Chinese Economy In 2013: Following The Old Growth Pattern?

Four years after China’s economy was rescued by a four-trillion-yuan ($586 billion) stimulus plan, its economic growth continues to be shored up by an unsustainable reliance on credit.

The huge loan-filled stimulus helped China, which was then the world’s fourth-largest economy, surpass Germany in 2008 and Japan in 2010. It was clear that, as credit grew, so did gross domestic product growth.

According to the World Bank, in the 30 years after Deng Xiaoping initiated economic reform, investment accounted for six percentage points to eight percentage points of the China’s 9.8 percent average annual GDP, while improved productivity contributed two percentage points to four percentage points.

In 2012, investment spending accounted for half of all GDP growth in China.

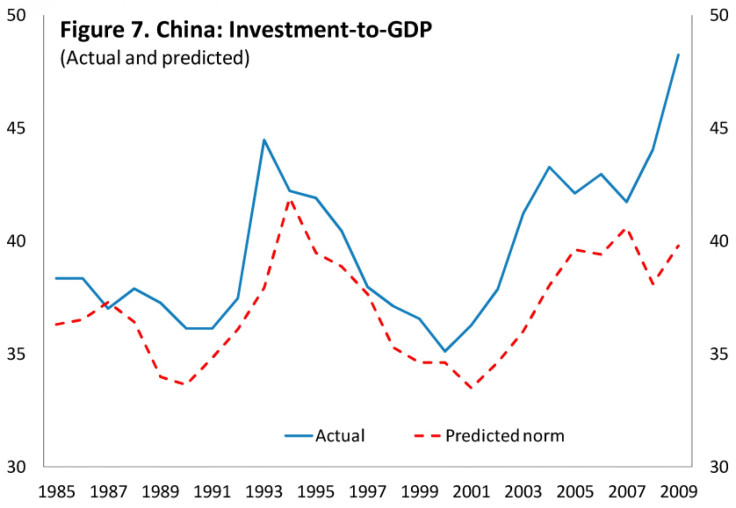

A recent International Monetary Fund working paper concluded that the level of over-investment in China is equivalent to about 10 percent of GDP, and perhaps as high as 20 percent.

Authors Il Houng Lee, Murtaza Syed and Liu Xueyan said: “Even allowing for elevated investment levels associated with most economic take-offs, the econometric evidence suggests that China is over-investing.”

China’s money supply has grown significantly faster than output in the past decade. In 2012, the growth rate of M2 (broad money supply) was about 14 percent, relatively low by historical standards, but still significantly higher than the nominal GDP growth rate. As a result, China’s M2-to-GDP ratio has surpassed 189 percent, the highest in the world.

Data released over the weekend showed that China, now the second-largest economy in the world, began 2013 with the same old model. Growth for the first two months of the year was driven mainly by exports and real estate.

Property sales jumped 49.5 percent year-over-year in terms of floor area sold. Cement output, a useful proxy for construction activity, rose 10.8 percent year-over-year, doubling December’s rate.

Thanks to the incredibly buoyant property market, fixed-asset investment powered ahead in January and February. Fixed-asset investment accelerated more than expected, at 21.2 percent year-over-year in the first two months, up from 19.8 percent in December.

“The goal of consumer-led growth remains a pipe dream for now,” Mark Williams and Qinwei Wang, of Capital Economics, said in a note to clients. Retail sales during the holiday period grew at the slowest rate since 2004.

Meanwhile, the supply of massive liquidity has triggered inflation.

In February, China’s inflation accelerated to 3.2 percent year-over-year from two percent in January, faster than the market had expected. While the February figure was distorted by Lunar New Year effects, the fact that consumer-price index inflation averaged 2.6 percent year-over-year for the first two months of the year, 0.5 percentage points higher than the fourth-quarter average, suggests that underlying inflation pressure is building. This will gradually restrict policymakers’ room to maneuver.

Even with a massive credit expansion, the economy grew last year at the slowest rate in more than a decade. But if China’s economy is to avoid running into overcapacity, credit growth will soon have to slow. This in turn will, at the very least, halt the ongoing economic turnaround, according to Williams and Wang.

© Copyright IBTimes 2026. All rights reserved.

- MOST POPULAR IN Business