Week Ahead: FOMC Meeting And Minutes, Lehman Brothers’ 5-Year Anniversary, RBI Rate Decision

Happy anniversary, Lehman Brothers. Five years ago on Sept. 15, Lehman Brothers filed for protection under Chapter 11 of the U.S. Bankruptcy Code during an almost-unprecedented financial and economic crisis. The turmoil was followed by an unprecedented monetary-policy response, which in turn has been followed by nearly unprecedented bull markets in bonds, stocks and now real estate.

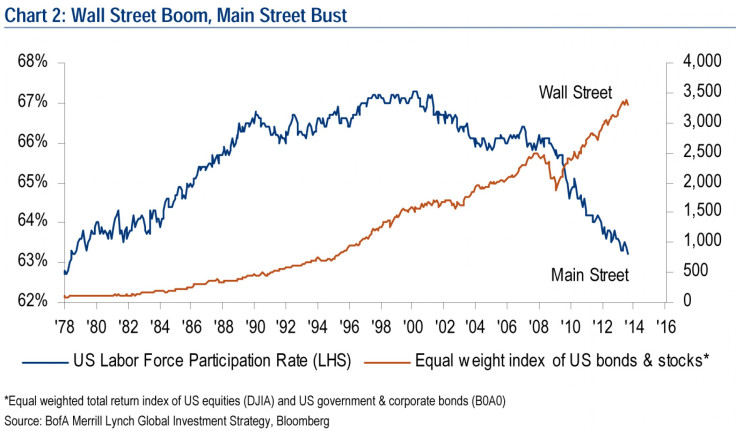

Wall Street has soared, but Main Street has soured.

“Significant monetary stimulus, the end of fiscal austerity, a booming housing market, a cheap dollar, record corporate cash balances ... if the U.S. economy does not significantly accelerate in coming quarters, it never will,” Michael Hartnett, Bank of America Merrill Lynch’s chief investment strategist, wrote in a report.

All eyes will be on the Federal Open Market Committee meeting this week as the market anticipates the Federal Reserve’s tapering decision. Both the FOMC policy statement and its up-to-date economic and market projections will be released on Wednesday at 2 p.m. EDT, followed by Fed Chairman Ben S. Bernanke’s press conference at 2:30 p.m.

The first thing market participants will be looking for is a decision on tapering. Nearly three-quarters of the 69 economists polled by Reuters after the mixed August jobs data anticipated the FOMC would announce a tapering of its quantitative-easing program following its Sept. 17-18 meeting. The consensus is the central bank will trim its monthly spending on QE asset purchases by $10 billion -- a smaller amount than previously expected.

How swiftly the Fed cuts its QE purchases at future meetings will depend a lot on the evolution of the labor market. The Fed announced its most recent round of QE in September of last year, and it has been buying $85 billion a month since January. Although the 169,000 U.S. jobs gained in August missed the forecast, the economy has added more than 180,000 jobs a month on average since the latest program was launched. That compares with an average of just 130,000 in the six months before the program was launched. During the same time, the unemployment rate has dropped to 7.3 percent from 8.1 percent ahead of last September’s FOMC meeting.

Among all the data to come out of this September’s FOMC meeting, the most interesting -- and market-moving -- may be what Fed officials pencil in for their 2016 forecasts. Projections that far ahead are subject to much uncertainty, but markets still will pay close attention. Bank of America Merrill Lynch economist Ethan Harris expects the FOMC to signal an ongoing recovery and a more gradual hiking cycle than markets currently anticipate.

At the postmeeting press conference, Bernanke is likely to clearly communicate the conditional nature of Fed policy toward the current QE program, and the distinct considerations for asset purchases versus interest rates.

“We expect Bernanke to discuss how the Fed intends to adjust its guideposts in light of the more-rapid-than-expected decline in the unemployment rate, even though most other labor-market indicators have shown much more limited improvement,” Harris said. “We also look for comments on how the Fed views risks from higher interest rates, the debt-ceiling debate, and Middle East geopolitical risks.”

