Mass Shootings Create Demand For ‘Active Shooter Insurance’

In the days after Oct. 1, when a gunman at the Las Vegas Mandalay Bay Resort and Casino opened fire on a crowd of concert-goers, killing 58 people and wounding hundreds more, the share price of MGM Resorts International, which owns the Mandalay, tanked. The company has assisted victims’ families with their travel needs and canceled shows at its Vegas venues, and it’s already facing at least one lawsuit. Legal experts say there are surely more to come. Put simply, the attack, while horrifying at its core, is costing MGM a lot of money.

In the past few years, as the frequency of mass shootings has ticked upward, a market for insurance that covers the commercial fallout in the wake of such tragedies — such as lawsuits, funerals, public relations cleanup and loss of business — has materialized in North America and Western Europe, but predominantly in the U.S. And, though little data or research exists on what is still a relatively new insurance product, it can be a very lucrative venture, experts told International Business Times.

The damage potential associated with mass shootings — stemming from not only casualties and structural harm, but decreased business due to brand stigma — is enormous. Add to that the tendency for media coverage of the events to lend the appearance of a spike in prevalence, and the result is a heightened demand for active shooter insurance from companies big and small, said insurance agents who spoke with IBT. Each new tragic event brings a fresh surge of demand. But the rare and terrifying nature of shooting events can create a disconnect between how necessary these insurance policies appear and how useful they actually are, leaving insurers with wide profit margins and virtually no claims to pay, experts told IBT.

“Any one single incident is a tragedy. But compare that to the number of possibilities, the millions of events that could occur,” University of Connecticut School of Law professor Peter Kochenburger said, pointing to the numerous concerts, sports games and other public events that take place across the country each day. But what matters to policyholders is not so much frequency as fear: “If you could sell shark bite insurance, you could probably make a lot of money.”

And because victims and their families can always sue for negligence, alleging that more could’ve been done, insurers have an incentive to focus predominantly on the response to a tragedy rather than what can seem like a futile prevention effort. As Paul Marshall, the managing director of the underwriter McGowan Program Administrators, which offers active shooter insurance, put it to IBT, “You can’t prevent crazy.”

Terrorism Insurance: Active Shooter’s Not-So-Distant Cousin

It’s unclear whether MGM Resorts has insurance to cover mass violence that hasn’t been designated a terrorist act by the federal government; an MGM spokesperson did not answer questions from IBT on the subject of the company’s coverage. But, according to its most recent annual financial statement, MGM, unlike some of its main competitors, has “‘all risk’ property insurance coverage for our operating properties, which covers damage caused by a casualty loss (such as fire, natural disasters, acts of war, or terrorism).”

That’s likely thanks in part to a federal program created in the wake of the Sept. 11, 2001 attacks, when sellers of terrorism insurance either pulled out of the market, fearing they could face the same market-destabilizing $40 billion in costs (in 2001 dollars) that followed 9/11, or raised their coverage costs to levels unaffordable for most corporations. The program, called the Terrorism Risk Insurance Act, or TRIA, originally enacted as a temporary measure in 2002, mandated that all property and casualty insurers offer terrorism coverage, and provided them with federal reinsurance for attack-related commercial losses of up to $100 billion. (After Congress reauthorized it in 2015, it became the Terrorism Risk Insurance Program Reauthorization Act, or TRIPA.) This model, according to a Congressional Budget Office report on TRIA from 2015, “left taxpayers bearing most of the catastrophic risk.”

When Congress skirted reauthorization of TRIA at the end of 2014, before ultimately renewing it the following January, some worried that Super Bowl XLIX would be canceled without the government’s terror-insurance safety net. In 2013, after all, the Boston Marathon bombings, which were not classified as terrorism, sparked interest in such insurance coverage.

