China PBOC Injects Cash Into Banks To Ease Credit Squeeze Ahead Of Lunar New Year Holiday

Following three cash crunches that struck China’s market last year, the country’s central bank is now taking the unusual step to strengthen its communication on interbank liquidity management.

“Better management of market expectations will become ever more important, as China’s financial system is set to go through significant changes ahead,” said Societe Generale's Wei Yao in a note.

With Chinese New Year holiday approaching, liquidity tensions are on the rise again. In response, the People’s Bank of China (PBoC) pumped 255 billion yuan ($42 billion) into the money market Tuesday.

While there’s nothing out of the ordinary about the injection, “what is unusual, and encouraging, this time is the use of communication,” Yao said.

On Sina Weibo (China’s Twitter), the PBoC disclosed Monday that it provided cash via the so-called standing lending facility, or SLF, a tool it launched a year ago to discreetly provide funds.

The PBoC said the moves are intended to maintain the stability of China's money market ahead of the weeklong Spring Festival that kicks off Jan. 31. The central bank also informed the market of the reverse repo operations before they took place.

Moreover, shortly after its Weibo posting, the central bank released a more elaborate statement (in Chinese) on its official website, saying that it has launched a pilot SLF on Monday to meet liquidity demand for four types of financial institutions (including city commercial banks, rural commercial banks, rural cooperative banks and rural credit unions) in 10 provinces and cities (including Beijing, Jiangsu, Shandong, Guangdong, Hebei, Shanxi, Zhejiang, Jilin, Henan and Shenzhen).

“We think these are significant steps by the PBoC,” Zhang Zhiwei, chief China economist at Nomura, said in a note. “These announcements suggest that the central bank is very concerned about potential liquidity risk in the interbank market leading into the Lunar New Year holiday period, as well as the financial risks in small banks.”

Money-market rates typically spike before the Lunar New Year break as Chinese parents withdraw cash from the bank to fill the red-envelopes they give out to their children as a symbol of good luck.

The recent news of a potential 3 billion-yuan trust default and the fact that the Shanghai stock market index dropped below 2000 on Monday suggest market confidence is weak, which may also have put pressure on the government to take action and restore confidence, Zhang said.

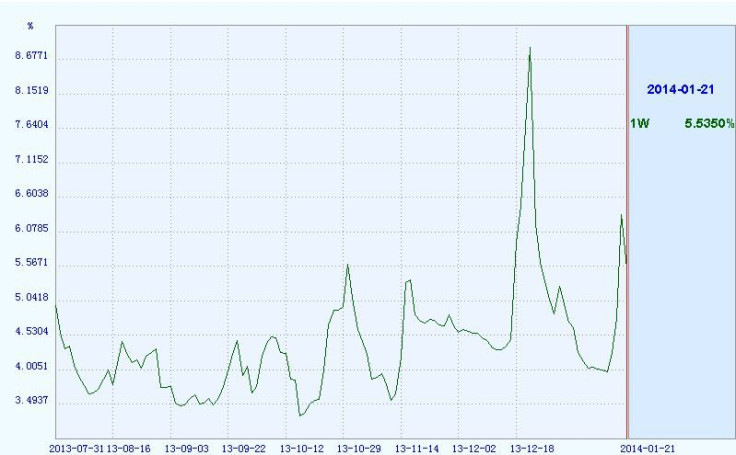

The seven-day repurchase rate, a gauge of interbank funding availability, averaged 4.09 percent last year, up from 3.50 percent the previous year. It ended at 5.54 percent Tuesday in Shanghai, according to a daily fixing compiled by the National Interbank Funding Center.

Nomura’s Zhang believes the PBoC’s latest moves do not suggest China is loosening its monetary policy stance because the current gross domestic product growth rate (7.7 percent in the fourth quarter) is still acceptable to the government.

“We think the government will continue to contain credit growth in the first quarter and tighten regulations on shadow banking after the Lunar New Year, and defaults in the corporate and shadow banking sector are likely to rise,” Zhang said.

“We continue to expect growth to drop to 7.5 percent by the first quarter and 7.1 percent by the second quarter, and the monetary policy stance to be eased in mid-2014,” Zhang added.

Societe Generale's Yao thinks the central government has the resources and control to avoid a disastrous outcome, at least at this juncture, but the tricky part is managing market expectations. “Hence, the PBoC’s effort to strengthen communication is of particular importance,” Yao said.

© Copyright IBTimes 2025. All rights reserved.

- MOST POPULAR IN Business