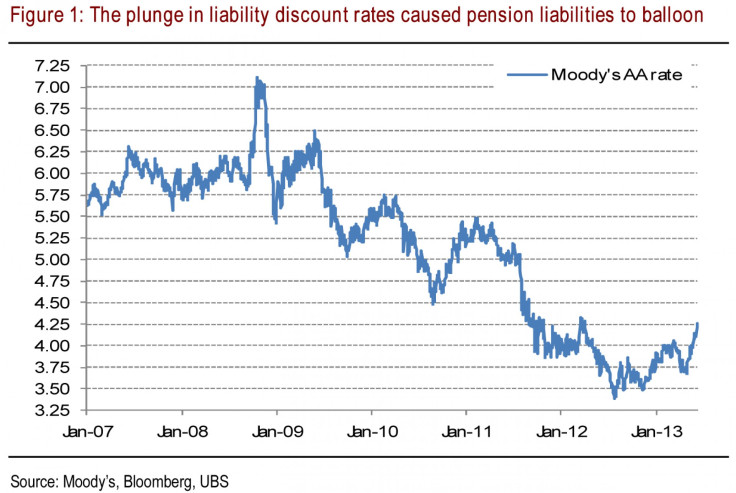

1) Defined Benefit Corporate Pension Funds

In recent years, persistently low interest rates in the bond market have been a drag on pension funds.

The funding shortfall bedeviling the 100 largest U.S. corporate pension funds rose for a second straight year in 2012, according to an analysis by Towers Watson. The gap between what these corporations, all publicly traded, will owe retired workers and how much they have put aside jumped 17 percent, from $252.7 billion at year-end 2011 to $295.2 billion at year-end 2012. By comparison, these companies had a pension surplus of $86 billion in 2007.

Under the traditional formula, companies determine the value of their pension plans and their pension liabilities based on a discount rate pegged to bonds. Plunging interest rates caused liabilities to balloon and pension funded ratios to deteriorate.

Chrysler announced last Friday that it plans to freeze pensions for 8,000 salaried employees at the end of the year, joining a growing group of companies seeking to limit the amount of money they have to set aside now for future retirees.

Ford Motor Company (NYSE: F)’s unfunded liability expanded to $18.7 billion at the end of 2012, prompting the company to embark on a pension buyout plan for salaried workers. Ford's pension plans had strong real-world returns -- up more than 14 percent. But the automaker had to lower its discount rate to 3.84 percent from 4.6 percent, which created a bigger liability on its balance sheet.

The number of terminated pension plans has jumped since QE was introduced. While there were only 94 pension terminations in 2006 and 67 in 2008, that number jumped to 144 in 2009 and has climbed every year since.

The Pension Benefit Guaranty Corp., the federal agency that insures private-sector pension plans, reports that the number of plans it insures for individual employers plummeted from 112,208 in 1985 to 25,600 in 2011.

Some, perhaps most, of the plans went bust because of the economic fallout from the financial crisis.

“In a perfect world we could separate the effects of the economy and QE, but this simply is not feasible,” Rjavinski said. “Still, we think that QE at a minimum has accelerated the demise of some pensions.”

2) Life Insurers

U.S. life insurers, a group led by Metlife Inc (NYSE: MET) and Prudential Financial Inc (NYSE: PRU), are also feeling the squeeze from rock-bottom interest rates.

A recent report from the U.S. Treasury Department warned that a sustained low interest rate environment may lead insurers to "reach for yield” by taking on more investment risks.

Life insurers are similar to defined benefit pensions. They typically hedge by buying long duration rate bonds, receiving fixed-in swaps or buying the corresponding options. “As yields marched lower, the cost of these hedges kept rising, and so were concerns regarding capital adequacy,” Rjavinski said, adding that a sizable increase in yields should alleviate this problem.

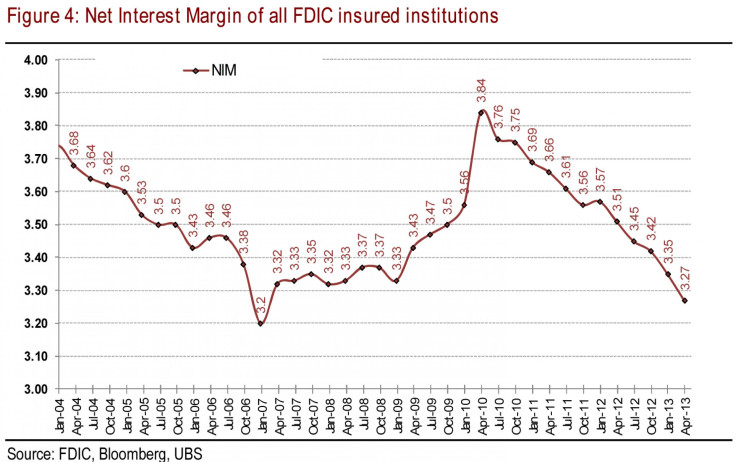

3) Banks And Depository Institutions

Financials are the most undervalued group in the market, and Fed tapering will eventually be a boon for the sector. Net interest margin (NIM) is banks’ primary driver of earnings. But as the Fed purposely pushed down long-term rates, NIM has compressed to multiyear lows.