Still, despite the wave of anxiety that follows instances of mass violence in the U.S., the CBO noted that, as of January 2015, the federal government had paid no TRIA claims. Because later terror attacks in San Bernardino, California, and Orlando, Florida, in 2015 and 2016, respectively, likely did not meet the Treasury’s $5 million damages threshold to trigger TRIA, it’s unlikely that the government has paid any claims since. (The Treasury Department did not respond to IBT’s questions about TRIA claims.) Meanwhile, the program has cost the government less than $1 million annually in administrative costs and netted the insurance industry $4.6 billion per year in commercial premiums for federally-insured, practically risk-free coverage, experts at the libertarian Rand Institute calculated in 2014. Those figures have led some to argue that TRIA is no more than a subsidy for insurers and should be outright abolished.

The Las Vegas attack has not been characterized as a terrorist act, drawing criticism from some terrorism experts and skeptics who say the color of the assailant’s skin may have been the deciding factor. Without the designation, MGM — or rather, its insurers — won’t qualify for help from the federal government through TRIA.

4. No proof is provided, but ISIS has rarely claimed attacks that were not by either their members or sympathizers.

— Rukmini Callimachi (@rcallimachi) October 5, 2017

4. No proof is provided, but ISIS has rarely claimed attacks that were not by either their members or sympathizers.

— Rukmini Callimachi (@rcallimachi) October 5, 2017

6. In their chatrooms, they are claiming that the West and the media is leading a cover-up in order to hide the "martyrdom" of their brother

— Rukmini Callimachi (@rcallimachi) October 5, 2017

Enter active shooter insurance.

‘Plenty Of Incentive To Create A Fear’

Between 2000 and 2006, there was an average of 6.4 mass shootings each year in the U.S., according to a study by the Federal Bureau of Investigation. Between 2007 and 2013, that number jumped to 16.4. In 2014 and 2015, that average rose once more, to 20 incidents annually, the FBI found in a later study, which noted that a full 70 percent of those events took place in “a commerce/business or educational environment.” But in contrast to the market’s response to 9/11, the supply of insurance policies for these events has been on the rise over the past several years, as the trade publication Insurance Journal has reported.

The increase in availability is a response to an upswing in demand, underwriters and insurance agents told IBT. According to John Eltham, who heads North America business for Miller Insurance Services LLP, a Lloyd’s of London broker, the rise in policies sought by businesses has led the coverage to broaden beyond gun violence to all manner of attacks, including those with knives and bombs, under the new category of “active assailant.”

Many of the insurers leading the way in the active shooter market did the same within the market for terrorism insurance — namely, American International Group Inc., or AIG, and Lloyd’s of London, which counts Miller as a broker, London-based specialist insurer Beazley Group as a syndicate and Atlanta-based Southern Insurance Underwriters Inc. as a binding authority coverholder.

Though AIG did not comment for this article, it certainly has been an early pioneer in the market for active shooter insurance policies. The company helped crisis management consultancy Marsh Risk Management Research develop two guidebooks on “addressing the risk of an active shooter” in the summer of 2014, hosted a webcast on “active shooter” for the industry publication Business Insurance in March 2013 and, around the same time, produced a brochure specifically identifying Las Vegas venues as high-risk clientele when it comes to violent incidents. At the bottom of its Hospitality and Leisure policy page, AIG offers a variety of advisory pamphlets on handling an active shooter event, courtesy of the New York Police Department, Department of Homeland Security and others.

#insurance AIG Active Shooter Webcast http://t.co/TA9vNPLQpa

— Christine Brown (@Brownsinsurance) March 22, 2013

In terms of demand, Paul Marshall, the McGowan Program Administrators managing director, said he used to receive one inquiry per month about active shooter insurance; now he receives 10 to 40 each week. His clients, he said, include a pride parade, a national political party convention organizer and a concert organizer. Kerri O’Dwyer, a political violence underwriter at Beazley, whose team focuses on everything from civil war and a “coup d’etat” to “riots, strikes” and “malicious damage,” said her unit was at first “ binding a handful of risks per month, and now we’re binding, what? Fifteen to 20 per month.” She added that Beazley has been quoting as many as 10 policies daily, compared to one per day at the outset, in 2016. Southern Insurance Underwriters Senior Vice President Hugh Nelson said that while demand for his firm’s policies has been flat, he’s “seen big companies give lip service to getting it.”

