Long-Term Capital Gains Tax Rates in 2019

Did you know that the IRS encourages long-term investing? Specifically, the capital gains tax the IRS charges Americans on their investment profits is considerably less when you've held an investment for longer than a year.

This article originally appeared in the Motley Fool.

The IRS recently announced its inflation-related adjustments to the tax code for 2019, and one of those changes was the revised long-term capital gains tax brackets. Here's a quick guide to the 2019 long-term capital gains tax rates, so you can determine whether you'll pay 0%, 15%, or 20% on your 2019 investment profits.

What is a long-term capital gain?

The term "capital gain" simply refers to a profit made by selling an asset for more than you paid for it. As an example, if you paid $3,000 for a stock investment and sell it for $4,000, you'd have a $1,000 capital gain on the sale.

The IRS splits capital gains into two distinct baskets for tax purposes: long- and short-term capital gains. A short-term capital gain occurs if you owned the asset for a year or less. If this is the case, the gain is considered ordinary income and is taxed at your applicable marginal tax rate.

On the other hand, if you owned the asset for at least a year and a day, any profit made upon the sale of the asset is considered a long-term gain and is taxed at preferential rates.

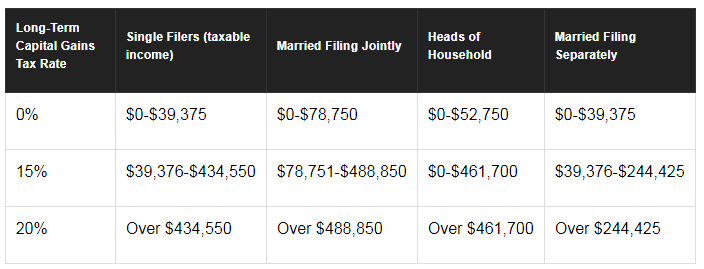

The long-term capital gains tax brackets

It may seem odd, but the income ranges long-term capital gains tax brackets look rather different than those for ordinary income and short-term gains. While the Tax Cuts and Jobs Act made significant changes to the income thresholds for the ordinary income brackets, it didn't make any such changes to the long-term capital gains brackets.

With that in mind, here's a look at the 2019 long-term capital gains tax brackets:

In addition to the rates listed in the table, higher-income taxpayers may also have to pay an additional 3.8% net investment income tax.

How much could the long-term capital gains tax rates save you?

To illustrate just how valuable these long-term capital gains tax rates can be for investors, here's a simplified example.

Let's say that you're married and that you and your spouse file a joint tax return. To keep the numbers simple, we'll say that you have combined taxable income of $200,000 in 2019, which puts you firmly in the 24% marginal tax bracket.

Now, let's say that you have a stock investment that is worth $10,000 more than you paid for it just over 11 months ago. If you were to sell it now, the gain would be taxed as ordinary income, and it would add $2,400 to your tax bill. On the other hand, if you wait another month to sell it, it would qualify for the 15% long-term capital gains tax rate, which would reduce your tax hit by $900 to $1,500. In other words, a $7,600 effective gain on the investment would become $8,500.

Think twice before selling winners after just a few months

The long-term capital gains tax rates are designed to encourage long-term investment and are yet another reason why it can be a bad idea to move in and out of stock positions frequently.

Specifically, it can be tempting to sell winning stock positions quickly in order to lock in gains. However, be aware that the higher tax rates that apply to short-term gains can take a big bite out of your profits. It's generally a bad idea to sell stocks simply because they went up in value, as long as the initial reasons you bought the stock still apply. And the lower long-term capital gains tax rates make buy-and-hold investing even more attractive.

The $16,728 Social Security bonus most retirees completely overlook

If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $16,728 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after. Simply click here to discover how to learn more about these strategies.

The Motley Fool has a disclosure policy.

- MOST READ