Fed, And Powell, Face A New World Of Risk In Pivot To Tighter Policy

The U.S. Federal Reserve's plan to end the loose money policies used to fight the pandemic is facing an unexpectedly early test as the Russian invasion of Ukraine poses new economic and financial risks already being felt in global markets.

Fed Chair Jerome Powell testifies before Congress on Wednesday and Thursday, and his first comments on the economy in nearly five weeks will confront a situation that has become markedly more complex since January, when he outlined a straight-forward central bank effort to address high U.S. inflation.

The remedy - steadily rising interest rates, an eventual reduction in the Fed's bondholdings, and "nimble" attention to new data - may remain largely intact. Inflation since Powell last spoke has accelerated, a Fed report last week suggested it may prove more persistent, and the conflict in Europe could put even more pressure on prices.

But there may be a new note of caution in Powell's approach, and markets are now arguably making the Fed's job harder.

Fed officials in recent weeks spoke approvingly of the fact that Treasury rates had been rising on the expectation of Fed rate hikes, and viewed that financial "tightening" as helpful in countering inflation.

Since the start of the war in Ukraine market prices have moved the other way - the yield on the two-year Treasury hit as high as 1.62% on Feb. 25 but traded as low as 1.27% on Tuesday - and investors have all but priced out the possibility of a larger, half-point rate hike when the Fed meets March 15-16.

Russia's increasing isolation, meanwhile, with its central bank assets frozen and other sanctions starting to bite, has driven global risk aversion higher and pushed up the cost of dollar funding in European credit markets.

The jump was smaller than seen at the start of the coronavirus pandemic, when trading became difficult even in usually free-flowing markets like that for U.S. Treasury bonds, and prompted the Fed to intervene with massive bond purchases of its own to keep the financial system functioning.

Yet it is a reminder that efforts to punish the Russian government will exact a cost, potentially in the form of slower global economic growth and increased financial stress, that Fed officials may want to assess before moving too aggressively. Allowing its own bondholdings to shrink at a time of higher global financial risk, for example, is counter to the Fed's own adopted role as the world's financial backstop of last resort.

"So far all of the repricing in risk and dollar funding markets has been orderly," said Columbia Threadneedle senior analyst Ed Al-Hussainy. But the new uncertainty may "test" Fed facilities set up during the coronavirus crisis to help keep financial markets running smoothly, he said, and possibly force the Fed to at least temporarily boost purchases of short-term U.S. Treasury securities because of increased world demand for dollars.

"I think Powell sits down in front of Congress this week and says, one, we are 100% focused on reacting to inflation. Two, we will support market liquidity if necessary...Three, we will work hand in hand with Treasury to impose sanctions on Russia and make sure that the U.S. financial system has the capital and liquidity buffers to handle spillover risks," he said.

FOCUS STILL ON INFLATION

Powell will testify Wednesday at 10 a.m. ET (1500 GMT) before the House Financial Services Committee and at the same time on Thursday before the Senate Banking Committee, one of the Fed chair's twice yearly congressional appearances coinciding with publication of a semiannual Fed review of monetary policy.

The policy report was released last week, just two days after Russian forces invaded Ukraine, and included just one terse mention that "recent geopolitical tensions related to the Russia-Ukraine situation are a source of uncertainty in global financial and commodity markets."The focus of the report was on U.S. inflation, now running at triple the Fed's 2% target and, according to the document, at risk of remaining higher than desired unless more people start filling the record number of open jobs, and supply chains work through a pandemic backlog.

Powell is likely to keep much of his focus on inflation and the need for the Fed to begin raising interest rates.

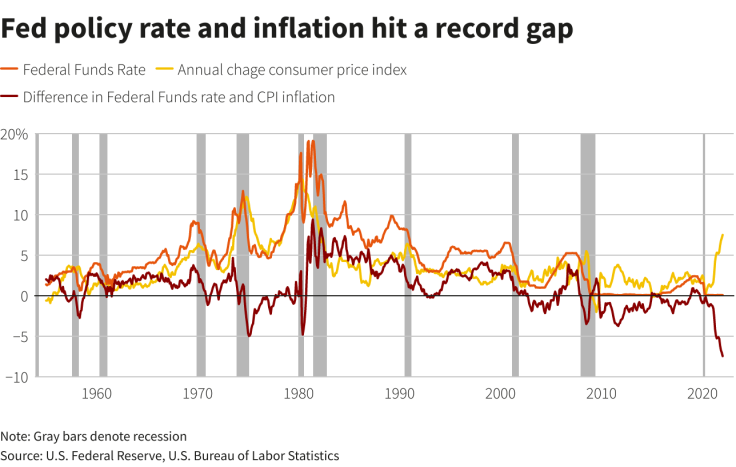

A related graphic: Fed policy rate and inflation hit a record gap:

The current emergency setting, effectively zero, is out of sync with the U.S. economy's comparatively fast exit from the pandemic-induced recession of 2020. The gap between consumer inflation and the Fed's policy interest rate is the widest on record as the central bank continues to stoke an economy enjoying fast growth, rising wages, strong consumer spending, and record demand for workers.

But recent events may temper how fast the Fed tries to fill that gap.

Analysts say Powell may downplay the possibility the Fed approves a half-percentage point increase to kick off this round of rate hikes at its upcoming meeting, in effect resolving an ongoing argument among his colleagues that sparked its own bout of volatility and showed some space between Fed officials.

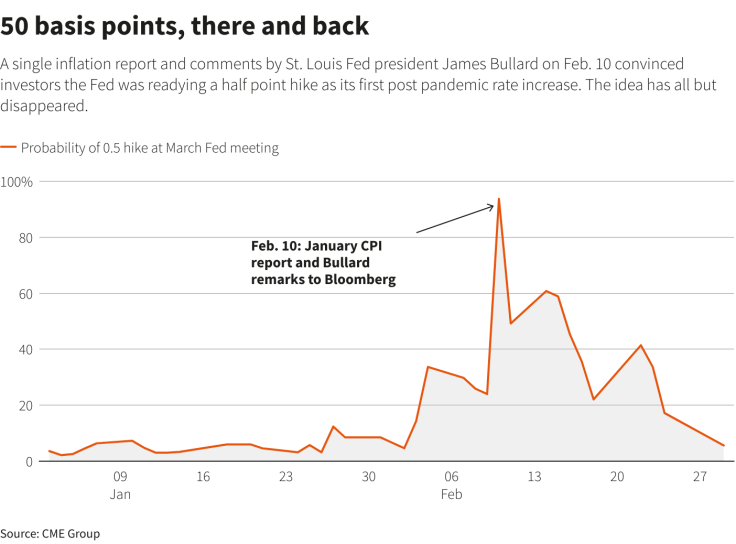

Traders in markets linked to the Fed's policy interest rate, spurred by high inflation and earlier comments from St. Louis Fed President James Bullard, were convinced as of Feb. 10 that the Fed would approve a 50 basis point increase in the Federal Funds rate at this month's meeting.

A related graphic: 50 basis points, there and back:

Other officials pushed back, and events since then have diminished the market's perceived probability of that larger increase to only around 5%.

"We now know what we are dealing with: a protracted stand-off between Russia and the West. We also think it has reduced the risk of central banks slamming the brakes to contain inflation," wrote analyst with the BlackRock Investment Institute. Interest rates "are headed higher. Yet central banks may face less political pressure to contain inflation as the conflict becomes an easy culprit for higher prices. We believe this will allow them to move more cautiously."

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Economy & Markets