As Nelson told the Insurance Journal in March, demand tends to rise after a deadly shooting incident, and his company has, in the past year, expanded both beyond educational institutions and firearms to cover a range of venues and weapons. Eltham, of Miller, said he’d already noticed an increase in demand immediately after the events in Las Vegas. The president and co-founder of McKinney, Texas-based GDP Advisors LLC, which also administers active shooter coverage and did not respond to interview requests from IBT, told the Journal in August 2016, “Sadly, active shooter incidents are the next cyber.”

But both the insurance industry — and the media, for what it’s worth — may be inflating the appearance of risk, said Kochenburger, the University of Connecticut professor.

“Cyber risk is everywhere, same thing as employee lawsuits against employers,” he told IBT, adding that the apparent dangers of an active shooter incident are often “greatly exaggerated.”

“To compare these risks against active shooter risks — well, to say it’s inaccurate is an understatement.”

Smaller mom-and-pop companies without the resources to analyze their own probability of facing an attack, Kochenburger said, could end up overpaying for what they believe to be a very real and imminent danger.

“One way you can make a lot of money in insurance is if the policyholders really overestimate the risk. Then you could have a very profitable insurance company,” he said. Mass shootings and other random violence is “not a silly concern. However unlikely it is that the event will occur, there’s been an increase… The question is how necessary or important [insurance coverage] is.”

George Mocsary, an assistant professor at the Southern Illinois University School of Law, echoed Kochenburger’s argument that mass shootings are far rarer than they might appear from news coverage, and that it pays to play on those worries.

“There’s plenty of incentive to create a fear to get active shooter insurance,” Mocsary said. For example, if a customer at a tech store is purchasing a TV, he said, “the salesman scares you about how your TV can break.”

It’s clear that active shooter insurers and underwriters, or at least their marketing teams, are aware of such tactics.

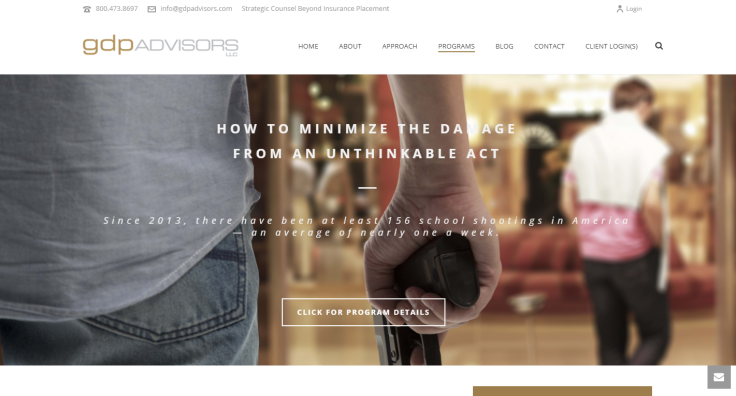

GDP Advisors’ Active Shooter Insurance Program webpage, for instance, features a harrowing graphic of an individual entering what appears to be a restaurant or hotel lobby, a handgun at their side. The text overlay reads, “How to minimize the damage from an unthinkable act” and, “Since 2013, there have been at least 156 school shootings in America — an average of nearly one a week.” GDP Advisors launched its active shooter coverage in July 2016.

McGowan Program Administrators, in a brochure on its own active shooter program, obtained by IBT, said “the numbers as of November 10, 2016 are a bit staggering,” and that, “unfortunately, by the time you begin and end this article the numbers are likely to be outdated just as quickly.”

“Despite security measures, by design and necessity these places remain very open places. The reality of the needs of these buildings directly oppose much of what the security measures look to achieve,” the pamphlet, which included graphics of bullet-pocked glass and frightening newsprint headlines, continues. “Organizations have been successfully sued for negligent security.”

Marshall defended the use of chilling ads as a tool for raising awareness.

“Mass shootings and recent public attacks make security upgrades and purchasing adequate insurance a priority (and should be legally required like auto insurance),” he wrote in an email, citing an internet article on “powerful social issue ads that’ll make you stop and think.”

‘My Prediction Is It’s Virtually All Profits Right Now’

According to O’Dwyer, the popularity of this new insurance coverage skews American. Beazley, she said, offers this coverage in the U.S., Canada and Western Europe, but three quarters of demand for its active shooter insurance comes from the U.S., compared to 20 percent for Canada and 5 percent for Western Europe.

