Citigroup Inc (NYSE:C) Earnings Preview: Q4 Sales Erode, Profit Up On Cost Cutting

Citigroup Inc. (NYSE:C), the nation’s third-largest bank by assets, is expected to report declining fourth-quarter revenue but a 153 percent jump in profit as it rebounds from a year-ago quarter weighed down by heavy charges. Citigroup also continued to squeeze expenses amid a slump in fixed-income trading and mortgage banking revenue.

“Citigroup is going to have a disappointing quarter because they don’t seem to be able to generate revenues,” said influential bank analyst Dick Bove of Rafferty Capital. He is also the author of a new book, “Guardians of Prosperity: Why America Needs Big Banks.”

“They’ve put too much focus on restructuring the business and reducing costs in the business,” Bove added. “Their trading is not going to be any good either.”

The New York-based bank struggled under the weight of its mortgage woes in the fourth quarter of 2012, taking a hit of $1.3 billion in legal costs and related expenses. The bank posted earnings of $2.15 billion, or 38 cents a share, significantly below analysts’ estimates. For the last three months of 2013, analysts polled by Thomson Reuters expect Citigroup to earn $3.05 billion, or 96 cents a share. Revenue is projected to be $18.19 billion in the fourth quarter of 2013 compared with $18.66 billion in the same period a year ago.

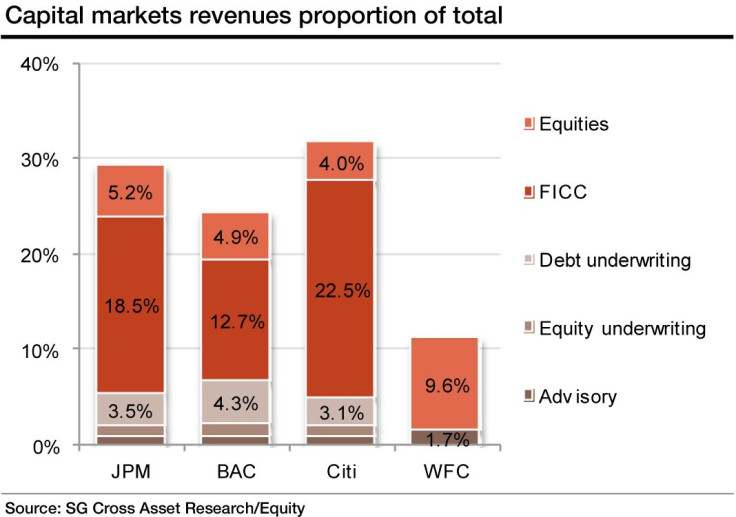

Fourth-quarter revenue from capital markets and investment banking probably will fall short of 2012’s final three months, Chief Financial Officer John Gerspach warned on Dec. 10. “As we look to the fourth quarter, the capital markets environment remains somewhat muted, with revenues tracking slightly below the same period last year,” Gerspach said.

“In investment banking, quarter-to-date results are tracking better than the third quarter, driven by M&A and equity underwriting. However, we expect to be down somewhat year-over-year given the strong debt underwriting revenues in the fourth quarter of last year,” Gerspach added.

Citigroup expects net interest margin to have remained roughly flat in the fourth quarter. Meanwhile, there will be little help from loan-loss reserve releases for the quarter.

For the full year of 2013, Citigroup is likely to record a profit of $14.39 billion, or $4.56 a share, on revenue of $76.96 billion. In 2012, the bank posted earnings of $11.92 billion, or $2.44 a share, on revenue of $77.13 billion.

Fixed-Income

At the center of the weak top-line growth is Citigroup’s fixed-income unit -- a closely watched division that has helped in past quarters to buoy the bank’s overall earnings.

Revenue from the bank’s fixed-income trading plunged 26 percent, to $2.78 billion in the third quarter of 2013 – a trend that is expected to continue. More importantly, none of Citigroup’s other business units emerged to pick up the slack from the fall in trading revenue.

Offloading Non-Core Assets

Citigroup was the largest bank in the world by total assets until the global financial crisis. Like its peer Bank of America Corp (NYSE:BAC), Citigroup suffered huge losses during the financial crisis and was rescued in November 2008 in a massive stimulus package by the U.S. government. Eventually, by December 2010, it had repaid the emergency aid in full.

In the wake of the financial crisis, Citigroup started to reduce its presence in emerging market economies, which accounts for about 30 percent of the bank’s consumer lending. The bank now has two units: Citicorp (core unit), and Citi Holdings (non-core unit), which includes operations it wants to sell or run off.

Citigroup sold its entire stake in Indian's biggest mortgage lender, Housing Development Finance Corp., in February of 2012. In 2013, Citi has divested/repositioned its consumer business in Turkey (one of the larger contributors to expected savings), Poland, South Korea, and to a lesser degree the U.S.

Gerspach said in the bank’s third-quarter earnings call in October: “Revenues in Korea could begin to stabilize in early 2014, but we expect this market to continue to present a drag on year-over-year revenue comparisons for Asia through at least next year.”

“A reasonably large proportion of the savings will be driven by the branch closures in these markets. Other markets such as Pakistan and Paraguay continue to be on the list for future action,” Societe Generale’s Brajesh Kumar wrote in a note.

The efforts are part of a plan by Citigroup’s CEO Michael L. Corbat, to cut yearly costs by $1.1 billion by 2014. The plan also includes 11,000 layoffs across the bank’s global operations.

“Assuming no change in the revenue environment, we would expect core operating expenses to trend somewhat lower in the fourth quarter as additional benefits from our repositioning actions would be partially offset by some seasonal marketing expenses,” Gerspach said in December.

Stock Performance

Citigroup had a great run in 2013 with a gain of 31.7 percent.

“We reiterate our ‘strong buy’ rating on Citigroup ahead of the fourth-quarter earnings given its attractive valuation and still favorable outlook for double-digit growth in operating EPS,” Raymond James analyst Anthony Polini said in a Jan. 2 note.

Shares of Citigroup are among the cheapest for any bank relative to forward earnings estimates.

“Any bank that is selling at a discount to book value, I’m going to buy, because the discount is going to go away and Citigroup is selling at a big discount to book value,” Bove said.

Shares of Citigroup closed up 0.43 percent, or 23 cents, to $53.95 a share in Tuesday’s session.

EDITOR'S NOTE: THIS CORRECTS AN EARLIER VERSION THAT STATED CITIGROUP'S SHARE PRICE ROSE 27 PERCENT DURING 2013 RATHER THAN THE 31.7 PERCENT IT ACTUALLY ROSE.

© Copyright IBTimes 2025. All rights reserved.

- MOST POPULAR IN Business