How Much Will I Get From Social Security If I Make $100,000?

It's kind of important to know how much income you can expect to collect from Social Security -- or at least to have a rough idea of it. After all, it probably won't be sufficient to support you comfortably on its own, so you'll need to know how much more income you'll have to set up for yourself with savings, investments, and so on.

Here's a look at how much you'll get from Social Security if you earn $100,000 annually. Why $100,000? Well, while an income for typical American households was recently around $50,000, plenty of households average closer to $100,000. As of 2017, for example, the median income for a household headed by someone with at least a bachelor's degree was $98,038 -- and that includes plenty of households featuring just one person.

So here's how much folks making $100,000 annually might get from Social Security, along with how to find out what you can expect to reap from the program.

The shortcut -- for any income

Before focusing on those earning $100,000, he's how you can find out what you can expect to receive in retirement, no matter whether you earn $35,000 annually or $275,000: Go to the Social Security Administration (SSA) website and set up a "my Social Security" account. Doing so will let you see, at any time, the latest estimate of your eventual benefits, based on the SSA's record of your earnings. You can also examine that record, to make sure it's accurate -- because if it isn't, you may end up receiving less in benefits than you should. (Setting up an account is also a good idea because it can prevent identity theft and headaches, if you set up your account before a scammer does so for you, pretending to be you.)

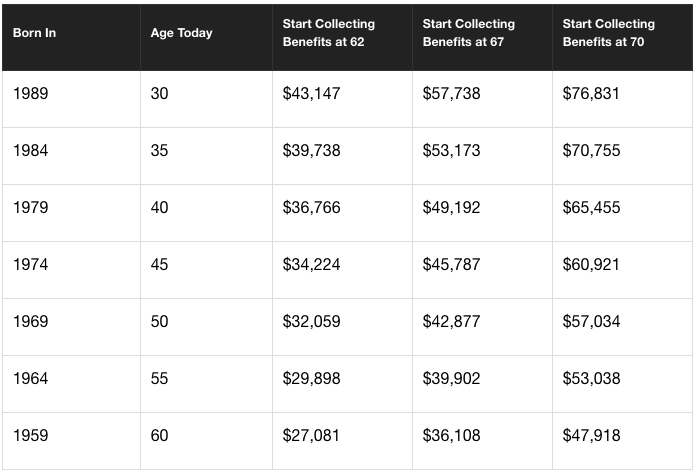

Social Security benefits for those earning $100,000

It's hard to offer any kind of definitive sum here, even with the precise income of $100,000, because your ultimate benefits will still depend on several factors, such as your age and when you start collecting your benefits, not to mention your history of earnings. (After all, you may be earning $100,000 annually now, but you might earn or have earned much more or less in other years.) Here's a rough idea, though, courtesy of an online calculator at smartasset.com:

Note that these sums reflect adjustments for inflation over the years.

Beef up your Social Security benefits

Whether you like the numbers above or you don't, know that there are ways to increase your Social Security benefits. For example:

- Work at least 35 years: The formula used to determine benefits is based on the 35 years in which you earned the most, with each year's income adjusted for inflation. So if you retire after working for only 30 years, there will be five zeros incorporated into the calculation, resulting in lower benefits than you'd otherwise get.

- Work for more than 35 years: If you're earning a lot more these days than you ever used to on an inflation-adjusted basis, then your 36th year of income will kick out your lowest-earning year, resulting in greater benefits.

- Delay starting to collect your benefits: You can start collecting as early as age 62 and as late as age 70, with your checks getting bigger for every year you delay. Most people start at age 62, which does make sense, because the system is designed to pay you the same benefits, in total, no matter when you start, if you live an average-age life. (After all, starting early will give you smaller benefit checks, but many more of them.) If you stand a good chance of living an extra-long life, though, and you can get by without claiming Social Security until age 70 or close to it, you'll get more total income out of the program.

The more you know about Social Security, the better decisions you can make related to it. And whatever your income, it's smart to know what to expect from retirement: It can help you plan and save more effectively for your future, and in the best scenario, it might help you realize that you can retire early.

This article originally appeared on The Motley Fool.

The Motley Fool has a disclosure policy.

- MOST POPULAR IN National