The NIM compression began before the introduction of QE2, and continued throughout Operation Twist and the current QE3. Rising rates will significantly improve banks' lending profits.

Nearly every bank executive seems to be predicting his bank will make money when rates rise, and bank investors seem to be siding with the CEOS. Shares of the big four banks, Bank of America Corp. (NYSE: BAC), Citigroup Inc. (NYSE: C), JPMorgan Chase & Co. (NYSE: JPM) and Wells Fargo & Co. (NYSE: WFC), have all been rising lately.

In his annual letter to shareholders published in April, JPMorgan CEO Jamie Dimon predicted that the biggest U.S. lender would make $5 billion over the following 12 months if interest rates were to suddenly rise 3 percent.

4) Money Market Funds

The prolonged period of zero short-term interest rates and flat yield curves has also posed an existential challenge to money market fund managers.

UBS found that an average money fund has been yielding essentially zero after fees. Consequently, money fund assets have dwindled by about 35 percent since early 2009 as investors desperately looked for other alternatives.

Money funds are not out of the woods, though, especially given the possibility of major regulatory changes in the space in the next one to two years. But they might finally get some breathing room.

Losers

1) U.S. Treasury Department

Last year, the Fed shipped about $80 billion of its earnings to the Treasury. Large Fed remittances have become a significant source of revenues for the government in balancing its finances.

UBS economists estimate the federal budget deficit to be about $670 billion in fiscal year 2013. If the Fed rebates roughly the same $80 billion this year, it will cover about 12 percent of the deficit.

Therefore if the Fed scales back new purchases substantially while the size of its existing holdings, especially of mortgage-backed securities, decline then the amount it earns on its portfolio may decline a lot. Furthermore, rising rates, which result in a commensurate price decrease, almost certainly will cause hefty mark-to-market losses on the Fed’s portfolio. “The Fed’s remittances are linked to realized income, not unrealized losses, but if it eventually does sell at a loss then the amount it can rebate to the Treasury will fall,” Rjavinski said.

The Fed appears to be preparing for this problem already. Below is the explanation Bernanke provided in his February Congressional testimony:

"Another aspect of the Federal Reserve's policies that has been discussed is their implications for the federal budget. The Federal Reserve earns substantial interest on the assets it holds in its portfolio, and, other than the amount needed to fund our cost of operations, all net income is remitted to the Treasury. With the expansion of the Federal Reserve's balance sheet, yearly remittances have roughly tripled in recent years, with payments to the Treasury totaling approximately $290 billion between 2009 and 2012.

"However, if the economy continues to strengthen, as we anticipate, and policy accommodation is accordingly reduced, these remittances would likely decline in coming years. Federal Reserve analysis shows that remittances to the Treasury could be quite low for a time in some scenarios, particularly if interest rates were to rise quickly."

But Bernanke quickly added:

"However, even in such scenarios, it is highly likely that average annual remittances over the period affected by the Federal Reserve's purchases will remain higher than the pre-crisis norm, perhaps substantially so. Moreover, to the extent that monetary policy promotes growth and job creation, the resulting reduction in the federal deficit would dwarf any variation in the Federal Reserve's remittances to the Treasury."

Toss-Up

1) Retail Bond Fund Investors

Many retail investors have faithfully followed the Fed’s lead into bonds, including long-duration mutual funds and ETFs. Some estimates show that net inflows into all bond and income mutual funds in the four-year period 2009-2012 may have reached $1 trillion.

“With the 10-year Treasury yield about 60 basis points above its July 2012 low, it is not hard to see why some retail investors are feeling buyer’s remorse,” Rjavinski said. Those who invested in popular long-maturity funds can be down as much as 12 percent or more.

On a positive note, Rjavinski noted that retail investors could see much more appealing reinvestment rates. “They should be pleased if rates jump to more palatable levels,” he said. “The journey will be rough, but the destination should be pleasant.”

2) Fixed Income Asset Managers

Quantitative Easing has been a mixed blessing for fixed income managers. UBS strategists think that fixed income managers will generally welcome the eventual taper. Some of the challenges to their business models should start to fade if yields move up and central banks’ influence on interest rates weakens. However, they probably will suffer outflows from their funds and will need to mitigate duration risk.

© Copyright IBTimes 2025. All rights reserved.

- MOST POPULAR IN Business