A handful of Fed officials will be speaking publicly later in the week, offering markets a chance to gain more insight into what happened behind closed doors on Tuesday and Wednesday. The central bank won’t release the minutes of the September meeting until Oct. 9.

In Europe, the European Commission and German ZEW consumer-confidence surveys will point to a continued modest recovery. Meanwhile, the election in the German state of Bavaria this Sunday might provide some early clues to the outcome of the following week’s federal election. Elsewhere, both the Swiss National Bank and the Norges Bank will hold monetary-policy meetings on Thursday.

Markets will be closed on Monday for a public holiday in Japan. It will be a quiet week for economic data there, with the August trade figures on Thursday being the only noteworthy release.

In India, Friday’s monetary-policy meeting at the Reserve Bank of India will be the first to be chaired by the new central-bank governor, Raghuram Rajan. Much will hinge on how markets react to the U.S. Fed’s policy decision, according to Gareth Leather and Daniel Martin at Capital Economics. The rising likelihood of the Fed withdrawing stimulus has been one of the key factors in the collapse of the rupee over recent months -- it is down by 14.5 percent since late May, despite a recent rally.

“In our view, Fed tapering is now largely priced into the markets, and we are not expecting fireworks this week,” Leather and Martin said. “As long as the rupee does escape relatively unscathed, the RBI is likely to leave rates unchanged.” However, a fresh sell-off would raise the possibility of a rate hike.

Below are entries on the economic calendar Sept. 16-20. All listed times are EDT.

Monday

8:30 a.m. -- The September Empire State manufacturing index will likely show a print of 9.20, an increase from August’s 8.24.

9:15 a.m. -- Industrial production is expected to advance at a 0.4 percent month-on-month clip in August. This gain in output comes after a month when industrial production was unchanged. If the forecast is correct, the capacity-utilization rate will rise to 77.8 percent from 77.6 percent. Driving the solid gain in the headline series is a rise in manufacturing production by 0.2 percent, following a 0.1 percent decline in July.

Non-U.S.:

Euro zone -- European Central Bank Executive Board Member Yves Mersch will speak on market infrastructures in Dubai.

Portugal -- Officials of the so-called troika -- the European Central Bank, European Commission and International Monetary Fund -- are to begin a review of the Portuguese aid program.

Euro zone -- ECB President Mario Draghi will speak at an SME conference in Berlin.

Euro zone -- August final harmonized index of consumer prices, or HICP.

Tuesday

TBA -- First day of the two-day FOMC meeting.

8:30 a.m. -- Economists look for the consumer price index in August to edge 0.2 percent higher month-on-month, matching July’s gain. The core measure probably rose by 0.1 percent in August. Against year-ago levels, core CPI inflation should run 1.8 percent, below the Fed’s 2 percent target rate. Slack demand and muted wage growth all point to continued softness in inflation.

10 a.m. -- The National Association of Home Builders housing market index has improved sharply in recent months, printing 59 in August after printing 41 as recently as April. Given the risks posed by a slowdown in the pace of growth in starts and sales related to higher mortgage rates, however, economists look for an unchanged reading of 59 in September.

Non-U.S.:

Netherlands -- Budget day.

Australia -- Reserve Bank of Australia board minutes.

Euro zone -- ECB Executive Board Member Peter Praet will speak on global reform of financial regulation and architecture in London.

Turkey -- Benchmark repo rate, overnight lending rate and overnight borrowing rate.

Euro zone -- ECB Executive Board Member Peter Praet will speak on the path of financial stability in the monetary union in Brussels.

Euro zone -- ECB current account.

U.K. -- August CPI.

Euro zone -- July trade balance.

Germany -- September ZEW economic-expectations index.

Wednesday

7 a.m. -- The Mortgage Bankers Association’s, or MBA’s, Mortgage Index for the week ending Sept. 13.

