Shares Slump After Retail Giants Sound Stagflation Alarm

World stock markets suffered more heavy falls on Thursday after stark warnings from some of the world's biggest retailers about just how hard inflation is biting gave Wall Street its worst day in almost two years.

Bond markets rallied in the dive for safety and on bets that interest rate rises may get recalibrated, but it was the gloom striking down equities after Wednesday's $25 billion wipeout in U.S. retail giant Target's shares that dominated the action. [.N]

Wall Street, which haemorrhaged $1.5 trillion altogether, reopened another 1% lower, Europe dropped 2% as its retailers slumped 2.5% [.EU], and Chinese tech firms tumbled overnight too [.SS], all of which left MSCI's world stocks index sliding toward 1-1/2 year lows.

"Target and Walmart coming out with disappointing numbers has really, really spooked people," said Close Brothers Asset Management's Chief Investment Officer Robert Alster.

"We are going to see a raft of downgrades to U.S. GDP (forecasts) now... it really looks like we are running into a faster slowdown than we expected."

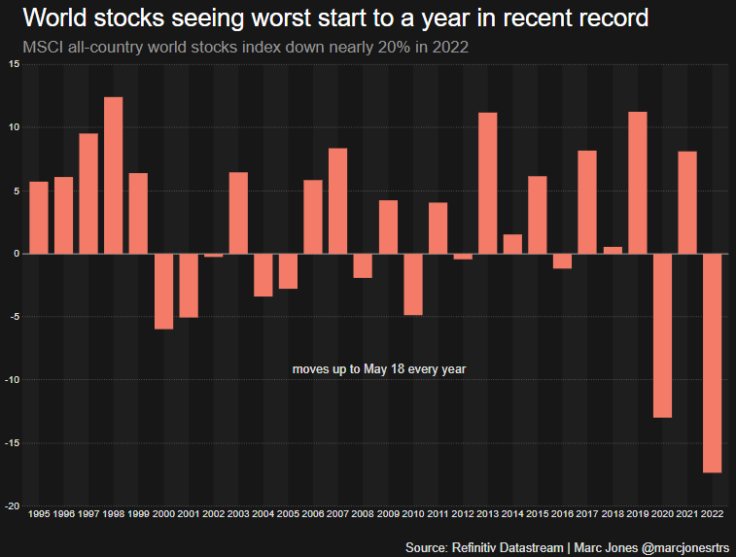

That MSCI world index is now down almost 18% in what is its worst start to a year on recent record.

Signs of spluttering economies were highlighted as weekly U.S. unemployment benefit claims figures rose slightly and a survey of businesses in the Mid-Atlantic region showed confidence about the months ahead at 13-year low.

Goldman Sachs now estimates a 35% probability of a U.S. recession in the next two years, while Morgan Stanley's sees a 25% chance of one in the next 12 months.

The fresh Wall Street selling came after Wednesday's rout knocked 4% off the S&P 500 and 5% off the Nasdaq [.N] as megacap giants Amazon, Nvidia and Tesla all dropped close to 7% and Apple tumbled 5.6%.

Asia-Pacific shares ex-Japan snapped four days of gains to wilt 1.8%, dragged down by a 1.65% loss for Australia's resource-heavy index, a 2.5% drop in Hong Kong. Tokyo's Nikkei shed 1.9% too.

Tech giants listed in Hong Kong were hit particularly hard, with the index falling nearly 4%. China's online behemoth Tencent sank more than 6% after it reported no revenue growth in the first quarter, its worst performance since going public in 2004.

China's technology and property sectors are still reeling from a year-long government crackdown and slowing economic prospects stemming from Beijing's strict zero-COVID policy, even though soothing comments from Vice Premier Liu He to tech executives buoyed sentiment on Wednesday.

(Graphic- Worst start to a year for world stocks:

)

CENTRAL FOCUS

The focus remained on what central banks will now do as they walk the tightrope of trying to regain control of inflation, which is now at 40-year highs in some countries, without causing painful recessions.

"We will have to discuss what we can do together in our respective areas of responsibility to avoid stagflation scenarios," German finance minister Christian Lindner said as he arrived for a two-day meeting of top central bankers near Bonn.

Two top U.S. central bankers said on Wednesday that they expect the Federal Reserve to downshift to a more measured pace of rate rises after July, but in Europe traders were suddenly pricing in as many as four ECB hikes. It hasn't raised interest rates for over a decade.

However, while things haven't reached the point of no return, they are seemingly heading in the direction of "out of control. That is probably the most worrying part for the market," said Hebe Chen, market analyst at IG.

In the currency markets, the U.S. dollar eased back 0.3% against a basket of major currencies, after a 0.55% jump overnight that ended a three-day losing streak.

The euro gained nearly 1% on the ECB rate rise view, while the Aussie dollar jumped 1.6% and New Zealand's kiwi bounced 1.2%, helped by an easing of Shanghai's COVID lockdown in China. [FRX/]

U.S. Treasuries continued to rally with yields - which move inversely to prices - as low as 2.77% while Europe's risk-adverse mood saw Germany's 10-year bond yield fall well back below the closely watched 1% level. [GVD/EUR]

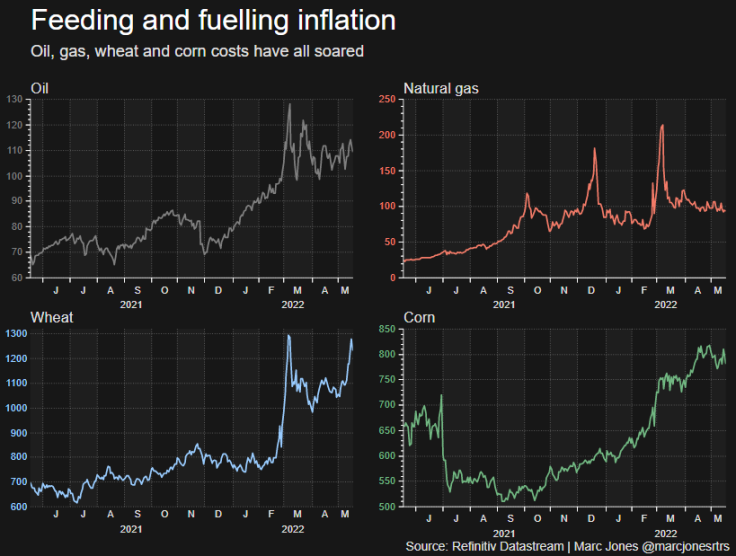

Inflation worriers watched oil prices ease again too, as fears over slower economic growth and signs that Venezuelan oil might be coming back onto the market outweighed lingering fears over tight global supplies.

Brent crude went from $110.41 to $108.04 per barrel in London trading, while U.S. crude dipped to $108.05 a barrel and gold, which has fallen more than 12% since March, clawed up to $1,830 an ounce. [GOL/]

(Graphic- Inflation surge driven by food and energy prices:

)

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets