Factbox-From Property To Bonds, Four Financial Flashpoints For The Euro Zone

While a financial storm gathers nearby, the euro zone has so far been comparatively unscathed.

The club of 19 countries that share the euro has not seen a flare-up in financial stress even as UK pension funds gasp for air and Swiss banking giant Credit Suisse comes under market pressure.

But surging interest rates and a drying up of capital means it is probably a matter of time before some trouble emerges in a bloc that has relied for a decade on ultra-low borrowing costs.

Here's a look at four possible flashpoints that are keeping investors and regulators awake at night: property prices, bank loans, government bonds and "shadow banks".

REAL TROUBLE

The euro zone enjoyed a real-estate boom until last year, with home prices rising by some 40% since 2015 and commercial real estate prices up 26%.

But the picture is changing fast as mortgage rates have doubled from record-low levels in response to the European Central Bank's moves to curb inflation.

That could cause trouble in countries such as Spain and Portugal, where most home loans are at a variable rate.

"Banks will have to increase their provisions to cover potential losses," Spain's central bank governor Pablo Hernandez De Cos has said.

ECB staff estimate that when rates have been ultra-low, a 1 percentage point increase in the mortgage rate - like the one we've seen since the start of the year - leads to a 9%-15% decline in home prices after about two years.

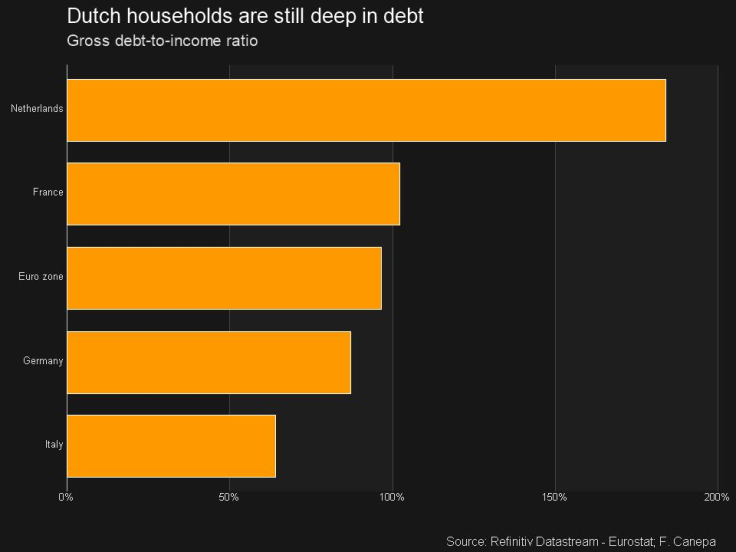

Prices have already started falling in large German cities and have been stagnating in the Netherlands - the European country that Oxford Economics sees at greatest risk due to its high household debt and expensive properties.

The Dutch are still in a lot of debt

SPREAD TOO THIN

The rise in interest rates has raised fresh questions about one of the world's most indebted borrowers: Italy.

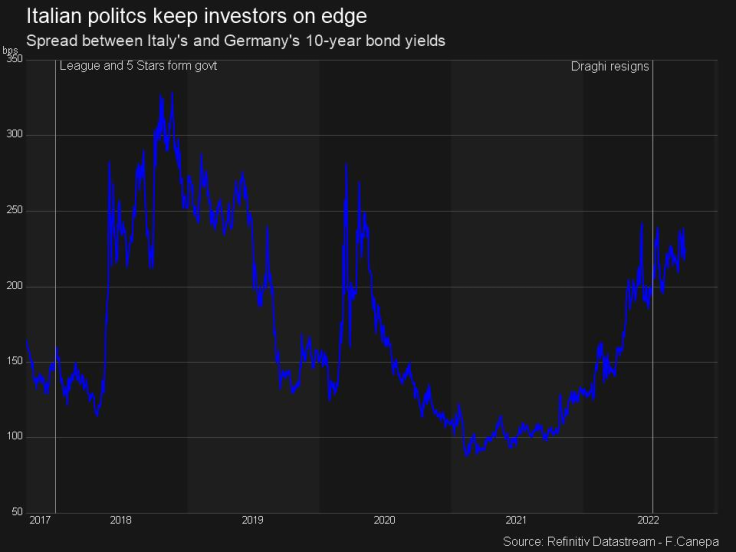

Investors and central bankers are watching every tick in the spread between Italian and German borrowing costs for signs that the market is losing faith in Rome's ability to roll over its debt, which now stands at 134.8% of its economic output.

Italians have voted in a right-wing coalition with a eurosceptic past, which will now have the hard task of keeping public finances in order while fulfilling at least some of its election pledges for tax cuts, more social spending and higher pension benefits.

Economists at Morgan Stanley estimate that these measures would increase the deficit by roughly 2 to 4 percentage points of GDP.

"Such policies will prove difficult during a time of rising interest rates and heightened market scrutiny about debt dynamics," Seth Carpenter, global chief economist for Morgan Stanley, said.

The ECB has put up firewall against a widening of bond spreads.

It has been using proceeds from its pandemic-era, bond-buying programme to buy more debt from Italy and other southern European countries and it still has an entirely new scheme in its arsenal.

But policymakers have told Reuters they did not see a need to activate it yet, despite the German-Italian spread hitting 250 basis points several times in recent weeks - a level that triggered a reaction last summer.

Italian bonds under pressure since Draghi left

ADDING FUEL TO FIRE

ECB bank supervisors have been telling banks to cut down on leverage finance - extending credit to already indebted borrowers - but feel their words have been ignored.

The exposure to leveraged finance - including high-yield bonds and collateralised loan obligations - stood near a record 600 billion euros at the end of June, or 6% of banks' capital, according to ECB calculations.

"Importantly, a large share of these exposures is to highly leveraged corporates, which are the riskiest segment of an already high-risk asset class," the ECB's top supervisor Andrea Enria said.

Fellow ECB supervisor Elizabeth McCaul warned of "significant deficiencies" in how banks evaluate and manage risks associated with this type of credit.

LURKING IN THE SHADOW

European regulators have warned about "shadow banks" for so long that they have tired of that phrase, which indicates financial institutions that engage in some form of lending but aren't banks, and started calling them "non-bank financial intermediaries".

Stress has emerged in companies that trade energy derivatives as a result of the sharp rise and successive gyrations in the price of oil and gas that followed Russia's invasion of Ukraine.

The ECB has batted back calls to throw a lifeline to these firms, leaving it to governments instead, and spoke out against relaxing capital requirements at clearing houses, where trades are settled.

Instead, central bankers gathered at the European Systemic Risk Board, the European Union's financial watchdog, said fund managers should use "liquidity management tools" - a likely reference to making it more difficult or costly for clients to get their money back at times of stress.

Even insurers, normally seen as one of the safest corners of the market, were told to watch out for households missing their payments.

"Stretched household balance sheets heighten the risk of insurance contract lapses, potentially widening the protection gap but also making liquidity monitoring relevant," the ESRB said in a warning.

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Business