Column-Yellen Could Face G7 Pressure On Dollar: McGeever

U.S. Treasury Secretary Janet Yellen has barely made any public comment on the dollar's exchange rate since she assumed office in January last year, but she may have to find her voice soon.

She will meet other Group of Seven finance ministers and central bankers in Bonn this week against one of the most challenging global economic backdrops in decades, at the heart of which is the role of the seemingly omnipotent U.S. dollar.

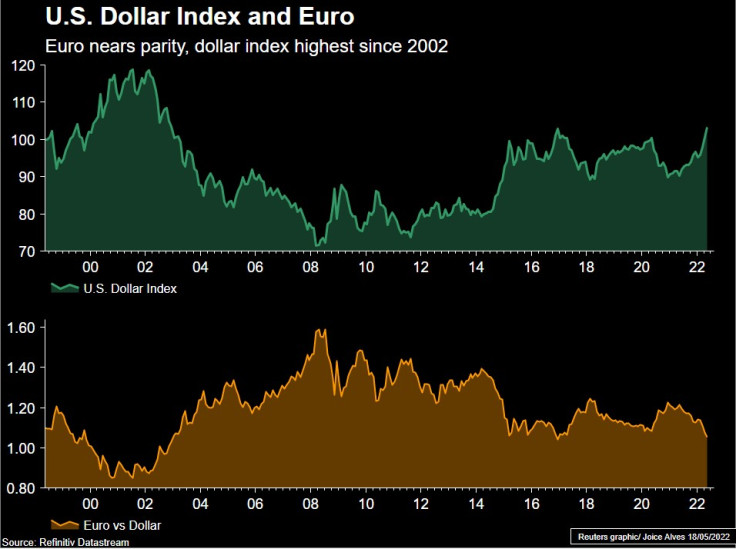

Measured against a basket of major currencies it is the strongest it's been for 20 years. Japanese officials have expressed discomfort with the yen's weakness, and now euro zone officials are squirming at the inflationary impact of the euro also approaching a 20-year trough and parity with the dollar.

Bank of France governor Francois Villeroy de Galhau said this week that the European Central Bank will "carefully monitor" exchange rate developments, adding: "A euro that is too weak would go against our price stability objective."

(GRAPHIC- Dollar index & euro since euro launch:

)

Yellen should be quite happy with a high exchange rate - it helps dampen the impact of import prices on inflation, which is running at its highest in 40 years and is now the most pressing issue for consumers, business, and policymakers alike.

Treasury has largely adhered to the policy set out in 1995 by then Treasury Secretary Robert Rubin, who declared that a strong dollar was in the U.S. national interest and the phrase became a mantra for him and his successors for many years after.

The policy doesn't refer to specific levels, but was designed to dissuade markets from speculating about any government bias towards trade-enhancing currency weakness and help keep U.S. bond yields and inflation expectations under control into the bargain.

Former President Donald Trump threw all that out the window as part of his broader shift towards protectionism, and often expressed support for a weaker dollar. His Treasury Secretary Steve Mnuchin also infamously welcomed a weaker dollar before being forced to row back.

Yellen, of course, is from the Democratic side of the political aisle. But she has still barely raised the issue of exchange rates since replacing Mnuchin.

At her Senate confirmation hearing she said she believed in market-determined exchange rates, and that targeting a weaker currency to gain commercial advantage is "unacceptable".

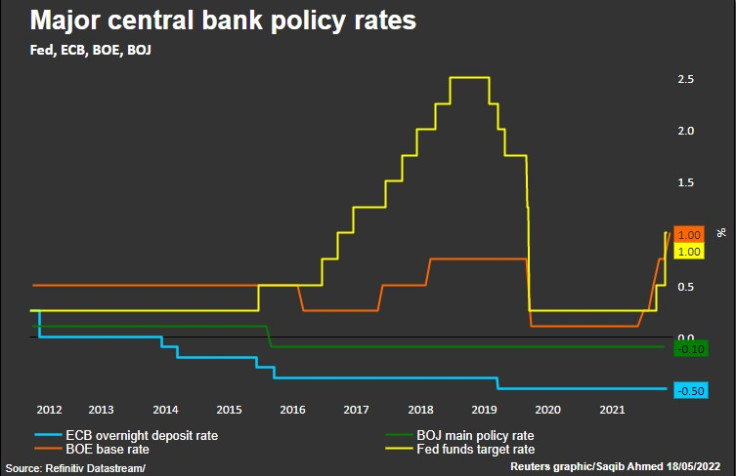

She repeated that line during a Wall Street Journal-hosted webcast this month, adding that rising U.S. interest rates relative to those in the rest of the world have helped fuel the dollar's rise.