“It’s more to do with [the fact that] that’s where we offered our education programs,” she said. Beazley pushed its education program hardest in the U.S., she added, since the frequency of major non-terrorist shootings is higher.

American gun politics aside, the frequency is still so low that active shooter insurance policies come with fat profit margins, according to experts.

“At this point, my prediction is it’s virtually all profits right now, because the events are so sporadic that they’re just not hitting the insured population yet,” said Adam Scales, a Rutgers University law professor who specializes in insurance. “You’re not talking, probably, about significant exposure by the insurance agency.”

Because the cost of adequately covering an active shooter incident — for instance, with a $5 million policy — is cost-prohibitive for most businesses, Scales added, companies will resort to purchasing cheaper policies in the $250,000 range that won’t give them much of a cushion, and won’t hurt the insurer, if a claim is paid.

“I would wonder why you would even buy it,” he said, adding that such coverage is “not economically valuable” to the policyholders.

For insurers and underwriters, though, there is economic value, Kochenburger noted.

“It is a for-profit market,” he said. “If they’re not making a profit, they’re not going to cover it.”

Marshall defended the industry’s corporate ethics.

“We feel we’ve been responsible… If we collected $10 million in premiums, we’re going to assume that we’re going to be paying out a large portion of that in claims,” he said. “Time will tell. We want to insure responsibly. We’ve not had a claim, but we’re insuring risks similar to ones that have had claims.”

Negligence: ‘You Can Always Allege It’

One of the benefits of insurance coverage is the monetary incentive to minimize risks as much as possible, because doing do minimizes the cost of insurance. Kochenburger compared the active shooter preparation and prevention effort to buying smoke detectors or storm shutters when getting a quote for home insurance. Mocsary suggested the purchase of metal detectors might bring down a company’s premiums by way of lowering its active shooter risks.

But attempts at prevention can only go so far.

“To the extent that you can reduce the [likelihood of the] acts of someone who’d do this — they can’t address the psychological issues, gun control — they can’t do anything about that,” Kochenburger said.

Marshall said something similar.

“Some of the prevention experts may not like me, because this event at the Mandalay — there’s no way you could’ve prevented this. You can’t prevent crazy,” he said. Marshall’s ratio of focus on post-event remediation versus prevention and preparation is 80 percent versus 20 percent, he told IBT. “You have to understand that you really won’t be able to stop this event… I think it may be leading to a false sense of security. Kind of like a tornado, or your house getting burned down.”

Both O’Dwyer and Nelson said the divide was closer to 50-50.

To Mocsary, buying an active shooter policy simply meant “buying legal representation,” because of the lawsuits sure to come in the weeks after an instance of violence inside a theater, stadium, hotel or other business. O’Dwyer emphasized the importance of the public relations response that comes with Beazley’s policy.

“What you say in that first few minutes and hours, that will stay with you forever,” she said.

Nelson, of Southern Insurance Underwriters, pointed to the constant threat of negligence lawsuits, no matter how much companies prepare.

“You always allege it,” he said.

On the other hand, Scales, the Rutgers professor, said that standard commercial general liability insurance policies, akin to MGM’s “all risk” policy, cover litigation already, rendering the extra layer provided by active shooter insurance pointless.

In Vegas, one victim is testing that assertion with a lawsuit alleging that MGM failed to notice the massive stockpile of weapons the assailant had lugged up to his 32nd-floor suite.

“How did the hotel not know about that? Why wasn’t that a red flag?” Michelle Tuegel, an attorney for the victim, told the Las Vegas Review-Journal. The lawsuit, depending on its outcome, could inform standards of corporate liability following a mass shooting and define the need for active shooter insurance in the future. As Tuegel put it, the legal action was aimed at companies “who have a responsibility to keep the people who are on their properties at their events safe.”

Update (10/16/2017, 11:05 AM): This post has been updated to clarify the relationship between Lloyd's of London and several other insurance firms.

© Copyright IBTimes 2024. All rights reserved.

- MOST POPULAR IN Business