8:30 a.m. -- Economists expect housing starts will rise 3.2 percent month-on-month in August to 925,000 units. Building permits probably slipped to 948,000 in August from 954,000 in July.

2 p.m. -- FOMC statement and forecasts released.

2:30 p.m. -- Fed Chairman Ben Bernanke holds media briefing live via website following a two-day FOMC meeting on interest-rate and QE policies.

Non-U.S.:

France -- Government presents pension reform.

Australia -- RBA Assistant Governor Edey will speak at a conference on financial services in Sydney.

Euro zone -- ECB Executive Board Member Benoit Coeure will speak on European financial-market infrastructures in Dubai.

U.K. -- Bank of England Monetary Policy Committee minutes, bank-rate vote and QE vote.

Japan -- August trade balance.

Thursday

8:30 a.m. -- Economists expect initial jobless claims to climb up to 330,000 for the week ending Sept. 14 from 292,000 in the prior week.

8:30 a.m. -- The already reported decline in the trade deficit to $117.8 billion in the second quarter, from $122.6 billion in the first, suggests that the overall current account deficit narrowed to $97.2 billion. This would amount to 2.3 percent of gross domestic product on an annualized basis, a modest narrowing relative to the 2.6 percent in the first quarter.

10 a.m. -- Existing-home sales are expected to fall 2.6 percent month-on-month to 5.25 million in August, still a solid level. Pending home sales fell slightly in June and July, and economists expect the higher mortgage rates since May to dampen the August data. Existing-home sales are counted at the time of closing, as opposed to new sales, which are counted when the contract is signed, accounting for the lagged response of existing-home sales data to changes in mortgage rates.

10 a.m. -- Economists look for an increase of 0.5 percent month-on-month in the Conference Board’s index of leading economic indicators in August.

10 a.m. -- After falling to 9.3 in August from 19.8 in July, economists look for a modest rebound in the Philadelphia Fed manufacturing index to 10.1 in September.

12:20 p.m. -- Federal Reserve Bank of Cleveland President Sandra Pianalto (a nonvoter on the FOMC this year) will speak on “Looking for Common Ground and New Solutions in Household and Consumer Finance” at her bank’s 2013 Policy Summit on Housing, Human Capital, and Inequality in Cleveland.

Non-U.S.:

South Africa -- Repo rate.

Egypt -- Deposit rate.

Australia -- RBA bulletin.

Switzerland -- Interest-rate announcement.

Norway -- Interest-rate announcement.

Greece -- Q2 unemployment rate.

Ireland -- Q2 preliminary GDP.

Friday

12:30 p.m. -- Federal Reserve Bank of Kansas City President Esther George (a voter on the FOMC this year) will speak on “The Federal Reserve and the Economy” before the Manhattan Institute for Policy Research Shadow Open Market Committee meeting in New York.

12:40 p.m. -- Federal Reserve Board Gov. Daniel Tarullo (a voter on the FOMC) will speak on “Macroprudential Regulation” at the Sullivan & Cromwell Conference on Challenges in Global Financial Services hosted by Yale Law School in New Haven and viewable via Livestream.

12:55 p.m. -- Federal Reserve Bank of St. Louis President James Bullard (a voter on the FOMC this year) will speak on the “U.S. Economy and Monetary Policy” before a New York Association for Business Economics luncheon in New York.

1:45 p.m. -- Federal Reserve Bank of Minneapolis President Narayana Kocherlakota (a nonvoter on the FOMC this year) gives as academic talk at the New York University Stern School of Business’ Conference on Extracting and Understanding the Risk Neutral Probability Density from Options Prices in New York.

Non-U.S.:

India -- RBI repo rate, reserve repo rate.

Argentina -- Q2 GDP.

Sources: Central banks, European Commission, Reuters, Market News, Capital Economics, Barclays, Bank of America Merrill Lynch.

© Copyright IBTimes 2026. All rights reserved.

- MOST POPULAR IN Business