"In a way, that is part of how a tighter monetary policy works," she said, indicating that she was comfortable with the dollar's appreciation up to then.

(GRAPHIC- Major central bank policy rates:

)

TWO-WAY RISK

If it's a simple as that, then Yellen and her fellow G7 finance chiefs may just assume that a reversal in these interest rate gaps will cool the dollar's jets eventually.

But some may be tempted to issue a verbal shot across the bows of any potential dollar overshoot that could unnerve global markets further.

Analysts at Barclays and Goldman Sachs reckon the dollar is close to topping out - Goldman estimates the dollar is 18% overvalued - but they are cautious of calling for a reversal.

The ECB's window to raise rates before recession hits may be smaller than the Federal Reserve's and the Bank of Japan is still committed to an ultra-loose monetary policy aimed at capping the 10-year yield at 0.25%.

Steven Englander, head of FX strategy at Standard Chartered and a veteran G7 watcher, notes that Japan's monetary policy is entirely consistent with a weak yen, which reduces the chances of a Tokyo protest against dollar strength making it into the Bonn communique.

"Any mention would be an effort at making investors more cautious on one-way dollar-buying. Any intervention mention is a shot across the bow but they are not close to taking a real shot at intervention yet," Englander said.

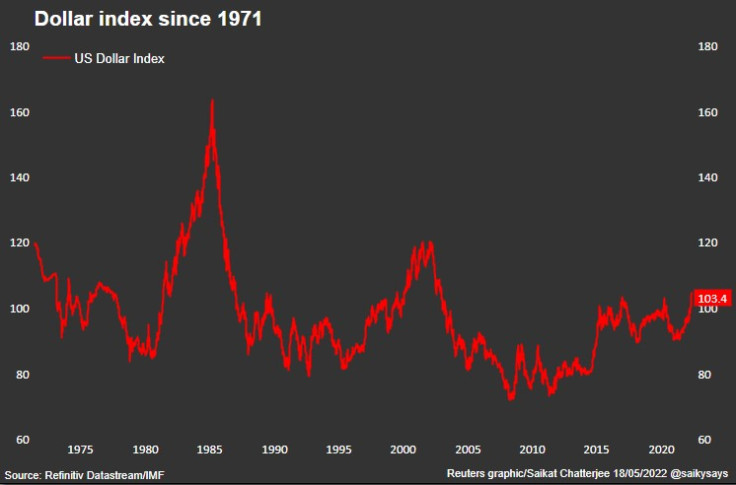

The last time the world's leading industrialized economies took coordinated action to address independent dollar strength was the G5's Plaza Accord in 1985.

(GRAPHIC- Dollar index since 1971:

)

The current mix of high U.S. inflation, a hawkish Fed, and divergent policy among the world's top central banks has drawn parallels with the early 1980s and the run-up to Plaza - even if most see any repeat as unlikely.

But the G7 host sets the meeting's agenda, and if French officials are already making noises about the euro, you can be sure Germany is way more nervous about the weak exchange rate and inflationary pressures that come with it.

Joe Lavorgna, chief economist, Americas at Natixis and former adviser to President Trump, doubts Yellen will want to address the issue if she can help it, but doesn't rule it out in the near future.

"The administration won't want a weaker dollar, certainly not at this point. A weaker dollar eases financial conditions, and the U.S. wants tighter conditions. But if you get an overshoot of the dollar through the summer and stagflation in the euro zone, the calculus could shift," he said.

Related columns:

TINA' still driving hedge funds' bullish dollar view

Stirring ingredients of 1985's dollar-capping Plaza Accord

Fed fingers crossed for 1994 re-run as hiking path shortens

Fraying central bank consensus spurs dollar and market stress

(The opinions expressed here are those of the author, a columnist for Reuters.)

(By Jamie McGeever; Editing by Tomasz Janowski; Graphics by Saikat Chatterjee, Joice Alves, Saqib Ahmed)

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets